Real Estate Investment Trusts (REIT) is basically a pool consisting of income-generating real estate assets that are held similarly to a Mutual fund. Just the way in Mutual funds, with REITs, the investor’s funds are deployed in commercial real estate spaces/assets. Through REITs, retail investors get an opportunity to invest in commercial properties which otherwise, would have just been a distant dream.

Units under this portfolio are sold to investors through a public offer. Once these list on the exchanges, the unitholders can trade the units in the secondary market

Types of REITs.

Equity REITs – Equity REITs basically make money by the owner giving spaces like shopping malls, large office spaces, massive residential townships to tenants on the lease. The income earned is then divided among the REITs investors in the form of dividends.

Mortgage REITs – Here, there is no concept of an owner. There are only finances that are taken against the debt which is taken for the development of the real estate projects. Basically, Mortgage REITs earn income in the form of EMI’s which are then distributed among the REITs investors as dividends.

Structure:

SEBI requires REITs in India to have a three-tier structure like mutual funds. The sponsor sets up the REIT, the manager runs the portfolio and the trustee is supposed to watch over both.

-

Sponsor – they hold at least 25% in the REITs for 3 years and 15% after that. Their main responsibility is to set up the REIT and appoint the trustee. To ensure that doubtful entities don’t promote REITs, sponsors need to have a minimum net worth of Rs 100 crore and at least 5 years of experience in the real estate industry.

-

Manager – who is a company or an LLP or a body corporate which manages and operates the REIT. A manager has to have at least 5 years of related experience along with other requirements as notified.

-

Trustee – who generally oversees the activities of the REITs who is appointed by the Sponsor.

What is the minimum investment required?

The minimum application value has been cut down to the range of Rs 10,000-15,000 for both REITs and InvITs, compared to the earlier requirement of Rs 50,000 for REITs and Rs 1 lakh for InvITs, Sebi said in two separate notifications dated July 30, 2021. The allotment to unitholders will be in the multiples of the lot size.

However, once listed they can be traded in single units.

Where are the funds invested?

A REIT in India is mainly allowed to invest in completed and revenue-generating assets and other approved investments. Also, REIT has to distribute the majority of the income they produce among the unitholders.

REITs can mainly invest in commercial real estate through two ways – (i) directly and (ii) through a Special Purpose Vehicle (“SPV”) which has to invest more than 80% of their assets in properties.

The remaining 20% can be in under-construction properties, listed or unlisted debt of real estate companies, listed or unlisted equity shares of real estate companies, mortgage-backed securities, g-secs, and money market instruments. If the REIT is being done through an SPV, their ultimate holding in the SPV should be at least 26%.

In terms of leverage, REITs are not allowed to take leverage of more than 49% of their total assets making sure that they are not over borrowing.

How are returns distributed?

Unitholders earn income through rentals received from properties owned by REITs which could be through dividend income, interest income, or capital gains via the sale of units in the secondary market.

The REITs make money through 3 sources:

-

They receive rent from the commercial properties which have been leased out.

-

Interest payments from their subsidiaries or SPVs which they have funded to develop the property.

-

Capital appreciation of their properties.

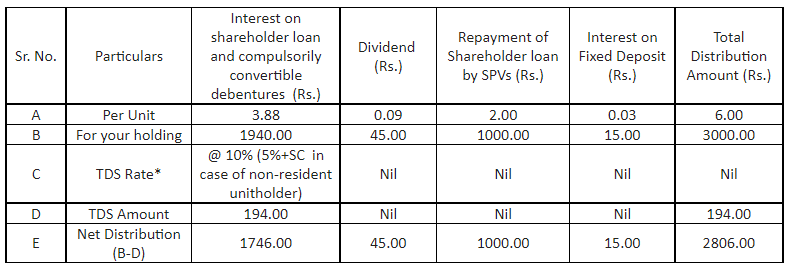

They are required to distribute 90% of the income they receive to the unitholders. These distributions are mandated once every six months.

What should you be considering before investing in REIT

-

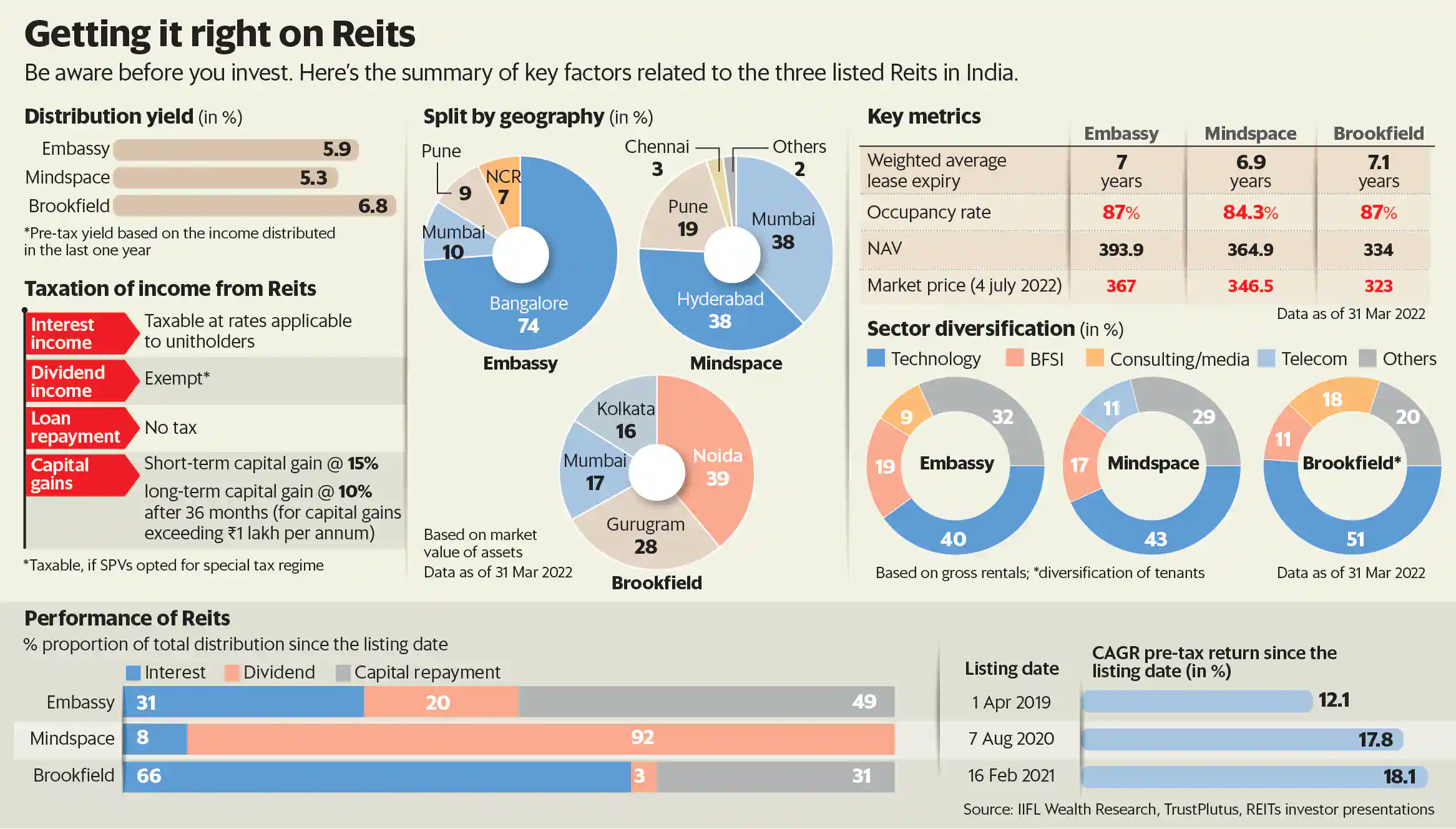

The biggest risk of running a commercial property is the vacancy which is measured in years through Weighted average Lease Expiry (WALE). Higher the time for a property to be vacant, the better.

-

By law, REITs have to pay 90% of distributable cash flows to the investors. The metric to measure this is the distribution yield. Also, this is not a guaranteed payout and depends on the trust performance.

-

A property that is in a prime location will have a high occupancy rate. If the occupancy rate is high, the cash flows are stable.

-

NAV: This is calculated as the estimated market value of all the properties minus the liabilities divided by the number of shares outstanding. NAV provides quite a fair estimation of the REIT performance and its capital appreciation.

How does taxation work in REITs?

There are basically 6 types of scenarios which can be constituted as Income from REITs (interest, dividend and rental, other income, loan repayment by REITs and sale of units)

1. Interest Income:

- For us residents, It will be taxed at applicable slab rates.

- For NRIs, the rate of tax is 5%

2. Dividend Income:

There are two categories in this: Qualified and Disqualified Dividend Income

If the Special Purpose Vehicles (SPVs) of the REITs follows concessional corporate tax rate, dividend Income from such SPVs shall be taxed at applicable slab rates or else it is exempt.

However, in most cases it is exempt.

3. Rental income:

It will be taxed at applicable slab rates.

4. Any Other Income Taxable in the hands of the REITs:

Tax is exempted for unitholders.

5. Loan repayment by REITs:

Till the total distributed loan repayment is less than issue price, it can be deducted from the cost of acquisition of units.

Once the total distributed loan repayment is greater than issue price: The excess amount is considered as Income from other sources and taxed at slab rate.

*Earlier, The return of capital was neither taxed in the hands of the trusts nor the unit-holders. The above changes were made as a part of the Amendments to the Finance Bill, 2023

6. Capital gains on sale of units of REIT

-

If the holding period is less than 36 months, STCG is applicable at 15%

-

If the holding period is more than 36 months, LTCG is applicable at 10% without indexation benefit

InvITs:

Similar to REITs, Investment Infrastructure Trusts (InvITs) pools money which is then invested in cash flow generating infrastructure projects such as highways, roads, pipelines etc.

Structure:

They typically have a 4 tier structure

-

Trustee: These are the debenture trustees which are required to be SEBI registered.

-

Sponsor: Promoter, LLP, or a corporate body with a net worth of atleast 100 crores who sets up the trust and must hold at least 15% of the total InvITs for a minimum of 3 years or as notified by any regulatory requirement.

-

Investment Manager – It is a company or an LLP or a body corporate which basically manages all the business activities surrounding the InvITs.

-

Project Manager – He is responsible for the execution of the project and in the case of PPP, it is the entity formed that has to take care of responsibilities surrounding the execution of the project.

Since the units of REITs & InvITs are listed on the exchange, one can easily buy/sell them in the secondary market.

REITs listed in the exchange

| Name | Symbol |

| Brookfield Real Estate Trust | BIRET |

| Embassy Office Parks REIT | EMBASSY |

| Mindspace Business Parks REIT | MINDSPACE |

InvITs listed on the exchange

| Name | Symbol |

| India Grid Trust | INDIGRID |

| IRB InvIT Fund | IRBINVIT |

| POWERGRID Infrastructure Investment Trust | PGINVIT |