Hello Everyone,

I have been a client of Zerodha since the NEST client and the Zerodha Trader days, from far back in about 2011-2012. Being witness to the tremendous and exciting growth, diverse initiatives taken up by Zerodha over the years like ZConnect, 60 Day Challenge, Varsity, Pi Trading Software, Kite Web, all the way up to the beginning of the Rainmatter works like Sensibull and Coin, I would like to say that the hunger to do something innovative and beneficial for retail traders has always been very strong at @nithin Zerodha and i have always admired all the dedication and hard work and would like to thank everyone for it. ![]()

Personally having been severely focused on SAR moving average like strategies on NIFTY for majority of my trading years of whom very less number were profitable, I paused trading towards the end of 2017. I had to change something, learn something more because most of the profits which i made would be given back to the markets. While using futures as my trading vehicle the major problems which i faced were -

-

Gaps against my position leading to unnecessary hitting of stop losses.

-

Lack of ability to tailor my position size which would not let me stay in the market for the duration i wanted.

-

Very high risk with futures (related to point no. 2)

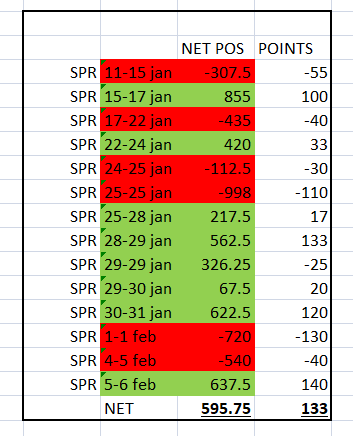

Varsity has been very helpful, the Options theory module in particular. Learning about vertical spreads (credit) has been very much beneficial thanks to the free trial provided by @Sensibull. So much so that i could sort of end Jan 2019 sort of without a loss despite NIFTY being range bound (personal journal snippet attached) when in similar situations i would have easily lost trading futures.

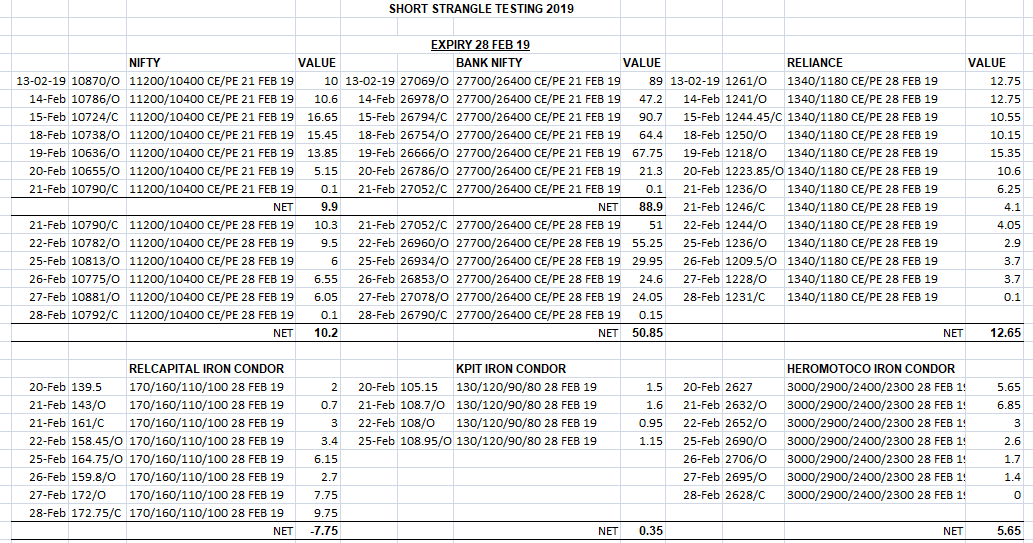

Moving on, the idea of selling strangles apart from using credit spreads for directional trades emerged when nifty weekly options were launched. Selection of strikes using the historical volatility data of NIFTY, BANK NIFTY and some stocks as mentioned in the Varsity chapter. Resulting in the following observations over Feb 19.

This was just a plain noting down for profit accrued due to theta decay. The volatility factor was still missing, entering these trades at times of high volatility would give a better return on every trade, i guess. Increase in volatility inflates prices, been listening to @Sensibull webinars religiously. So recently the thought of using Bollinger Band Width on a relatively smaller time frame to gauge that occured.

The premium available was much higher in the weeklies as compared to the observations aforementioned on the image.

So a few questions to anyone and everyone:

-

Is this a reliable way of measuring sudden change in volatility in Index and Scrips?

-

Should short strangles/straddles be traded in this manner? How long to keep them, booking them at a percentage of profit or holding them till expiry if not is loss zone. Likewise using percentage of max profit as loss point or waiting till a strike in breached?

-

Will the slippage in the most active stock options be too high?

-

Can drops in volatility be sustain-ably traded this way over the long term or the theoretical unlimited loss in such strategies should lead to the dropping of this idea altogether?

-

Am I somewhat going in the direction towards least draw downs and sustainable profits?

Too many questions for anyone who may have labored patiently through this long first post:grinning:. All suggestions and guidance welcome.![]()