There’s a very innovative corporate action that Britannia underwent last month, wherein they issued bonus debentures to all their existing shareholders. Personally, I’d never heard of bonus debentures before and found the concept pretty interesting. Sharing here for the larger community’s benefit

What are bonus debentures?

We all know the concept of bonus shares, where companies convert a part of their free reserves into additional shares. Similarly in the case of bonus debenture issues, the same free reserves are converted into debt instruments (NCDs) that are issued to existing shareholders. The total number and value of outstanding shares of the company remains the same.

The basic idea then is that companies create fresh debt securities out their free reserves, and issue them to their shareholders (thus effectively borrowing from their shareholders). This is a cheap way to raise capital for companies at affordable rates.

What’s the difference ?

Unlike bonus issues where there is no wealth creation, in case of bonus debentures every existing shareholder of the company is credited additional NCDs into their demat accounts. This is in addition to the existing shares, whose value continues to be the same. As a result, there is wealth creation in case of bonus debenture issues.

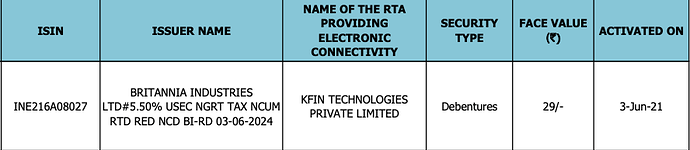

These additional NCDs issued are tradable on the exchange, and shareholders can sell them and lock in their profit. So for instance in Britannia’s case, the company issued to each of its shareholders an NCD of face value Rs 29, carrying 8% interest for a maturity period of 3 years. This came at no cost to shareholders.

Explained in another way, the company creates a bond for shareholders from its equity reserves, pays 8% interest on them for 3 years, and after 3 years redeems the bond and gives the principal back to the shareholders. All this, at no extra charge to shareholders.

What are the advantages of doing this?

This is a cheap way to access capital for the company, wherein it has borrowed from its own shareholders instead of raising external debt. The company has also saved on the administrative costs associated with raising external loans.

This is also quite tax efficient. In case the company had paid out a similar amount to shareholders as dividends, those payouts would have been taxed both at the company level and at the shareholder level, resulting in 40+ % tax.

From a shareholder’s perspective, 8% interest is better than what they’d get with FDs and other debt instruments. Of course, they can sell the NCDs anytime they want, since the instruments are listed on the exchange and have decent liquidity.

Win-win for all.

Why doesn’t everyone do this?

A few reasons. The biggest reason is that the Companies Act does not easily allow this. Specific approval is required from the National Companies Law Tribunal (NCLT) to do this, which is a tedious process which might take a few months.

For most companies, they may be borrowing because they don’t have cash on their balance sheet to fund their operations. So a mechanism like this does not really work for them.

My guess is this is typically only possible for companies like Britannia that generate a large amount of cash in their business and don’t have ways to effectively reinvest that cash in the business (FMCG companies or tobacco companies, for instance).