Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how, too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Jindal Steel wants to buy one of the largest European steel businesses

- China: between competition and self-destruction?

Jindal Steel wants to buy one of the largest European steel businesses

Jindal Steel just made a non-binding offer to buy the steel business of Germany-based Thyssenkrupp.

Right now, this is just an expression of interest without a formal price tag, not a signed deal. But Jindal is ready to splash billions of euros on buying one of the oldest names in European steel, which also operates the largest steel plant in Europe in its headquarters — Duisburg.

But, the plant is also one of the dirtiest by emissions, still running on old coal-fired blast furnaces. To keep selling steel in Europe, where strict climate rules are being rolled out, Duisburg has to be rebuilt. That is going to cost a fortune, and Thyssenkrupp has been struggling to find someone willing to foot the bill, until now.

Let’s unpack this potential deal.

Why is Thyssenkrupp trying to sell?

Thyssenkrupp used to be a sprawling German industrial giant whose history spans all the way back to the 1800s. It made steel, car and ship parts, and its elevators and escalators were known worldwide. If you’ve ever taken a lift (or escalator) in a metro station, airport, or even society building in India, you probably noticed their logo.

But in 2020, the group sold its entire elevators business for €17 billion (~₹1.5 lakh crore). It was drowning in debt and needed a reset. That sale gave it cash but also signaled a shift in strategy. Thyssenkrupp no longer wanted to be a jack of all trades. It wanted to slim down and master just its core businesses.

But Europe’s new climate rules threw a wrench into those plans. Duisburg’s green rebuild will take billions — its old furnaces have to be torn down and replaced with those running on cleaner sources like hydrogen. But, it is also losing money fast: it makes €10.7 billion (₹80,000 crore) in revenue a year but often runs at a loss.

The company has tried different escape routes, none of which worked. A joint venture with Tata Steel was blocked by the regulator. UK’s Liberty Steel circled but never closed. In 2023, Czech investor Daniel Křetínský bought 20% of its steel arm, but that didn’t solve much.

Jindal wants a shot at the world

Jindal Steel is obviously one of India’s biggest private steelmakers, with over 90% of its sales being domestic. Its overseas bets so far have been small and scattered—coal mines in Mozambique and Australia, an iron ore project in Cameroon, and a recent purchase of a small steel mill in the Czech Republic.

None of these deals changed its core identity. But taking over Thyssenkrupp’s steel arm could make a dent to it.

Consider this: Duisburg alone produces nearly 10 million tonnes (MT) of steel a year. Owning it would put Jindal on the same global stage as Tata Steel and ArcelorMittal. It would open up a new market in Europe, where new rules and technologies are reshaping the future of steel.

This acquisition might also strengthen Jindal’s supply chain. It would start with high-quality iron ore from its African mines. This will be shipped to Oman, where it is building a new hydrogen-ready plant to turn that ore into sponge iron. From there, the output would be fed directly into Duisburg’s furnaces. There’s no doubt this jigsaw puzzle has a lot of complex logistics involved, but it’s ambitious.

The reward of this bet could be global scale, access to a new market, and a solid place in the green steel transition. And Jindal seems willing to take it. But this is no simple acquisition. Jindal will have to bear the burden of a full green rebuild. And it isn’t just the furnaces — Thyssenkrupp is also tied down by pension obligations to workers worth €2.7 billion (~₹24,300 crore).

Are the costs worth it? We aren’t steel experts so we can’t answer this for sure. But we can look into how hard it is.

What does “green steel” actually mean?

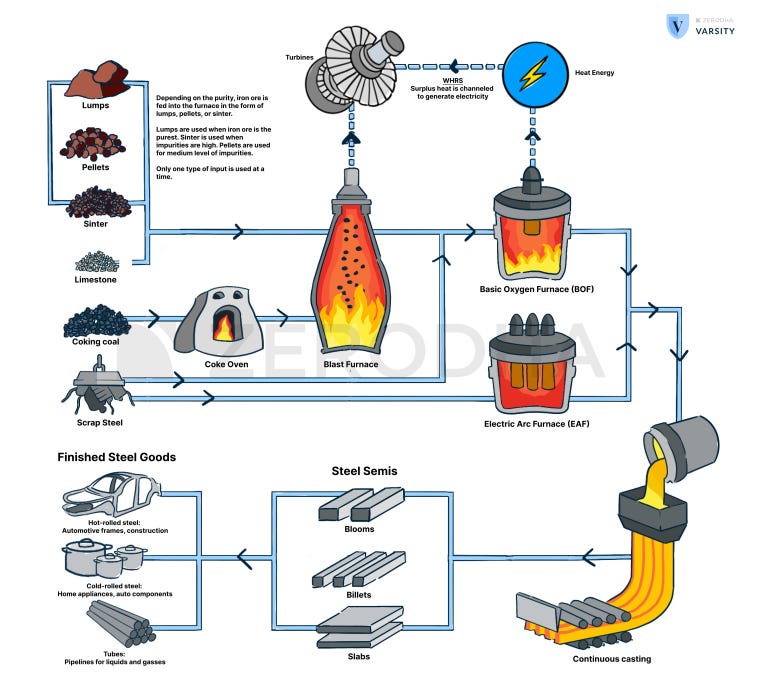

To see why green steel is so expensive, it helps to understand how steel is made today.

A traditional blast furnace takes iron ore and mixes it with coke — a fuel made from coal. The coke provides the heat but also does the chemistry, stripping oxygen out of the ore. The end product is molten iron, but the process releases huge amounts of carbon dioxide — roughly two tonnes for every tonne of steel made this way. And Europe has called an end to this model.

The replacement is the hydrogen route. Instead of coal, you use hydrogen gas to react with the iron ore. That produces iron without releasing CO₂. The iron then goes into a different type of furnace called an electric arc furnace, which runs on electricity instead of coal. If that electricity comes from renewable sources, emissions can be cut by 90%.

The catch is cost. If you read yesterday’s Daily Brief, you’d know that hydrogen production itself uses a lot of electricity. And electricity in Europe is already costly, especially since Russia’s invasion of Ukraine. A tonne of steel made dirtily might cost ~₹40,000 in Europe; with hydrogen it can jump to ~₹60,000. Green steel is a tall order.

No buyer wants to pay that difference out of pocket, so governments step in with subsidies. Germany is planning €2 billion (~₹18,000 crores) to help Thyssenkrupp build its first hydrogen-ready furnace at Duisburg.

But finishing the transition will cost much more, and that gap is what a private buyer like Jindal would have to fill. And that gap is no patch-up job. Jindal will not only have to finish the hydrogen-ready furnace already under construction, but also install additional electric arc furnaces in Germany. This will require a second layer of investment, and therefore tons of commitment from Jindal.

What about Tata Steel?

It’s impossible to talk about an Indian steelmaker buying into Europe without mentioning Tata Steel’s experience.

Back in 2007, Tata bought Corus, an Anglo-Dutch steelmaker, for around ₹1 lakh crore. At the time, it was India’s biggest-ever overseas acquisition, marking our arrival on the global stage.But that celebration was short-lived. The global financial crisis of 2008 hit just months later. Steel demand in Europe collapsed, and Tata found itself with expensive plants in markets that weren’t growing.

The acquisition has always been a drag on Tata Steel’s balance sheet. The bigger of the two ports in its European business — Port Talbot — has been the problem child, running losses for years.

The UK government recently agreed to put in ~₹5,250 crores to help Tata shut down its old furnaces and replace them with a smaller electric arc furnace. But that only helped survival and not growth. And because of the replacement, thousands of jobs were at risk, creating a trade-off between climate goals and employment.

Europe has been a tough market to crack for Tata, and that history hangs over Jindal. If a giant like Tata has struggled for so long to make Europe work, can Jindal really do better? The hope is that the circumstances have changed enough for Jindal. Additionally, Thyssenkrupp’s representative union — which didn’t like the sale to Kretinsky — has welcomed the Jindal offer.

But, as we shall see, even if they have changed, Jindal could be walking into a market where the risks are no joke.

Europe, a landmine of a market

Well, for one, demand in Europe has been flat for years . Europe consumes 140 MT of steel annually, and that number hasn’t really grown in over a decade. The continent’s auto industry, once a strong driver of demand, is in flux as it shifts to EVs which use different supply chains — and hence, less traditional steel. Construction, another big consumer, has slowed as high interest rates make new projects more expensive.

On top of this, imports give too much competition . Europe has long complained about cheap steel arriving from Asia, especially China. Even with tariffs and safeguard duties, shipments continue to flow in at still-lower prices. European producers struggle to raise their own prices, no matter how high their costs are.

As we mentioned earlier, European energy costs are among the highest in the world . After Russia’s invasion of Ukraine, natural gas and electricity prices in Europe soared. Despite some decline, they remain higher than what steelmakers pay in India, China, or the US.

Additionally, climate rules add both pressure and opportunity . Europe is introducing the Carbon Border Adjustment Mechanism (CBAM). This is basically a tax on imports of carbon-heavy goods, steel included. It is meant to level the playing field — so that European producers who invest in cleaner technology aren’t undercut by cheaper, dirtier imports. For a producer who actually goes green, CBAM is protection. But for those who can’t, it’s a nail in the coffin.

Lastly, rivals are hedging their bets . ArcelorMittal, Europe’s largest steelmaker, is investing billions to decarbonise its plants on the continent. At the same time, it is putting more money into India and North America, where demand is growing and costs are lower. Clearly, they don’t expect Europe to be very profitable, but their survival still depends on expanding there.

That’s the environment Jindal would be buying into. A stagnant market, high costs, strict rules, and rivals who are investing in Europe.

Conclusion

For Thyssenkrupp, Jindal’s interest is a potential escape hatch. The company has been trying for years to find a solution for its struggling steel arm. If a buyer comes along who is willing to carry the pension liabilities, finish the green rebuild at Duisburg, and keep jobs in Germany, that is about as good an outcome as management and policymakers could hope for.

For Jindal, it is the boldest overseas move it has ever attempted. If the deal goes through, it would instantly become a global steelmaker, not just an Indian one.

Jindal’s offer is still non-binding. The real test will come when it has to commit: is Jindal ready to spend the money and stay the course long enough to see a payoff? If it does, it could mark a new chapter in India’s rise as a global steel power. If it doesn’t, then just like Tata, it will be yet another disaster.

China: between competition and self-destruction?

Lately, the headlines from China read like a corporate bloodbath. And we couldn’t ignore this onslaught of news anymore.

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

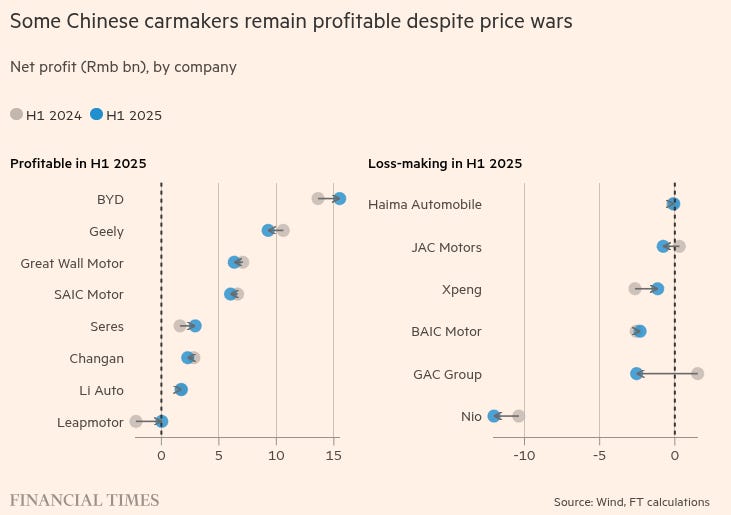

BYD, arguably the world’s largest EV maker today, slashed its sales forecast by 16% to 4.6 million units as an "intense price war " decimated profits. Investors responded by selling off $45 billion worth of stock. China’s food delivery firms have agreed to a truce after a devastating, subsidy-fueled price war last year. China’s solar industry is in heavy losses.

In no way are these isolated incidents. They’re symptoms of something called "involution " (neijuan in Chinese). It’s a situation of extremely-intense competition where companies keep lowering their prices — even below cost — in order to sell more.

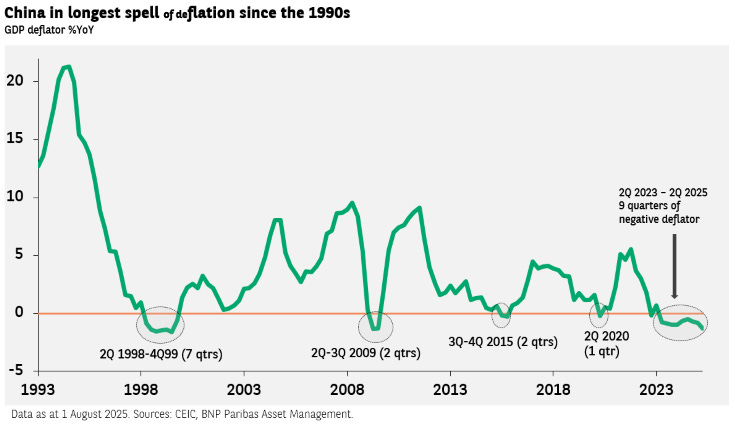

This might sound normal, but there’s a huge problem: in China, nobody’s winning this race. It has left entire sectors teetering on the edge of profitability. In fact, China is in its longest period of deflation since the 1990s.

However, neijuan is also a product of how China’s economy is designed. Attempts to curb it might fundamentally go against its foundations. We’ll be going into how, more than anything, neijuan is really a story of trade-offs — and how China is trying to manage them.

Let’s dive in.

The blurry line between competition and involution

Before we get into China, let’s answer a fundamental question: what’s the line that separates competition and involution?

Well, “healthy” competition always expands the pie. Firms compete by making new products, or achieving better efficiencies, or getting to economies of scale. This drives down costs while improving quality, benefiting both businesses and consumers. Competition is undoubtedly one of the most important drivers of innovation.

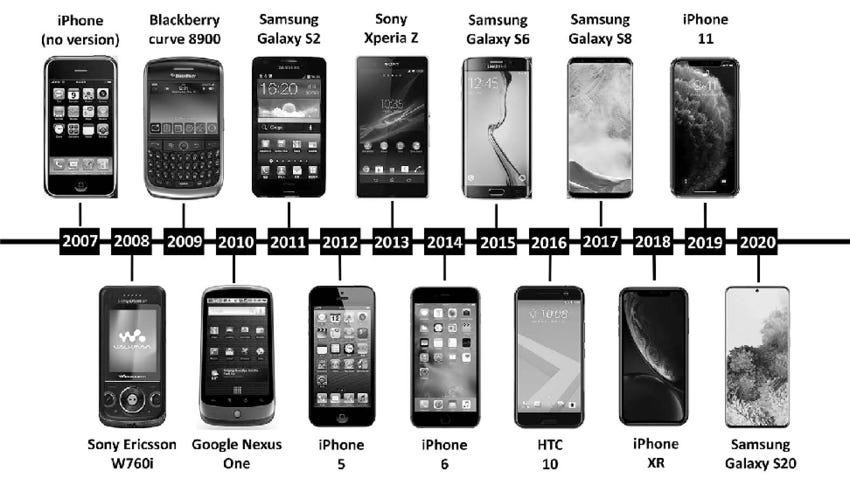

Take the smartphone market, for instance. With each passing year, phones got cheaper, had better cameras, faster processors, and longer battery life. A range of companies competed to get here: Apple, Xiaomi, HTC, and so on.

You might be thinking: isn’t this wonderful? Shouldn’t we have more of it? Of course we should. But what happens when this virtuous cycle stops as industries mature?

In effect, it creates a fixed pool of demand that firms have to fight for. Then, the only way to compete is not by innovating, but by lowering prices, or expanding volume capacity . As a result, across the industry, profits evaporate, and firms that took on debt to expand capacity find it harder to repay. That’s when you know competition has gone from being great to being unhealthy.

Many countries have suffered this at some point. Japan’s electronics giants went through similar cycles in the 1990s. In fact, involution goes as far back as the 19th century, when American rail firms fought to build railroads that often overlapped each other — creating vast inefficiencies with too many tracks.

But China’s version is unique for two reasons. One, the country’s sheer scale — at over 1.4 billion people — magnifies this problem. The second reason has to do with how China’s economy itself is structured — and the tensions it creates. That’s what we’ll address next.

The structural roots of hyper-competition

The primary reason for why Chinese firms compete so intensely has a lot to do with the role of the Chinese government.

The state’s visible hand

In China, bank credit is mostly controlled by the state instead of the market. They decide which industries deserve loans — and for those target sectors, those loans are made extremely cheap . This means that companies — no matter how big or small — could borrow to invest in new capacity relatively easily. Banks often continue rolling over loans to avoid defaults, adding further to excess capacity.

This creates a situation where domestic demand for a good is far behind its supply. Far more money goes into investing in production than consuming it. As a result, a lot of unproductive firms get too much money.

And this is by design . The idea is that a lot of competition is good for technological development, and eventually, the herd will thin itself to a few big “national champions ” (something we’ve covered before). But it’s a double-edged sword that can lead to over-supply. As we shall see later, the strategy that allows for many bets is, ironically, different from the strategy that decides the winners of the bets.

Involution is amplified by how China’s local governments work. They fiercely compete with each other to develop the same high-growth, high-prestige industries like EVs or AI. They woo investors with free land, subsidies and cheap loans, leading to inefficient duplication of efforts on a national scale. Take the province of Hebei, for instance. Companies there are called “price butchers ”, because no one dares to down-bid them.

Other important factors

There are other factors that add to the magnitude of involution. For one, Chinese consumers are extremely price-sensitive and love chasing bargains — just like India. Years of abundant supply and low, transparent prices mean that even a single seller reducing prices by a few yuan shifts demand considerably.

What also matters is the type of product — how much it can be differentiated, and how easy it is to enter. Low-end manufacturing products like t-shirts, toys, pencils, socks, bedsheets, furniture and so on. Without unique technology or branding, competition here inevitably becomes pure cost-cutting. China dominates such low-end goods.

Because of these reasons, the trend in China is usually one where hundreds of brands (instead of just a few) exist to fight over the same pie. And some key industries have emerged as the poster-children of this problem.

Major industries caught in the involution trap

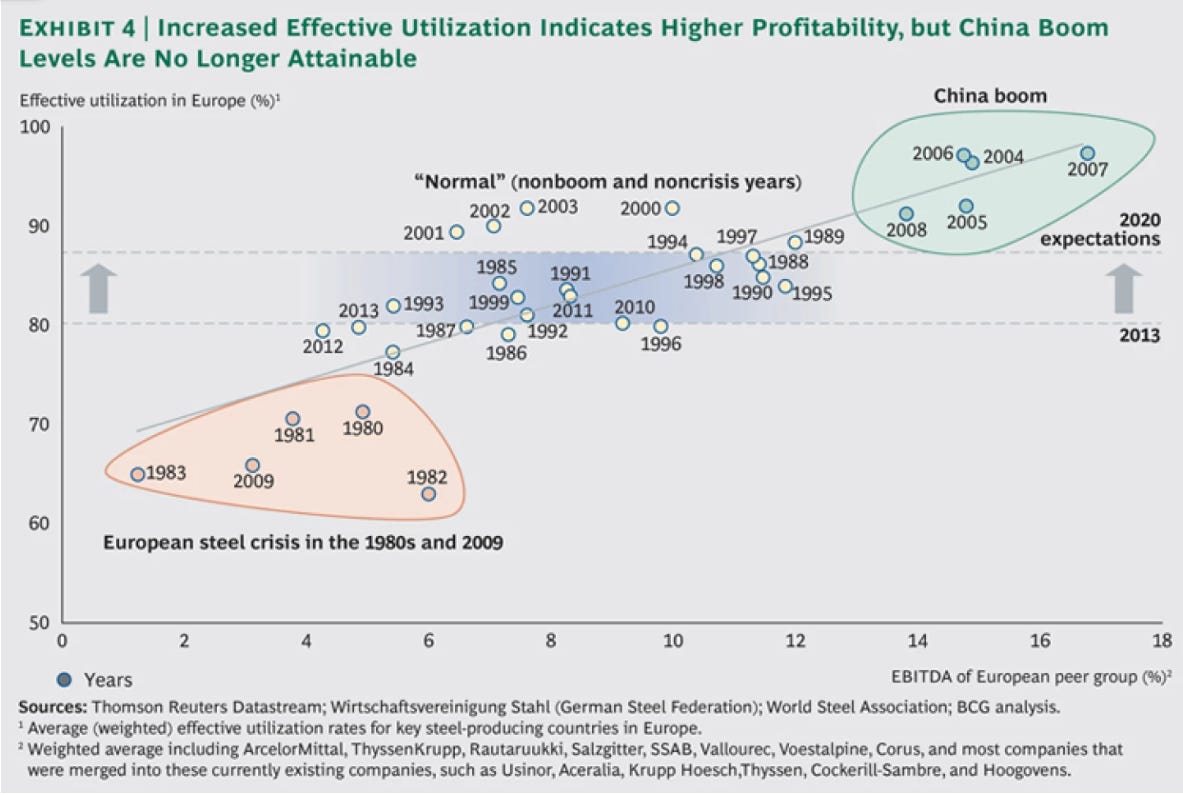

Steel is arguably the most important case study in neijuan . In the 2010s, there was a frenzied expansion of steel mills, many backed by local governments chasing growth. By 2015, China faced such massive oversupply that prices plunged and mills were hemorrhaging money. Additionally, at the time, China did low-end forms of steel well, which worsened the problem. This issue was so big that it led to a global — forget domestic — over-supply of steel.

Source: BCG

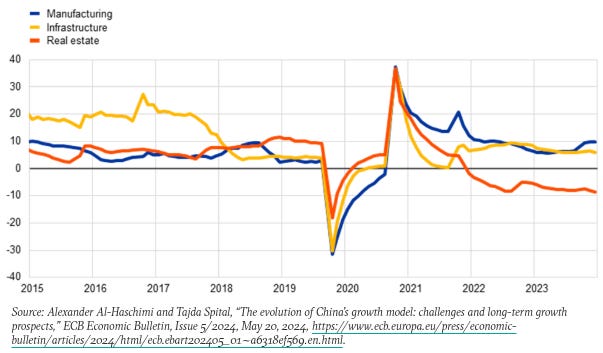

The oversupply of steel was partly because of another, hotly-debated industry that uses a lot of steel and cement: real estate. Now, it isn’t a textbook case of involution: since houses are much less in supply than other goods, their prices generally rise with more demand. But excess competition fueled by cheap credit did fuel a bubble in the sector.

To make houses, there are mainly two ways to compete: build faster , or build cheaper . Chinese firms like Vanke and Evergrande (that we covered recently) did both. But this created an excess of homes that never got sold, bursting the bubble and deflating prices massively.

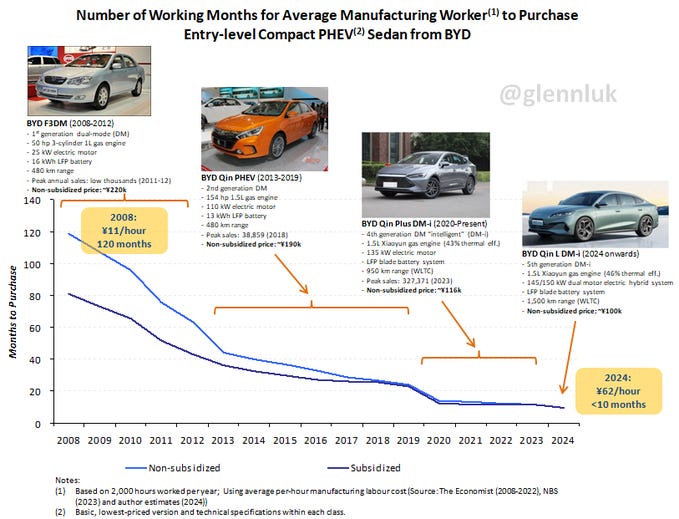

A new-age industry that’s suffering from involution is EVs . China’s EV market is the world’s largest and is an outright success story of technological prowess driven by competition. The chart below shows how the price of an entry-level BYD car fell because of technological improvements — that even a Chinese factory worker can buy it now.

But there may be signs that this co-exists with involution. Sales volumes grew nearly 10x between 2020-2024, and China is leading the world in EV battery technology. But at the same time, due to involution, the median net profit margins for Chinese automakers fell from 2.7% in 2019 to just 0.83% in 2024. BYD saw its first profit decline in over three years. Some firms are cutting projections, while others — like Xiaomi — are advancing with better products.

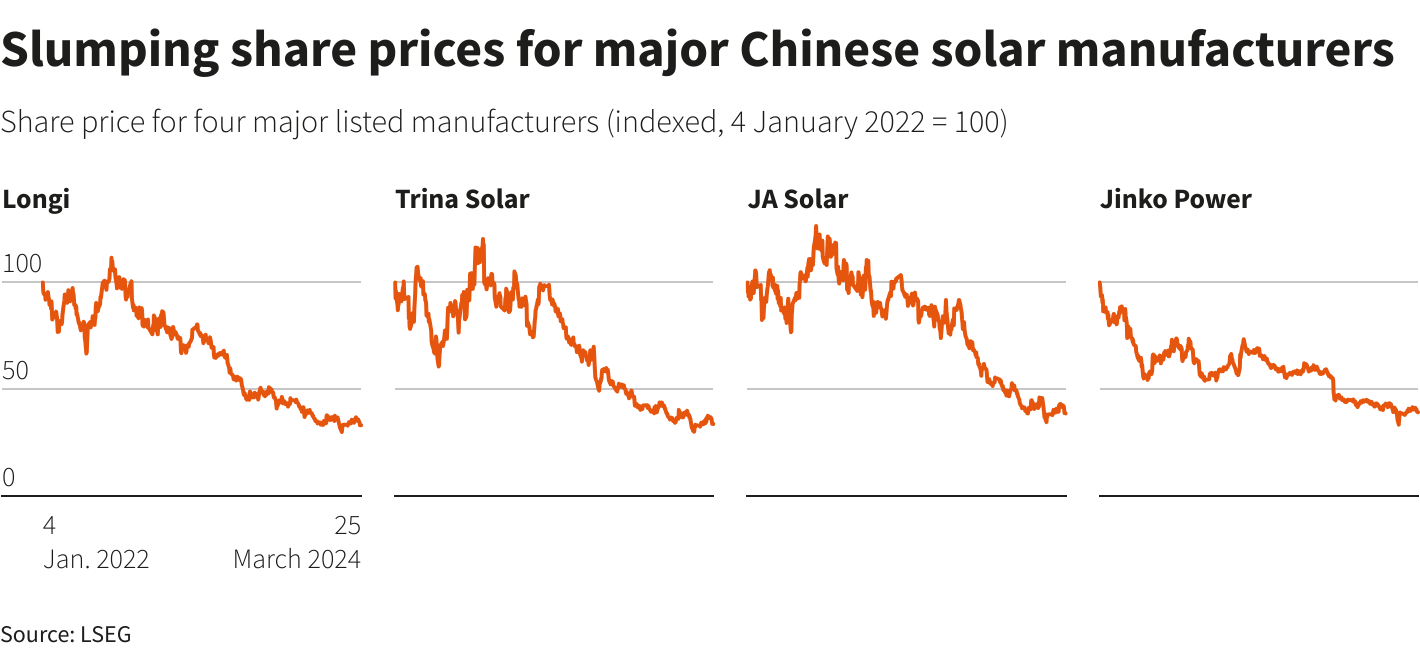

Similarly, China’s solar power capacity is the largest in the world. Increasing efficiency in Chinese solar cells is steeply lowering panel prices, benefiting consumers worldwide. This is a huge step in the fight against climate change. Moreover, there is enough demand for it within China, so it’s not the biggest issue.

However, price wars due to over-supply might be, as Chinese solar firms collectively lost $40 billion in 2024. China’s 2024 capacity for solar parts was so large it could meet global annual demand through 2032, even if no one else built a factory. Giants like Jinko and Trina Solar swung into heavy losses. The resulting picture is a wild contradiction: China dominates the global solar market share, but individual Chinese firms struggle to break-even.

The second-order effects

The most obvious consequences of involution are massive price deflation and unproductive firms being propped up artificially, which we’ve already covered. But there are two interesting — and crushing — second-order effects of Chinese involution.

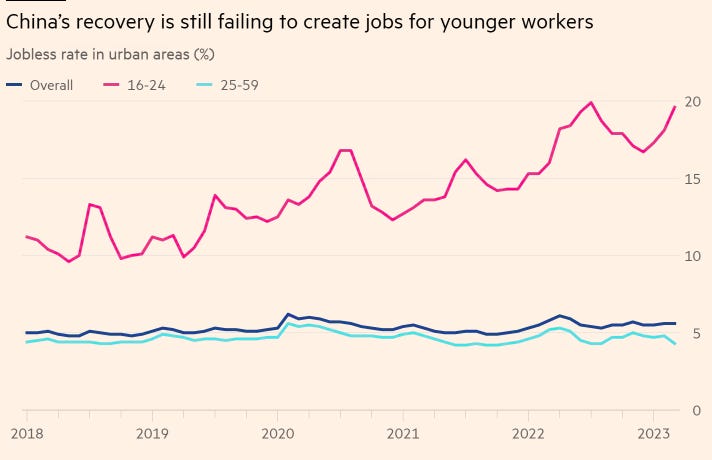

The first one is domestic — how involution distorts labor markets . As companies fight to cut costs, they often do so through longer working hours and stagnant wages. The infamous “9-9-6” work culture (9am-9pm, 6 days a week) in China partly reflects the pressures of involution. Meanwhile, youth unemployment remains high at ~20% as workers can’t be profitably absorbed.

The second such effect is more international — overcapacity . When China’s excess capacity can’t find enough customers at home, they flood export markets. This benefits global consumers through cheaper goods but also undercuts domestic industries abroad , sparking trade tensions. It’s partly why India (and the US) have imposed tariffs on Chinese goods, or why the EU has launched an anti-subsidy probe on Chinese EVs.

Beijing’s anti-involution campaign

The CCP is on its guard. Last year, it launched an "anti-involution " campaign to stem excess competition. Just recently, president Xi Jinping has explicitly called for authorities to curb “disorderly low-price competition” while promoting “high-quality development” over sheer quantity. Beijing is amending its price laws to discourage selling below cost. It is meeting with leaders of the EV and solar industries to discuss strategy.

In fact, this is hardly the first time China has tried to curb involution. In 2015, Beijing ordered production cuts and encouraged mergers and acquisitions — especially with state-owned enterprises. This consolidates production in fewer, more efficient firms while killing redundant competition. And the entire industry followed quite successfully. The state itself has attempted to manage the exits of failing private firms while stemming the side effects of such a fallout. Evergrande’s managed implosion was an example of this.

That was on the supply side. In 2015, the state also issued a stimulus to increase household demand. However, China doesn’t like this solution for reasons we can’t get into here, one being that it is a strain on state finances. We recommend reading this to dive further.

There are some structural issues with the supply-side approach. For one, China’s model of state-directed cheap credit will continue, as it always has. The model itself spawns excess competition that further needs curbing. Even if the state might attempt to curb capacity in some areas, it’s entirely likely to happen again somewhere else. The imbalance will simply shift to another industry, but it will persist.

Secondly, China has also been strengthening its anti-monopoly initiatives to reduce the abuse of power by large firms. However, consolidations only increase monopolistic power, making both “anti-involution” and “anti-monopoly” somewhat at odds with each other. It could dampen private sector involvement — which makes up most of China’s employment. Capacity closures would also mean lesser jobs, and unemployment is already really high.

In other words, the strategies for competition and consolidation (and capacity reduction) can conflict with each other.

Can China repeat the success it achieved in 2015? Well, the times are much harder now. The imbalances are far worse, and domestic demand is far weaker. It is also harder for China to offload its excess product to countries putting up high tariffs against it. Moreover, China has generally been unwilling to issue another stimulus.

Trade-offs, trade-offs everywhere

Neijuan has both been the driver of China’s incredible economic growth, while also reflecting a structural imbalance between China’s productive supply and domestic demand. And Beijing understands this well.

But it walks a tightrope on what to do. It can’t do too much to reduce competition, in case private sector interest dampens. However, doing too little is taking a toll on the financial health of entire industries, hurting both China itself and other countries. There are pains in both doing something and nothing.

It’s too early to judge whether China’s current anti-involution measures are working. There are some positive signs: some equity analysts have seen solar profits recover, while average discounts across car-makers declined in July.

But what will really matter is if China is able to address the root causes of involution — and whether it can take the hard calls necessary to tackle it.

Tidbits

- JSW Paints–Akzo Nobel deal

India’s antitrust regulator approved JSW Paints’ plan to buy up to 75% of Akzo Nobel India. The $23 billion JSW Group will become the fourth-largest paint player, behind Asian Paints, Berger, and Kansai Nerolac. The move comes as the paint industry faces rising costs and fierce competition.

2.Source:* Reuters - SBI sells Yes Bank stake

State Bank of India (SBI) gained over 3% after completing the sale of its 13.18% stake in Yes Bank to Japan’s Sumitomo Mitsui Banking Corporation for ₹8,889 crore. This is part of SMBC’s plan to buy 20% of Yes Bank, making it the largest shareholder. SBI still holds 10.8%.

4.Source:* Moneycontrol - Dreamfolks halts domestic lounges

Dreamfolks, India’s airport lounge aggregator, has stopped domestic lounge services but will continue global operations. The company faced challenges as airports began offering direct lounge access. It had already lost key contracts and warned of a material impact. Its stock is down 65% this year.

6.Source:* Reuters

- This edition of the newsletter was written by Krishna and Manie

Have you checked out Points and Figures?

Points and Figures is our new way of cutting through the noise of corporate slideshows. Instead of drowning in 50-page investor decks, we pull out the charts and data points that actually matter—and explain what they really signal about a company’s growth, margins, risks, or future bets.

Think of it as a visual extension of The Chatter. While The Chatter tracks what management says on earnings calls, Points and Figures digs into what companies are showing investors—and soon, even what they quietly bury in annual reports.

We go through every major investor presentation so you don’t have to, surfacing the sharpest takeaways that reveal not just the story a company wants to tell, but the reality behind it.

You can check it out here.

Introducing In The Money by Zerodha

This newsletter and YouTube channel aren’t about hot tips or chasing the next big trade. It’s about understanding the markets, what’s happening, why it’s happening, and how to sidestep the mistakes that derail most traders. Clear explanations, practical insights, and a simple goal: to help you navigate the markets smarter.

Check out “ Who Said What? “

Every Saturday, we pick the most interesting and juiciest comments from business leaders, fund managers, and the like, and contextualise things around them.

Join our book club

Join our book club

We’ve started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we’d love to have you along! Join in here.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()