…and was soon clarified as

none of the mutual fund AMCs discussed are government backed.

So for practical purposes they are in the same risk class, with one nuanced exception -

There have been past instances in which mutual fund houses acted in the interest of the masses.

So, one may instinctively feel that investing in such mutual funds houses,

aligns oneself with the masses,

and thus one can expect some additional assurance that

the policies/actions of such a fund house will be friendly to the investor.

However, a key aspect to note is that

investing in any mutual fund of such a mutual fund house,

does not always guarantee that

one’s financial interests are aligned with the interests of the masses.

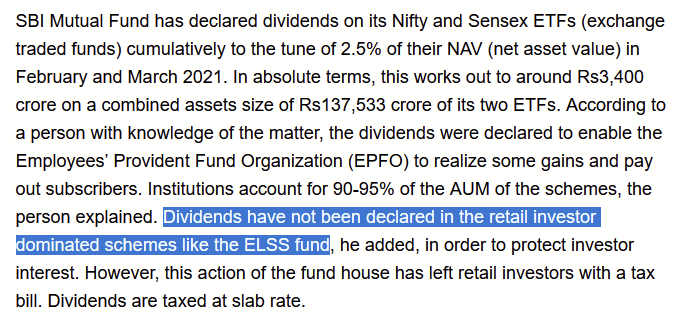

An example of such a difference is

when a specific AMC opted to declare tax-inefficient dividends

a seemingly sub-optimal policy for its investors,

presumably in the interest of the masses (via the major EPFO investment in the security).

At the same time, the same AMC did not follow the same sub-optimal policy for another of the securities they offered, as doing so would have had no major impact on the masses (as no major EPFO investment in this other security).

Source: Article linked earlier in this thread.

In future, the expectation that such an AMC would be bailed-out is far from guaranteed, as the relief that may be provided in such a scenario may apply specifically for the masses and not necessarily to all the investors.

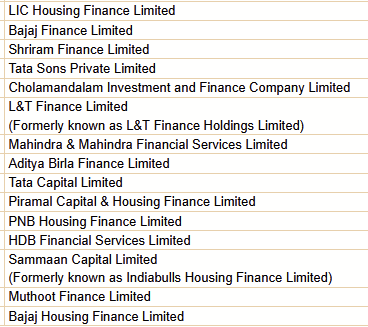

Then how does one identify “too-big-to-fail” institutions to invest in ??

If one is interested in relying on a “too big to fail” aspect, for some form of additional assurance, instead of looking for Government PSUs in the ownership patterns of MF-AMCs as a proxy for “too-big-to-fail”,

one would likely be better served looking to invest in

securities offered by financial institutions formally designated as “too big to fail” -

Note that D-SIB and NBFC-UL/SI designations do NOT constitute any form of additional guarantees or backing for investors. It is just that the institutions designated as such have additional stringent regulations to comply with, which is expected to reduce the risks associated with them (relative to similar institutions without such a designation).