I head passive funds (ETFs + Index funds) business at Motilal Oswal Asset Management Company. Previously, I helped build a venture capital backed robo-advisory firm in San Francisco which managed close to $450 million in assets.

I am passionate about index funds/ETF’s and believe its great for investors looking to build long-term wealth. My approach towards building this business is in keeping things simple and customer-centric.

Hey @pratikoswal, thanks for doing the AMA. A few questions

Why passive now? I mean active has been in the DNA of Motilal - “Think Equity, Think Motilal”. And even the active funds of Motilal are pretty concentrated high conviction bets. How does the launch of passive funds square with the active DNA?

Is the recent undeperformance of active funds, especially the large-cap funds a motivating fator?

Also, do you think these funds will garner AUM. We’ve seen most AMCs jump on the passive bandwagon and most of these funds are pretty much shelf space fillers.

Given that mutual funds are still push based and 100bps is the max you can charge for index funds vs 225 bps for active funds, do you have the financial leeway to pay the distributors to push these products?

Also, based on your interactions, are distributors open to pushing this products?

I am guessing the thrust on passive will also mean a renewed focus on ETFs? Because Aashish in an interview with Livemint had called your ETF business and I quote > Another deviation is the ETF business, although we are not growing it. Is it still a deviation?

Does launching ETF with the index Funds as the underlying make sense. Reverse of what you guys did with N100 ETF by launching a FOF with the ETF as the underlying. This would kill 2 bird with one stone - popularize index funds as well as your ETFs.

Thanks, Rahul - Great questions overall. My responses below:

Actually very people know this but we were the first ones in India to launch ETF’s in 2010. We started with the smart-beta ETF followed by a mid-cap and international ETF. At the time - we were too early and hence pivoted to active strategies. This is our second attempt. We aim to be a strong equity house (whether it be active or passive).

Not at all. And if it were - we would be launching large-cap funds. I personally believe there is no correlation between short-term track record (2-4years) and future performance so this is a long-term initiative.

I think barring 1-2 AMC’s - there’s no real push of passive products in India. At the retail/HNI level - knowledge in passives is very low. I do however see a lot of long-term opportunity in passives (just like in other parts of the world).

I’ve learned this the hard way. The way I see passives grow is via awareness and education (not via commission). It may take a while but I believe its great for customers so totally worth the effort

I think saying and doing are two completely different things. So I’ll have to get back to you on this.

We are committed to both ETF’s and index funds. However, having spent almost 10 years in the ETF space - we feel index funds are better suited for retail + HNI customers. Reasons below:

No Liquidity problems: The industry is plagued with liquidity issues when it comes to trading ETF’s. ETF’s today are mostly bought and sold by institutions who prefer to go directly to the AMC and not the exchange. Retail + HNI customers, as a result, pay a premium to buy an ETF and sell ETFs at a discount. This adds cost and leads to a higher tracking error for the investor. Index funds, however, are directly bought from the AMC who provide daily liquidity.

Demat Account – All investors wanting to buy an ETF need to open a Demat account and buy the unit on the exchange. Buying an index fund is similar to buying any mutual fund.

Brokerage costs – Investors in ETF’s pay brokerage costs (on buying and selling) in addition to the expense ratio. Brokerage and other trading related costs are embedded in the expense ratio

Simpler to understand – Index funds are pure passive funds. ETFs however may not be (eg. CPSE ETF). Customers see index funds as natural investment vehicles whereas ETF’s are seen as trading instruments.

SIP option – Setting SIPs are possible in index funds (not possible in ETF’s).

Great short term hack. May/may not be a good long-term solution

Are there any plans for Motilal Oswal to launch any US based index funds and/or ETFs like the N100 ETF but something more diverse than the N100 (N100 is tech dominant), say the S&P500 or a total market fund like VTSAX. Currently all options available be it funds of funds, feeders, or others, all of them are active funds with fairly hefty TERs (often double the expenses in the cases of funds of funds due to investors having to bear the expenses of the underlying funds on top of the main fund’s expenses).

My query won’t fit to current size of passive markets but I believe it will at some point of time.

Coming to vanilla passive, it is just following some index, so funds will buy any stock which is part of the index and dump the stock if it is leaving that index.

Imagine if passive picks up,then if any stock leaving that index will be dumped by every fund following it,similarly if any stock is being added then again every fund will buy it, I believe this will have effect on price of that stock to a bigger extent. So, basically I want to convey that price of any stock can be moved on mere condition of adding or leaving the index with out it’s fundamental or macro factors.

Every index can have it’s own rules, so index can change it’s rules to kick out or add any stock any time. Can check this as one example. Example 2- MSCI tweaked some rule which has major effect on markets.

Recently in last budget FM proposes to consider of having minimum public shareholding to 35% from current 25%, one reason on this proposal can be related to passive investing in a indirect way. Government want Indian companies to have higher share in MSCI emerging market indices so that more foreign capital will flow to India and to be part of those it is required to have higher free float.

Having said above I am also a believer of passive investing but not plain, something like hybrid/smartbeta.

Coming to India, currently passive is just beginning so I believe it may take a decade or so to see interest in smartbeta ETFs unless something big happen. Would like to know your view about this.

I agree there will be some volatility in the short-term but don’t see any long-term impacts for any of the points above. Smart sellers will start selling stocks if they expect a stock to be removed by the index and vice versa. Active investors + Institutions are always looking out for short-term mispricings and keep the market efficient. The only long-term risk I see is if regulators put sectoral/stock caps. on indexes. It’s not done in any other part of the world so I don’t expect it to happen.

Smart-beta is an interesting concept - we did venture into this in 2010 and launched India’s first smart beta ETF. The initial response was good but the general level of knowledge is limited and we ended up not pursuing it further.

The biggest problem with smart-beta is expectations. You’re promising investors alpha at a low cost and most smart-beta funds out there have not been able to do that. Selling index returns and sticking to it makes it hard to have unhappy customers and will also lead to less customer churning portfolios/funds.

Also, selling Smart-beta funds requires back-testing (in my experience its something I don’t see much merit in). I do however see some advantages of factor-based investing - too early for India in my opinion.

Thank you for your reply. Also what’s your opinion on having inverse ETFs in Inida? you think it is too early to have? as you know did anyone consulted SEBI on this?

Ah, so no plans to do smart-beta in India as of now? For all the hype smart-beta has been BS wrapped in a closet-index wrapper. The biggest smart-beta funds have been nothing but S&P 500 clones in the US.

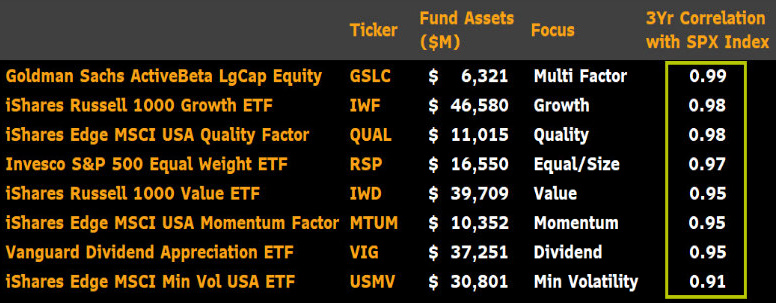

Any thoughts on the NSE factor indices? We do have a few value and quality ETFs which follow these factor indices which are, surprisingly cap weighted. Ideally the true implementation of smart-beta (a retarded term) breaks the link between price and size.

Great insights Rahul. Unfortunately, at this point we want simplicity in our offerings. We will look at Smart-beta when the market matures.

As far as smart-beta investing - I do believe there is a lot of value add in them. Factor based investing has been proven effective. Option overlays/wrappers and other solutions on top of passive funds have also gained popularity over the years. The market in the US is at the very different stage and so are the needs.

Both are great for long-term investing. You cannot go wrong.

Nifty500 has delivered slightly better returns than Nifty50 (over 20 years). This is because there’s a mid + small cap component to it.

I’m not sure i understand fully. Since buying ETF’s are like buying stocks - dividends can either be credited to your demat account (like buy stocks) or can be re-invested back in the ETF. If re-invested - the ETF performance will track the TRI (Total Return Index).

Hi

Its great to hear the pros but when we compare the returns with the benchmarks there is a difference of approx 3% or so on lower side , due to high tracking error(i guess) which kills the charm of it.which in total makes it very expensive(expense ratio + difference due to tracking error) .