@VishalJain On a slightly different note, I was curious what kind of educational requirements exist to be working in an AMC? More than regulatory requirements, I’m looking for what the industry wants.

Is a CFA qualification from the CFA institute in the US good for you to hire someone?

Does zerodha nifty largemidcap 250 have dividends? I bought the growth fund and today I saw dividend units credited with buy price as 0. I’m so confused as to what’s going on.

If anyone reading this has invested in zerodha largemidcap 250, I urge you to check your Coin transaction statement as posted above by me. It is showing a dividend credit on 13th Sep. I don’t know if it’s real or not.

Yes, same here. And the dividend amount is also large.

I’m not sure how it happened, but after checking thoroughly, my portfolio is showing the invested value as much lower than the actual investment. However, it seems to be offset by the dividend, making the current value almost the same. Did Zerodha convert my investment into a dividend? @VishalJain@Meher_Smaran

The fund seeks to align its weightage with the underlying index on a daily basis, striving to closely track the index by the end of each trading day. The index itself is rebalanced at regular intervals as defined by the index provider. For the Nifty LargeMid 250 Index, this rebalancing occurs every six months.

We have mutual funds who invest in Corporate Bonds and Gilts. Can such mutual fund invest in Bank Deposits.

There are banks offering varying interest rates, it is a onerrous process of opening an account with each and every bank, doing KYC, maintaining balances. For the banks too, no need to issue cheque book, atm card etc which could reduce cost. Is there any regulatory restrictions that Mutual Funds cannot consider FD as part of the fund constitutent.

Few years back I remember vaguely, Icici Direct, putting out an adv that customers can place deposits in banks using their portal. The FDs could be booked through Icici Direct and will remain in our demat or so. Not sure what happened to that proposal. At that time too, I thought it was a great idea as it eliminates the cumbersome process of opening ac, atm, cheque book, maintaining balance when the fact is to just place FD. Of course you need one to two main bank for all banking services. But this will be great for people who chase interest rate in bank.

Example Suryoday SFB is offering 8.65% for 2 years FD rate. I dont have an account, to avail this rate, I now need to open account do kyc etc. Only purpose is to place FD. If all of them are listed, just like buying ETF, we could place deposits. This would be very convenient and provide flexibility as well.

Is there any regulatory restriction of MF opening FD just like they buy bonds and Gilts. The commission payable will compensate for the MMB that need to be maintained if an account is opened - I guess.

FD is not a good investment for a mutual fund. It’s a fixed rate product with a fixed tenure with penalties on liquidating it.

And all FDs above 2CR are non callable (non breakable) right? With a mutual fund’s AUM, 2CR will easily be achieved.

And for such a big AUM, they won’t get any significant deposit insurance like we retailers do. So they cannot open in SFBs, which is what I think you are referring to. They have to stick to SBI, HDFC and other big banks to ensure safety.

When they get 6-7% p.a. through TREPS and and TBills for periods of time as short as a day or a week, why will they lock their money in a SBI FD for 2 years at 7% ?

FYI, you don’t need a savings account at a bank for opening FD. Small finance banks are offering excellent interest rates. If you’re near a branch or atleast in a city, they’ll come to your home and open FD for you. They complete all KYC, you just have to allocate 20 mins and a cheque.

I have FDs in multiple SFBs without an account. All of them come home and open it for you

With 5L deposit insurance, you can smartly spread a big amount across multiple SFBs and family members and get 8.5-9% p.a.

Corporate Bonds have fixed rate too. So how is it different. I am sure if the fund house prematurely closes, there will be charges.

No it is an option available to the depositor. Non callable have a higher interest rate than regular rates and since it cannot be prematurely closed. It is a customer choice.

I am sure a portion can be assigned to FDs - not all. When we can buy Mutual fund without any guarantees why expect this. I am sure all Corporate Bonds are not in the pedigree of SBI, HDFC etc. but still they do buy based on rating. With Banks capital adequacy could be a benchmark

Do Corporate Bonds get deposit insurance - no - so why expect this. The analyst will assess how good the strenght of the bank is before investing - just like they do credit assessment for Corporates before buying bonds

Gilts are in this range too. I have seen gilts with long maturity.

To the best of my knowledge, you need to open an account and Banks are not allowed to open FD without proper KYC and other documents. Funds to open FD are moved from SB ac and similary when closure happens. I could be wrong. If you know any bank who does this, can you please let me know. I will revert on this later. Personally, will never open a FD without having an account, - there is no audit trail of fund flow.

Can you please recheck and let me know. it would really help me. None of the banks who I talked to have told me this. When I say banks, Banks who are listed in stock market (Psu/private/sfb) and not cooperative banks, regional rural banks etc

This I agree, but how many will open accounts with many banks - I am an exception though. Hence this thought.

The scale at which these small finance banks operate is much lesser than the company issuing the corporate bond. Some of these SFBs are only 1k-10k crore m-cap.

No. I can confirm the same since I have done it multiple times. Just call your nearest branch. These guys are willing to go to great lengths for deposits. They will come after your office hours or any time when you are free.

Yes obviously.

I give my SBI bank account’s cheque to open all bank FDs. After maturity it will come back into my SBI account as expected. Irrespective of where i open FD. This is way better and easier to manage for me personally since I need to keep track of only 1 account.

Umm, you get FD receipt. If you give a cheque it also obviously appears in your statement as being deducted towards the bank. They also deposit TDS etc. Doubt it gets more auditable than this. Not sure how a debit row for a bank FD appearing in the same bank’s passbook is more legit than it appearing in some other bank’s passbook.

In fact it is less legit since the same bank can cook it’s books and cover up any fraud .

Can confirm. almost every small finance bank allows you to do it. They might ask and give you some premium account but just say no. I would suggest you check benefits of the account first. Their savings account benefits are very attractive (interest rates and debit card offers).

All this comes with added risk of course. To my knowledge, the highest rate right now is Unity SFB at 9% for common citizens, 9.5 for senior citizens. But they have fewer branches so you can explore as per your address.

Even if it is far atleast call the bank and ask if they will come home. You can even open it online through apps like “Stable Money” or Wint Wealth. I recommend stable money.

All MF can invest in FD, and lot of them does. Not only debt fund, even equity funds invest in FD. I am sure that is going to make you very happy

You can easily find that out by looking at monthly portfolio disclosure of funds.

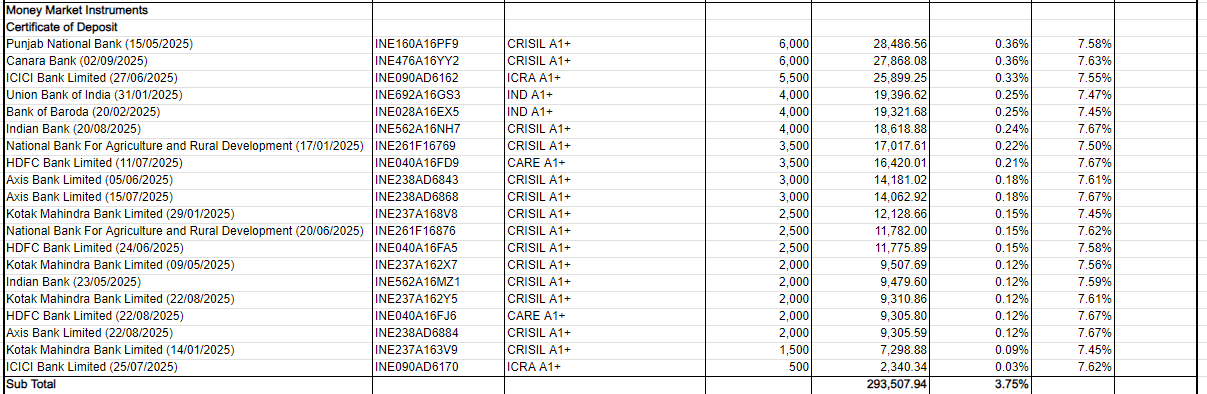

Take eg. of PPFAS flexicap fund. This is their investment on Certificate of deposits for Aug’24.

These are CDs and not really FDs, but practically serve same purpose as FD, with only difference that they are tradeable.

So no there is no restriction on MF investing in Bank Deposits.

Nope. Again something that will make you happy

Most Banks, especially Small finance banks, have gone completely online and you can book a FD online without opening a saving account.

You will still need to do a KYC, as it is a regulatory requirement, but it is fairly easy. Give your Aadhar, sit on a video call for 3-5 mins, and you are done.

In fact lot of Fintech apps have become aggregator for FDs. In past I used Moneycontrol to open couple of FDs with random banks (just to test ) and worked smoothly. And probably got some cashback too.

You will still be required to do Video KYC for each FD, but overall process is pretty smooth.

@Akash_Shah - MF who invest in CD of bank. Should I search for constituents in flexi cap fund? Please advise. @tallerballer - FDs can be opened without having a SB account. I called up few banks and all said they can do it - its called “standalone FD”.

Nah, I just gave an example to show that most MF invest in bank CD.

However their proportion of investment is tiny. Most would be putting in max3-4% of their Asset in CD, not more than that. So if your objective is to invest in MF which invest in bank FD, that won’t be serve.