With rates expected to rise, if the war continues, is it wise to lock up your money in FDs now?

Yes. even if after openeing the FD if rates increase sizably, then you can even close and reopen the same. provided overall it is still beneficial. Also check the SB ac interest rates, those rates also could be higher, for float balances.

it will be good to know whether these FDs offer the usual options for premature withdrawal,

like the effective rate-of-interest would be the rate for the actual period deposit maintained - 1% penalty,

or any other terms and conditions apply? ![]()

A bird in the hand is worth two in the bush

What if they keep hiking the rates over the next few quarters, how long does one wait?

Also, the rates don’t generally increase by more than 25/50 basis points and takes more time for the banks to pass on the same to depositors (unlike lending rates).

If one has already invested in FD, the premature withdrawal penalty is structured in such a way that it deters the depositors from doing it. i.e., in general, the interest rate lost to the penalty is often ≥ to the revised interest rate (hiked).

Also there is a catch, the rate on which the penalty applies is not on the actual FD rate agreed upon, rather the penalty is applied on the interest rate corresponding to the period the deposit was actually held.

Eg: If a FD was made for 5 years at @8% p.a., and you decide to close it at the end of 3rd year. The penalty is applied not on 8%, rather it is applied on the FD rate corresponding to 3 years.

Let’s say the 3 yr FD rate is 7.5%, and a penalty for premature withdrawal is 1%, now actual interest for the 3 year period would be 6.5% (7.5 -1), effectively you are losing 1.5% (8 - 6.5) from your agreed upon interest rate, by trying to chase a new FD with a higher interest rate, which will surely not be more than 0.5% higher than the previous FD rate on most occasions.

In summary, on most occasions, the cost of penalty from a premature withdrawal is higher than any benefit that might come with a rate hike, as the repo rates changes are made in increments of 25/50 basis points, and between rate hikes and the time the it takes for banks to launch new FDs at revised rates, it would take 3 to 6 months, so it would be better to just invest in a short-term FD now, and later switch to a new one at maturity.

if it does not increase then there is no issue. Deposit rate increase everything to do with the Bank liquidity issues. Every bank now is seeking high value deposits over 3 crore due to March year end. These bank are offering 8% plus some non callable as well.

This is the math a depositor needs to do. If it is profitable customer should close if not leave it.

This is not a catch, this is the norm. Obviously no bank will give u rate minus penality if the original deposit was at 5 years and the customer close it at 3 months. It will be 3 months minus penality.

As mentioned rate hikes solely depends on the banks liquidity situation. The repo rates gives an indication that is all.

These rates are not grounded in reality when inflation (3.5%) + rupee depreciation (6.5%) for the last 12 months are factored in. ![]()

Due to the war, the rate of increase of both inflation and rupee dep. are increasing. ![]()

Why should we add these two ?

To arrive at the real return of the investment (FD). ![]()

Market bets on Fed rate hike surge

https://www.reuters.com/business/markets-bet-fed-rate-hike-soon-july-2026-03-20/

India usually follows. Better to go with short duration/overnight.

Still dont get it.

Its one of the two ? From an external point of view, you look at INR vs USD.

From an internal point of view you look at inflation, which may be different that this number as expenses can be different. This might be influenced by USDINR, thats all.

I dont see any logic in adding up the two.

Man, INR really has done very poorly. Inflation probably will follow with some lag. Hopefully post war, we will see some recovery.

Inflation + taxation if paid - FD return could be the real rate of return. INR depreciation will be accounted for in inflation.

the point being in this asset class the capital is protected and you may get a negligible return whereas in equity, you could loose capital.

Although I get where you are coming from, unfortunately, the interest rates in India are intended to compensate only for the inflation in India, if we need protection against depreciation of INR, then we need to diversify by investing in foreign/US bonds or assets. No other choice.

We gotta cut some slack to the Govt on the depreciation of INR. What can we do better, when no matter what we do, the odds are against us.

I’m talking about the system of USD being the reserve currency.

We are playing a game where the scales are tipped/ rigged against us.

If a country’s currency depreciation is proportional to its CAD (current account deficit), then the USD should be falling 2 to 3 times more compared to INR.

i.e., when non-capital inflows primarily determine a country’s currency strength/weakness.

Comparison of Current Account Deficit (% of GDP)

United States: The U.S. traditionally runs a large and steady current account deficit, usually in the range of 2–3% or more of its GDP, driven by high consumption and lower savings.

India: India’s current account deficit has remained well within the “safe zone” in recent years, often falling below 1% of GDP.

FY2024-25: India’s CAD was very low, at approximately 0.6% of GDP.

FY2025-26 Projection: Despite pressures from higher US tariffs, India’s CAD is expected to remain relatively low, projected around 0.9% to 1.3% of GDP

The USD appreciation or stability comes primarily from its Capital account Surplus. i.e., From FDI/FPI/Borrowings etc.

People are willing to invest in the US simply because it is termed a safe-haven, ignoring the fact that, by doing so, they are indirectly contributing to INR depreciation

The US is pretty much stabilizing USD by borrowing money from the rest of the world at a cheaper interest rate.

As long as USD remains as the reserve currency, any country that has a Balance of Payments deficit will see its currency depreciate against the USD forever.

Here is a breakdown of how the USD reserve status creates a structural disadvantage for other nations

Imported Monetary Policy: Countries holding dollars must align their own monetary policies with the U.S. Federal Reserve. If the Fed raises interest rates to manage domestic US inflation, it can cause capital to flee emerging markets, forcing those nations to raise their own interest rates, which can stifle their local economies.

The “Exorbitant Privilege” and Debt: The high global demand for dollars allows the US to borrow at lower costs than other countries, enabling it to finance large budget deficits. Other nations must work harder to earn dollars to secure their trade, while the US can effectively generate them.

Exchange Rate Distortions: The constant, massive demand for dollars often keeps the USD overvalued, making U.S. exports more expensive but also creating an uneven playing field where other countries struggle to keep their currencies competitive, forcing them to accumulate dollar reserves to prevent their own currencies from appreciating too much.

Commodity Pricing and Transaction Costs: Because most global commodities—most importantly oil—are denominated in dollars, countries that do not use the dollar must pay currency conversion costs and bear exchange rate risks to buy essential goods, effectively subsidizing the use of the dollar.

Weaponization of Currency: The dominance of the USD gives the U.S. powerful financial, geopolitical leverage, allowing it to impose sanctions that can cut countries off from the global financial system.

Vulnerability to U.S. Crises: Because the world holds its reserves in dollars, any financial crisis in the U.S. is immediately exported globally. The 2008 financial crisis is a prime example of how reliance on the dollar forced other countries to bear the costs of U.S. financial decisions

PS: Most of our trade deficit is attributable to Crude imports, i recently read a news piece where the US was importing most (80%) of its Crude from the Middle East in the 1970s, now, they are the largest producer of Crude.

IMO, we too have untapped/unexplored crude reserves, it not like they are non-existent.

Hopefully, one day, we can become self-sufficient too and bring some stability to our currency.

Yes, the real rate of return formula uses only inflation but it’s not very useful in a globalized world. ![]()

I think a better term would be purchasing power. ![]()

If I have USD 100 or its equivalent in INR today, which of the following investment would be preferable:

- USD denominated debt of 4% APY

- INR denominated debt of 7% APY

With Indian inflation at 3.5%, US inflation at 3%, and INR depreciation at 6.5% for the last 12 months, the real return my purchasing power at the end of say, 1-yr maturity would be:

- USD debt spent in India: 4 + 6.5 - 3.5 = +7%

- USD debt spent in US (globally): 4 - 3 = +1%

- INR debt spent in India: 7 - 3.5 = +3.5%

- INR debt spent in US (globally): 7 - 6.5 - 3 = -2.5%

This last figure is what I attempted to calculate, though I incorrectly used Indian inflation figure earlier. ![]()

I don’t think USD being the reserve currency is remotely even a valid defense for the government. It’s just a red herring. The depreciation happens regardless of what currency was the reserve. If we take Gold standard, the INR has depreciated proportionately.

Furthermore look at Chinese currency. They do well with their currency and even depreciate it on purpose unlike us. There’s no excuse for the government.

And with Pakistan:

Do we have a product like this in India for resdident Indians - I do not think so. Yes I am aware of LrS and remit and do direct purchase from US etc, but this does not help a retail investor. Yes, NRI have the advantage of openeing FCNR deposits at 4 to 5.30% currently but same not available for residents.

What are the choices that resident retail investor have to edge against INR depreciation. (Affected party - if parents are thinking of sending their children abroad for education in the future)

- Gold - Digital gold purchases is a good option, but the product by itself do not generate anything.

- Invest in USD denominated equity - RBI restrictions has made it not available on a daily basis. ETFs are running at a premium of 15 to 18% to its inav.

- Invest in companies where revenue is in USD like TCS, but the market price has taken out a major chunk of Capital if invested.

What else is there, again for retail investor, please do not tell me to buy direct from USA all this is not going to happen with small capital.

Why not? Compared to dealing with Indian bureaucracy, the entire process is completely online.

How small are we talking? With SBI, flat charges are like 1k rupees.

Yes, we do. ![]()

Am assuming “education” is referring to a bachelors/masters degree in the US.

i.e. something with significant costs in the range of hundreds of thousands of USD.

With the purchasing power parity of ~20x,

a retail investor with minuscule amounts to invest

is unlikely to be able to afford such education in the US.

Not that such an education is inherently worth it.

But that’s a separate discussion that requires additional thought.

Especially including factors other than pure finance/probability, i.e. lifestyle choices.

That quickly transitions the discussion from expected-value to expected-utility.

So, for the purpose of this topic-thread, to each their own.

On the topic of PPP...

On a somewhat tangential note -

when comparing purchasing-power and expenditure in different countries,

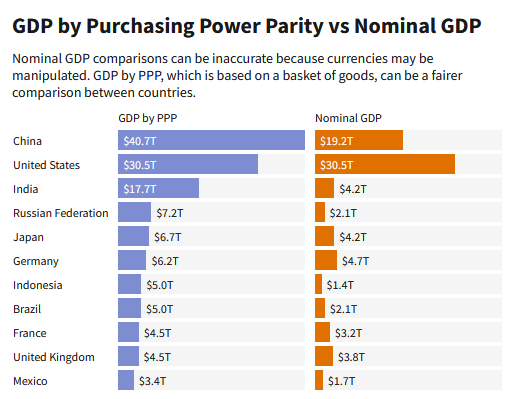

Purchasing Power Parity is another relevant factor to consider.

PPP between the USA and India is hovering around 1:21.

[ Source ]

In other words, on an average, across a bunch of goods and services,

what requires 1 USD in the USA, requires around INR 21 in India.

Here’s a chart that hopefully drives the point home by where India’s GDP appears if PPP-adjusted,

[ Source ]

The fact that the INR is depreciating at 6.5% despite a tiny inflation differential and a massive PPP undervaluation# also implies that the depreciation is being driven by capital flows, risk premiums, central-bank interventions, or a combination of these and other such factors.

# - Not that massively unndervalued, if one accounts for the actual disparity in quality of some of the goods and services involved.

Not all goods and services are ~20-times better in the US.

and even for the ones that are better,

this ends-up being a “forced upgrade and unnecessary additional expense” in the US

if one is fine with the quality of the product/service on offer in India

and that option/operating-point is not availabel in the US.

(A popular example used is “a haircut at a salon” in India and the US.)

So, if one is investing amounts that would enable accumulating sufficient capital to pay for education in the US, then the fixed overheads (exchange-rates, tax-compliance) are nominal and do not wipe-out the additional returns from exposure to USD compared to a depreciating INR.

Is the claim that

Micro-investing is viable domestically,

but the fixed-overheads involved in foreign remittances

make it impractical to do it overseas?

Sure, probably doesn’t makes sense to remit 100 INR daily or 1000 INR each week.

However, maybe can evaluate whether one can continue with one’s domestic micro-investments, and periodically (say once every few months) remit outwards a large enough significant chunk to nullify the fixed-cost overheads involved with outward remittances (say bring them down to <1% transaction-overhead)

Maybe even a couple lakhs depending on how well one can negotiate with the bank.

Ironically, easier for folks with larger capital/cash-flow and a better “relationship” with the bank.

BTW, agreed that the initial experience until one learns the various intricacies involved is full of friction. But, that’s a one-time thing as one ramps-up/learns.