Am assuming “education” is referring to a bachelors/masters degree in the US.

i.e. something with significant costs in the range of hundreds of thousands of USD.

With the purchasing power parity of ~20x,

a retail investor with minuscule amounts to invest

is unlikely to be able to afford such education in the US.

Not that such an education is inherently worth it.

But that’s a separate discussion that requires additional thought.

Especially including factors other than pure finance/probability, i.e. lifestyle choices.

That quickly transitions the discussion from expected-value to expected-utility.

So, for the purpose of this topic-thread, to each their own.

On the topic of PPP...

On a somewhat tangential note -

when comparing purchasing-power and expenditure in different countries,

Purchasing Power Parity is another relevant factor to consider.

PPP between the USA and India is hovering around 1:21.

[ Source ]

In other words, on an average, across a bunch of goods and services,

what requires 1 USD in the USA, requires around INR 21 in India.

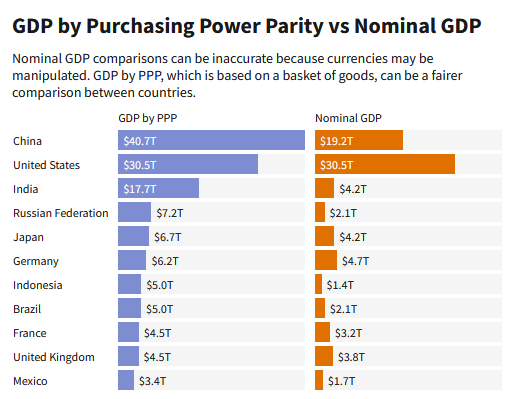

Here’s a chart that hopefully drives the point home by where India’s GDP appears if PPP-adjusted,

[ Source ]

The fact that the INR is depreciating at 6.5% despite a tiny inflation differential and a massive PPP undervaluation# also implies that the depreciation is being driven by capital flows, risk premiums, central-bank interventions, or a combination of these and other such factors.

# - Not that massively unndervalued, if one accounts for the actual disparity in quality of some of the goods and services involved.

Not all goods and services are ~20-times better in the US.

and even for the ones that are better,

this ends-up being a “forced upgrade and unnecessary additional expense” in the US

if one is fine with the quality of the product/service on offer in India

and that option/operating-point is not availabel in the US.

(A popular example used is “a haircut at a salon” in India and the US.)

So, if one is investing amounts that would enable accumulating sufficient capital to pay for education in the US, then the fixed overheads (exchange-rates, tax-compliance) are nominal and do not wipe-out the additional returns from exposure to USD compared to a depreciating INR.

Is the claim that

Micro-investing is viable domestically,

but the fixed-overheads involved in foreign remittances

make it impractical to do it overseas?

Sure, probably doesn’t makes sense to remit 100 INR daily or 1000 INR each week.

However, maybe can evaluate whether one can continue with one’s domestic micro-investments, and periodically (say once every few months) remit outwards a large enough significant chunk to nullify the fixed-cost overheads involved with outward remittances (say bring them down to <1% transaction-overhead)

Maybe even a couple lakhs depending on how well one can negotiate with the bank.

Ironically, easier for folks with larger capital/cash-flow and a better “relationship” with the bank.

BTW, agreed that the initial experience until one learns the various intricacies involved is full of friction. But, that’s a one-time thing as one ramps-up/learns.