I’m transitioning into quant research and hitting a wall with strategy validation. Here’s the paradox I’m facing:

TradingView Backtests show promising results for my Bank Nifty futures strategy, but:

Quant communities aren’t considering it.

Yet every institutional broker (Zerodha, Interactive Brokers) relies on TradingView for charting infrastructure.

When I attempt institutional-grade validation:

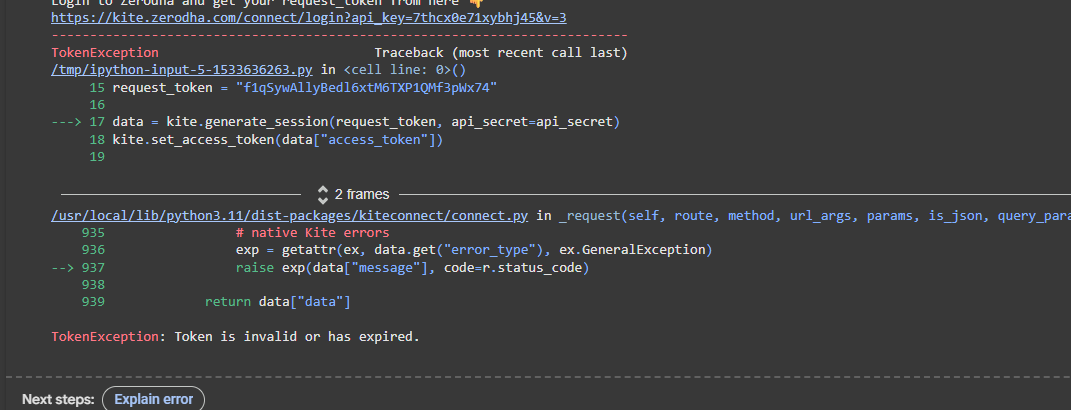

Kite Connect API changes its secret key or something called token/response key every second the moment i add it on code it says invalid key.

NSEpy/YFinance show same error.

Paid alternatives (TrueData/QuantInsti) demand hell lot of money– prohibitive for independent researchers [i am already bankrupt as i lost 1.5 lakhs and my parents and relatives denied help, i earn around 10k per month by doing daily labour & was thinking to get into some quant research job]

Core Questions:

If TradingView’s data is unreliable, why is it the industry standard for charting?

Where do quant firms actually source their India futures data? (Is there a hidden institutional pipeline?)

How are retail traders expected to compete when clean data is paywalled?

I’m fluent in Python/C++ and willing to build pipelines, but need direction on overcoming this data cartel. Any transparency/guidance would be transformative."

The Hypocrisy

Brokers: “Here’s TradingView - the gold standard for charts!”

Unless you are trading very actively, which seems unlikely give high fixed costs, data provided by Zerodha etc is good enough.

I have been trading off that for many years. ofc, data is not perfect, so you have to take that into account. Live trading will be worse, there will some ticks that wont be visible in data, so your stop can get hit in live but not show up in backtest. Edge has to be good enough to overcome all this.

Also make sure to include costs into backtest - taxes etc as well as estimate for slippages. You can start by doubling the costs ie slippage = trade costs. Without this, backtests can be misleading as both upside and downside will become more favorable than reality.

Once you have something, trade it live. No better proof then real results.

Does TV have slippages/fees inputs? Can you download the trades as CSV and run a bunch of other risk metrics? Also futures - are they rolling current month forward to get a continuous chain? Data wise TV should be good (at least for something like BN futures), else I can point you to alternate sources.

bro to arrange capital we should show something to some one who has capital, right? And as i dont have a generational wealth edge, the only way i can arrange capital is to show my backtest/ forward test to some instituiton/ prop desk. I did a mistake trading naked option buying. But does that mean we should stop if we dont have capital, atleast we can try some jobs, my question was that.

its intrady , entry exit within 1 hour and capital used is very less , so chances of slippage is negligible. Also my question is how to get all those [real data or backtester engine which is considered by firms] and from whre.

Lack of trading/coding experience/understanding is clear here. Which is fine, but you must know where you stand.

Slippage is something we cannot just wish away. By slippage i mean impact costs of entry and exits. This can only be avoided with limit orders which have no guarantee of fill ( and missed trades will be profitable as long as order is open )

At some point capital will have to be used, else whats the point ? So backtest must include reasonable slippage estimates ideally from real world data.

yes, dont trade without capital and certainly dont take loans to do that ( just saying because others have done this and lost the loan amount too). If you get a job great, else build up competency/skills for whetever you are interested in. Just because you lost money in trading does not mean you have to recover it from trading only.

More than 98% of traders dont make more than FD over 3 years and more than 90% lose - Zerodha boss himself said so.

Its completely natural then for 3rd parties to not hand out capital easily without clear proof and perhaps references. I have never dealt with them so dunno.

baba ji "Just to clarify — I’m a NISM-certified Research Analyst. check my linkedin for my trade/investment journals …I’m well aware of slippage, impact cost, and the limitations of backtesting. I wasn’t asking for a basic rundown of trading mechanics.

My actual question was about getting help with an API issue I ran into while building a backtester (invalid kite API response key, and seems like it changes after every second), and how to properly structure and showcase strategy results to firms — since most serious players don’t take TradingView backtests seriously. Also, quoting retail failure stats doesn’t reflect institutional/proprietary desk performance — which, as you know, isn’t publicly disclosed. So let’s not generalize.

Would really appreciate if comments were based on reading the actual question — not just assuming I’m clueless and giving generalized advice about retail failure stats. I’m asking about execution and presentation, not trading psychology. @siva

You said slippage doesn’t matter, which i clarified. But anyway …

I am not going to debug for you, but anyway Zerodha api forum is here

I wont take any backtest too seriously unless i did it myself and even here there is tons of doubt until live trading verifies the edge. Anyway, Its unclear where your skills exactly stand, so gave some warnings.

From what limited info i know from someone who trades with prop firms, you need to have a verified edge ( so traded live and made money) and then have a network/reference. Even then you are are basically taking a loan for leverage and need to give a deposit to cover Drawdowns. Only the really well established guys might have risk free capital but they would also get a lower cut of profits.

But i am no expert here and this is from a limited experience of 1 guy. Just saying that it will be very hard for anyone to give capital easily, i certainly would not looking at just a theoretical backtest. Good luck.

Considering that most people lose, its well obvious to consider people as noobs at first. Your replies seemed to suggest that too, but obviously i dont know.

You wanted to know about data accuracy and i gave you answer that its good enough.

Just to clarify — I’m actively interviewing for quant roles, and have had serious conversations with firms who’ve acknowledged I’m in the learning phase but see real potential. Every interview adds to my experience and sharpens my understanding — which is more than I can say for generic forum commentary.

If your takeaway from my question was to throw retail failure stats or explain slippage to me, you clearly didn’t read the post — or worse, didn’t understand it. I was seeking help on an API-level issue and how to backtest/structure strategies in a way that’s presentable to serious firms. Not a motivational lecture from someone who seems more obsessed with sounding right than being helpful.

I came here looking for constructive input from professionals. If you can’t provide that, you’re just adding noise — and frankly, I don’t have time for that.

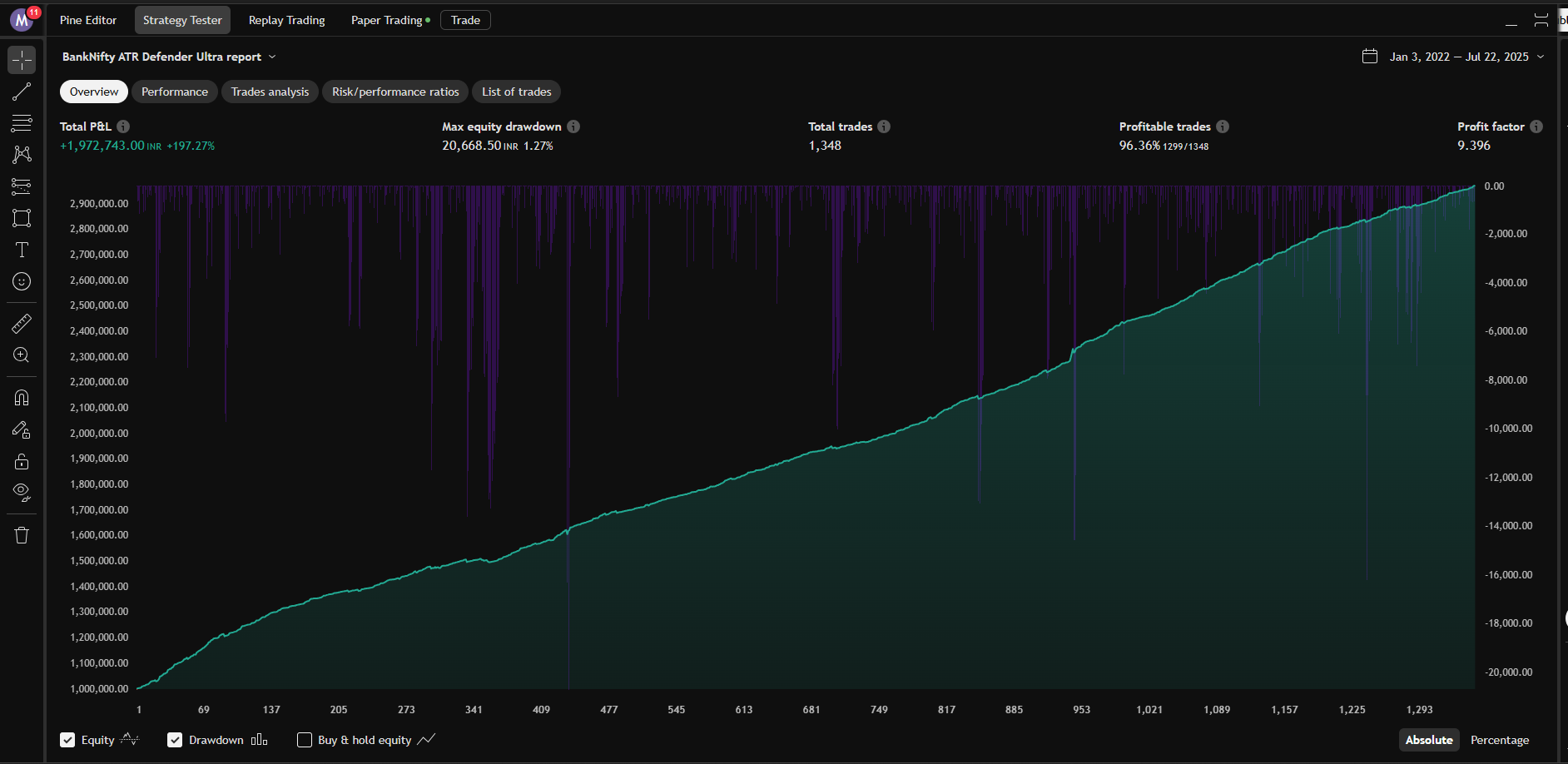

Looking at your backtest image raises a lot of red flags. Real market equity curves don’t work like this in a straight line, certainly not in futures. Something is wrong here.

Soooo many times i have come across people with claims of out of this world system/equity curve and no capital.

Its crazy. Just had another guy say its easy to make 1% per day recently and he also had no capital. Knew i guy who claimed 10% per day easy peasy.

Anyway, Good luck. Look at the api forum for coding related questions.

Thanks for the motivational TED Talk, but your assumptions are way off.

The equity curve was from a quick backtest to test an idea — not some holy grail claim. If you’d actually read the post, you’d have seen I was asking about API issues and how to properly structure and present strategies — not claiming guaranteed profits.

Also, lumping anyone who’s building and learning into the ‘1% per day no capital’ category is lazy and says more about your mindset than mine. I’ve been shortlisted for quant roles, received real feedback from firms, and I’m improving with every interview. That’s progress — not flexing on a forum with snide remarks.

If you’re not here to contribute or collaborate, maybe stop projecting skepticism as expertise. Forums are meant for learning — not for dumping your past disappointments on people who are actually trying.

And where are you getting all this about prop firms taking deposits? Legitimate firms don’t ask for any upfront money. Many of them actually hire freshers, especially for quant researcher roles, based on skill and potential—not capital. Drawdowns are usually limited to your assigned risk, and you’re never personally liable beyond that.

It sounds like your friend might’ve gotten caught up in some kind of scam. In real quant or prop trading roles, you’re paid a salary (or a profit share), not asked to “invest” anything to get started. In fact, Nikhil recently posted a job opening for researchers/data scientists—just check the job description for yourself.

They are probably playing with grey area, but are legitimate from traders pov.

Anyway, that is meant for established traders who need leverage/funding. Option sellers primarily my guess. They don’t advertise so you cant just approach them, dunno how it works exactly but they are brokers i think.

What you are talking about seems to be different, fresher recruitment and then i guess they will train you and assign tasks, more like a normal job and probably a lot more legal.

I am not interested in all this. I trade my own account.

Anyway -

For data, why not ask the firms yourself on what they expect. Data that zerodha/brokers provide is good enough for most of us but with the knowledge that its not tick by tick perfect. Its sampled i think and misses Highs and lows for some bars. Maybe also check with them on what exactly they are looking for, education etc.

For api issue, check docs and check the forum i linked. Its also from zerodha

My strong suspicion is that the backtest equity curve you posted is broken in some way. Take that as you will. Good luck.

Looking at your TV backtest graph, your strategy is likely repainted, and as such very misleading; actually I should probably say ‘definitely’ repainted

If you forward test your strategy, you could find signal shifts on the fly

Massive thanks to @siva and zerodha team — the only group who actually understood the core of my question and helped with real input, including code structure. That’s the kind of response that helps someone build institution-grade systems, not this wave of defensive, insecure noise.

Let’s break this down clearly:

Anuj Sharma — gave a couple of valid points, but looks like he want to help only pros, “dude why will a pro post these kind of things here”.

Spacemanstuff — legit sounds like he’s typing from a rehab center. Claims to be a “profitable trader” yet can’t handle a basic backtest thread without spiraling into conspiracy theories about repainting. Bro, put the vape down and show one real PnL. At some point, the “trust me bro” energy wears thin.

Nair — another rehab keyboard warrior. Didn’t even read the post properly. Just rushed in with criticism, most likely projecting his own trading frustrations. That kind of knee-jerk reaction reeks of someone more upset with their own PnL than mine. Maybe read a few books on behavioral finance before lashing out next time.

And just to set the record straight — I never claimed this was a holy grail strategy. I asked for help setting up a proper backtesting engine and understanding why TradingView backtests aren’t taken seriously. That’s it.

All of you are loud because you’re not used to anyone building anything serious. That’s why your first reaction is mockery — it’s classic insecure energy. The second someone shows actual initiative, you try to drag it down to your level.

So here’s the deal: Post your verified PnL links here if you’re so confident. Let people decide who’s real.

Because from what I’m seeing, all I got was rehab-level takes from people scared of anyone actually trying to build something serious.

And honestly, anyone who’s read even a basic book on psychology can see straight through what you guys are trying to do here.

I’ll keep building. You guys can keep barking. And Yes daily labour is hard — so am I.