No matter what the goal or the duration of it, fixed income allocation (debt) is almost always necessary. But investing in debt instruments for the wrong reasons or with wrong expectations can most often not be disastrous. In the past year or so, we’ve seen this play out in spectacular fashion with IL&FS, DHFL, Zeel, Reliance Home Finance, and others.

The reason for writing this post is to give you some pointers on how to invest in debt instruments without taking on too much risk. These are also the same principles I follow in my investing.

I am not going to talk about goals because those are personal and they are better planned with your financial advisor. If you are a DIY investor, a cursory Google search will throw up some amazing resources. Let’s start with having the right expectations. If you are investing in debt for anything other stability and peace of mind, then you will be extremely disappointed. Using debt instruments to chase returns is just like expecting to have a baby in 6 months, it ain’t gonna happen!

In debt, the more returns you want, the more credit risk you will have to take. Here’s the definition of credit risk

A credit risk is the risk of default on a debt that may arise from a borrower failing to make required payments. In the first resort, the risk is that of the lender and includes lost principal and interest, disruption to cash flows, and increased collection costs. The loss may be complete or partial.

So, in bonds, you have something called credit ratings. Although they are flawed, we’ll sidestep that for a bit. Yields on bonds depend on the riskiness of the bond. Government bonds (G-Secs) are backed by the full faith of the sovereign and hence carry no default. Hence the yields on G-Secs are lowest when compared to other corporate bonds on the risk scale. Here’s an illustration of how this works.

G-Secs are the safest and the riskiness of bonds increases as their credit rating decreases.

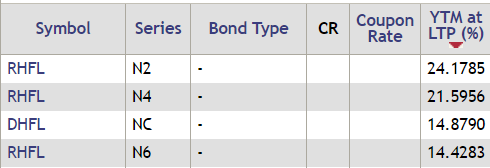

So to simplify, if you are seeing a bond or a debt fund with high returns, then you can be assured that the bond comes carries higher credit risk. For example, here’s a screenshot of a few bonds traded in the cash market.

Look at the yields of Reliance Home Finance Limited (RHFL) and Dewan Housing Finance Corporation Limited (DHFL). Both the companies have been in the news for all the wrong reasons. DHFL’s credit ratings for various debt instruments of the company have been downgraded multiple times since February. RHFL similarly has also seen ratings downgraded.

Now, as I mentioned above, the returns increase with the risk. Since the perceived risk of thee companies has increased the bonds trading will adjust to the news and hence the yields will move higher.

Dumb things investors did in the past year

The past year was a brilliant example of what not to do when investing in debt. I’ll explain this with the example of debt mutual funds. Liquid funds and ultra short-term funds are usually meant for parking funds and meant for short term goals. So the most important consideration when choosing these type of funds shouldn’t be returns but safety.

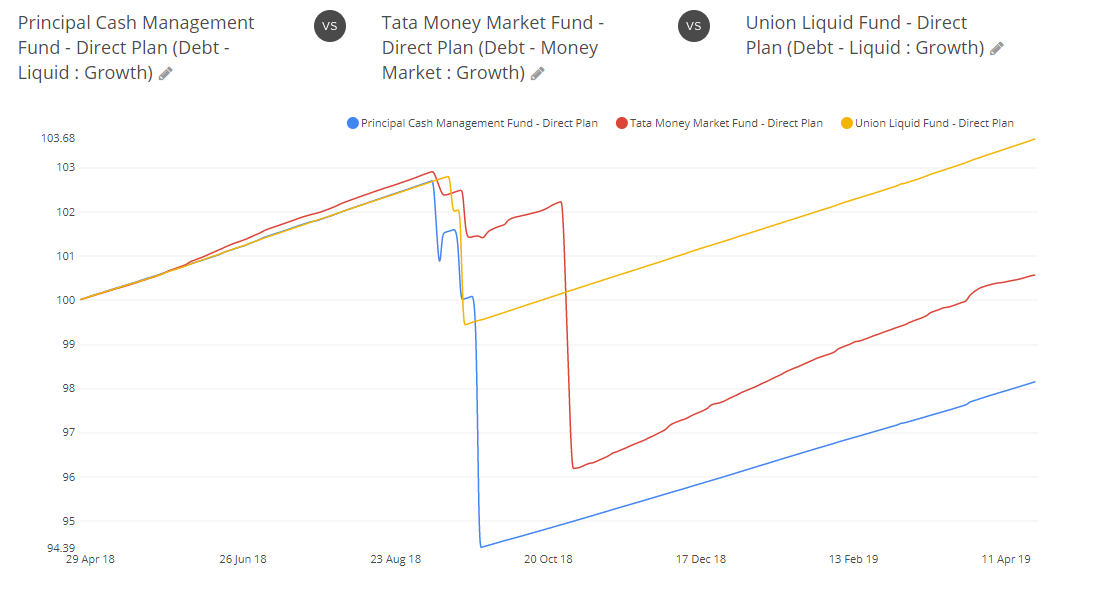

September 2018 was a really good example of what happens when you ignore safety to chase yield in debt. In September, IL&FS defaulted just before the default, ICRA downgraded IL&FS’ long term ratings from AA+ to BB - 9 notches in one go. That’s earth-shattering.

The end result was that from September 2018 to October 2019, some liquid and ultra-short terms funds saw massive drops. In September, Principal Cash Management Fund fell by 5.7% in a single day. In October, Tata Money Market fund has a massive drop of 6% in a single day. To put that in perspective, that is almost a year’s worth of return wiped out in a single day.

Investors were caught flat-footed. As much as investors were guilty of chasing returns, the fund houses were equally to blame. In a bid to attract assets, they choose to take on excessive credit risk to juice up returns in funds that had no reason to take credit risk. For god’s sake, these short term funds were sold as a replacement for Fixed deposits and savings bank accounts.

But when you ignore safety to chase yields, this is what happens.

> More money has been lost reaching for yield than at the point of a gun. - Ray DeVoe

What should you as an investor do?

For starters, have the right expectation - safety and stability over returns. Bonds are used to diversify portfolios and not to generate returns, that what equities are for.

Extra juice

I said that bonds are meant for stability, however, you can earn some extra returns provided that you take on extra risk. For example, you can choose to invest in a bond which is not AAA rated. The lower the rating, the higher the yield.

In case of debt mutual funds, there is a category of funds called “Credit Risk Funds”. These funds have to compulsorily invest 65% of their funds in bonds rated below AA. But you will have to have a high-risk tolerance given that bonds with AA and lower ratings are companies which are having problems and defaults are bound to happen.

In case you are wondering here’s what these ratings mean:

| Rating | Short description |

|---|---|

| CRISIL AAA | Highest Safety |

| CRISIL AA | High Safety |

| CRISIL A | Adequate Safety |

| CRISIL BBB | Moderate Safety |

| CRISIL BB | Moderate Risk |

| CRISIL B | High Risk |

| CRISIL C | Very High Risk |

| CRISIL D | Default |

| Crisil |

Choose the right type of bond/fund for the right goal

Assume that you are parking your money for 4 months, you cannot invest in Gilt fund or a 10-year bond. That would be stupid and in-spite of this, investors choose the wrong category of funds or the wrong type of bonds for their goals.

Understand the risks in bonds

Although the conventional wisdom is that debt is safer, at the end of the day, it’s just that - conventional wisdom. The risk depends on the type of bond, issuer, and duration. Not all bonds and funds are created equal.

A liquid fund has almost no interest rate risk while a gilt fund has the most. Lower the maturity of bonds or debt funds (avg maturity in the case of debt funds), the lower the interest rate sensitivity. The same applies for funds as well.

Know thyself

Know what kind of an investor you are and what risk you can take. If you are a conservative investor, you can stick to T-bills, which mature under one year for short term goals and G-Secs which have maturities ranging for 1-40 years for long term goals.

If you wish to invest in debt funds, then you can stick to Liquid funds and ultra short term funds for short term goals and gilt funds for longer duration goals. Again, not all funds are created equal. As I said above, liquid funds can also do dumb things. If you are picking a liquid fund, it should ideally have as little of credit risk as possible. It is not possible to eliminate completely because there are no funds which purely invest in T-bills (Govt backed).

However, you can look at Quantum Liquid Fund.

We do not take any exposure in private sector corporations and invest only in government securities, treasury bills and highest quality instruments issued by public sector undertakings (PSU) which are shortlisted under our proprietary credit research and review process.

Or other liquid funds which have large AUMs. Reason being, these large liquid funds are used by companies for their treasury management operations. Since they are large, they are also diversified with 100s of bonds and the AMCs have a very high incentive not to mess up by taking one credit risk.

Depending on the duration of the goals, you can also look at investing in Banking And PSU Debt Funds which predominantly invest in banks, both PSU and private.

You can also invest in bonds issued by PSU banks like SBI and PSU enterprises like REC, NHAI, PFC, etc. These bonds are almost as safe as government bonds.

When picking a fund or a bond, concepts such as average maturity and duration are important to understand.

Bond duration measures how long it takes, in years, for an investor to be repaid the bond’s price by the bond’s total cash flows. Using duration, you can estimate how much a bond’s price is likely to rise or fall if interest rates change (the bond’s price sensitivity, and it can be thought of as a measurement of interest rate risk. - Investopedia

Debt funds invest in various fixed income or debt securities and each security in the portfolio may have a different maturity. A bond’s maturity date indicates the specific future date on which an investor gets his principal back i.e. the borrowed amount is repaid in full. Average Maturity is the weighted average of all the current maturities of the debt securities held in the fund. The weights are the percentage holding of each security in the portfolio. Average maturity helps to determine the average time to maturity of all the debt securities held in a portfolio and is calculated in days, months or years. For e.g. a debt fund having an average maturity of 5 years constitutes debt securities held by the fund that, on an average, will mature in 5 years, though individual securities may have maturity different than 5 years. - Mirae

Always read the scheme information document to understand the scheme mandate. Narrower the mandate the better it is for you as an investor. Also, check the previous factsheets to see how the fund has maintained the portfolio consistency. If all this seems like hard work, then you are better off keeping your money in a savings account. Investing isn’t hard, it’s no cakewalk either.

Ok, all this sounds scary. Can I invest in debt without any credit risk?

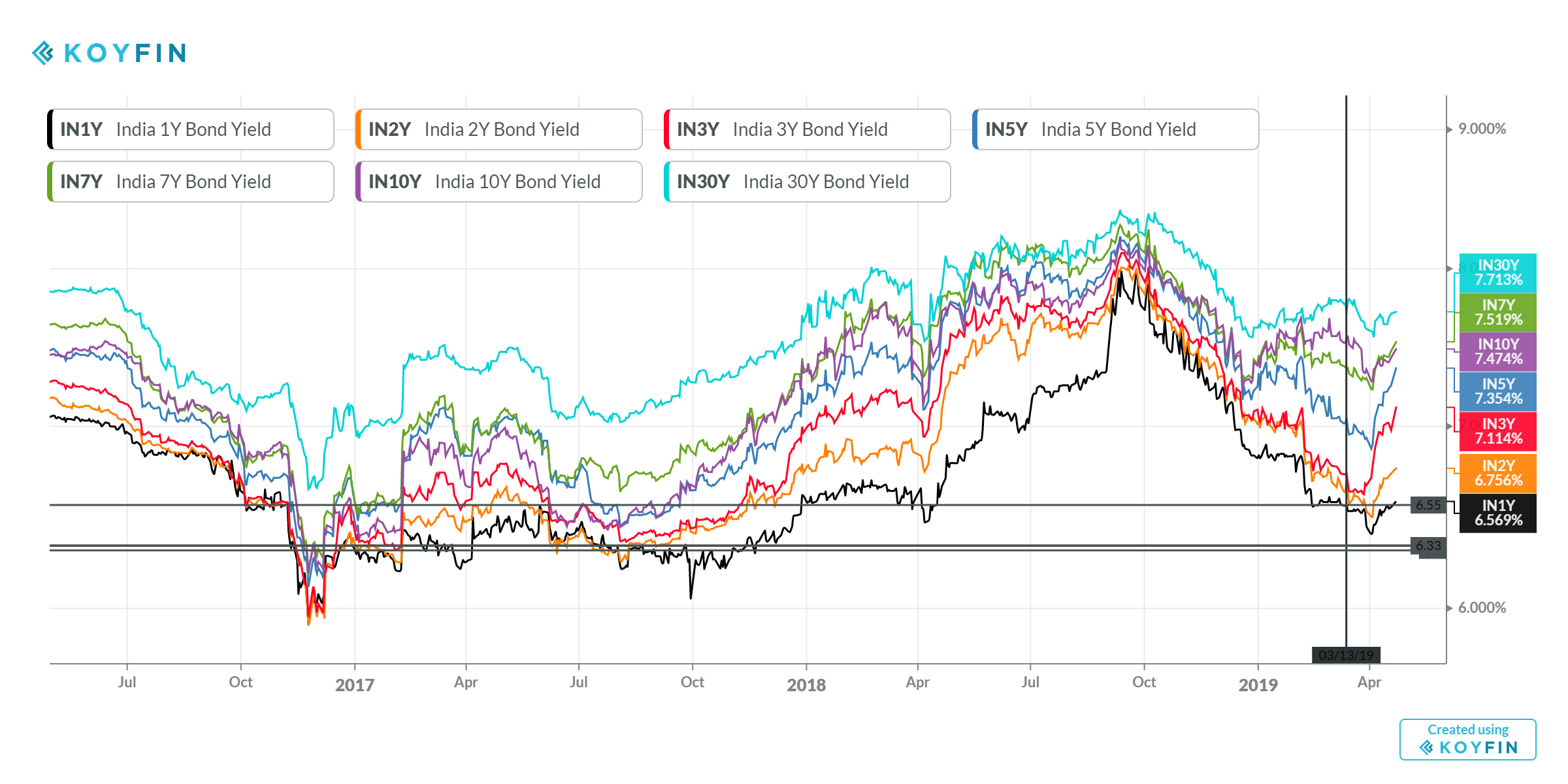

Yes, you can. Government securities - bonds and T-bills are sovereign guaranteed. Meaning they are backed by the full faith and credit of the Indian government and hence carry no credit risk. But in return for the safety, you will lower yields compared to AAA rated corporate bonds. Here are the yields on the various maturities as of writing this post.

Zerodha has made it easy to directly buy bonds from its portal. Alternatively, you can also look at investing in gilt funds (purely for the long term).

Do’s and don’ts

- Ignore past returns if you are investing a fund. Past returns tell you nothing.

- Ignore star ratings. They are purely based on past returns and they are pointless. Principal Cash Management Fund if I am not wrong was rated 5 stars on Valueresearch when it wiped away nearly one year’s return in a single day.

- Always look at the scheme objective, the scheme information document, and the factsheets to determine if the fund is sticking to its mandate.

- In liquid funds bigger the fund, the better.

- Stay away from NFOs and close-ended funds. Stick to open ended funds with established track records.

- Stay away from dynamic bond funds, unless you can time interest rate cycles.

- If you are investing in Fixed Maturity Plans, be very sure or this can happen