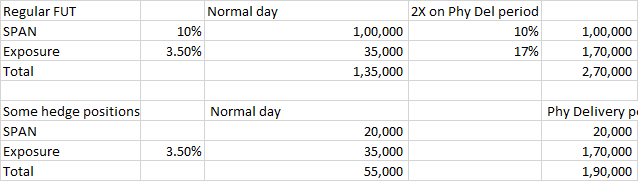

The new margin framework has been live from June 1st, margins for hedged positions have now dropped by almost 70% as compared to earlier. We have been getting quite a few queries on - how much margin have dropped and the most efficient way to enter these types of strategies. So find below an explanation with an example:

Today is June 11th 20200, assume you have a bearish view - Nifty (currently at around 10025) won’t cross 10200 by the end of the expiry (June 25th).

Most retail traders when they are bearish either short futures or buy put options. While these two ways will make you the most money if your view is right, but even the best traders are right maybe only 60 to 70% of the time. Futures and buying options give you no margin of safety and can cause you a large loss when the view is wrong. Here is when shorting or writing options has an edge, while a single trade may not make you tons of money as profits are limited, but a higher margin of safety increases the odds of winning significantly. Please go through Varsity to learn the basics of options.

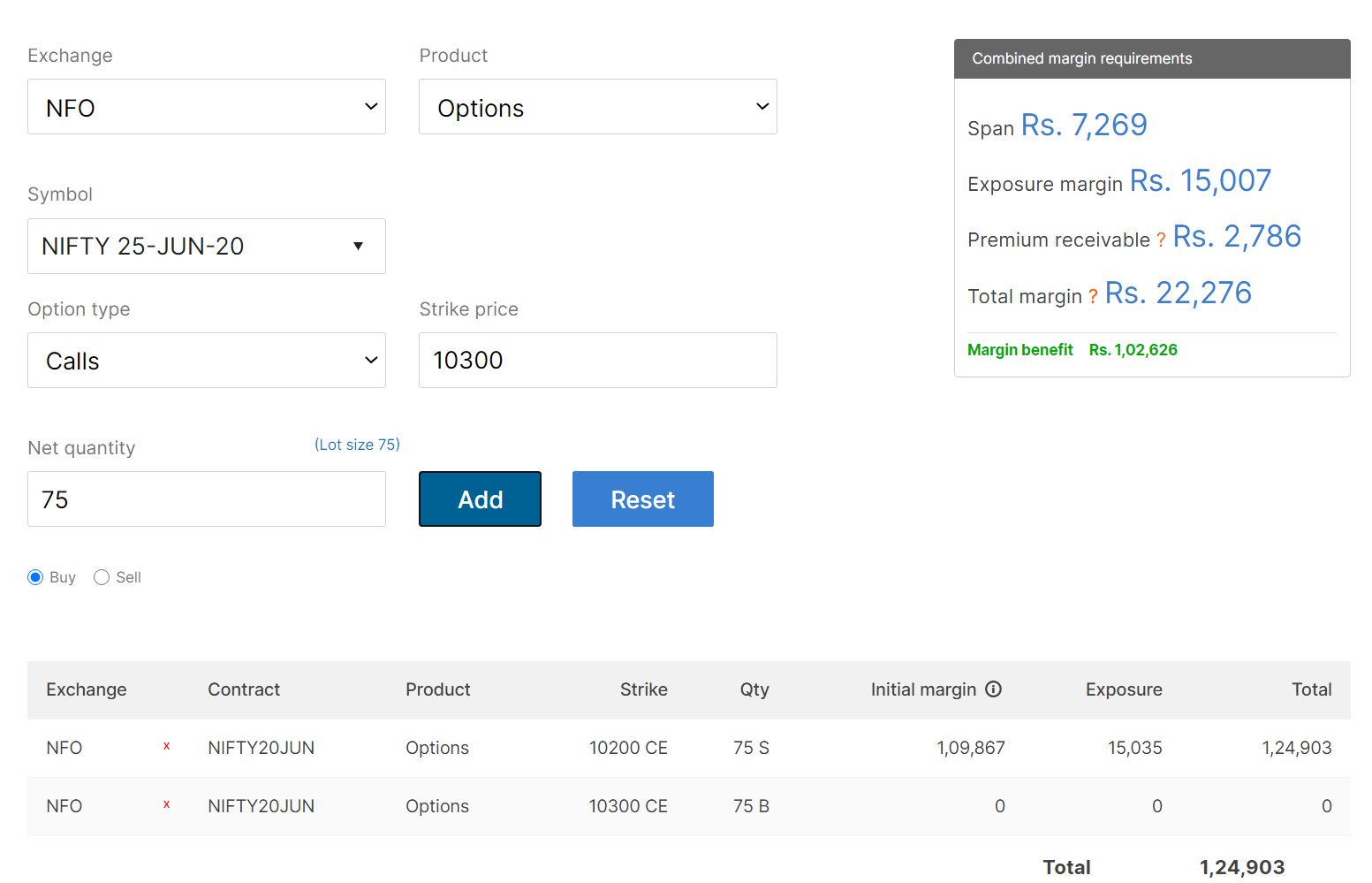

With the above knowledge, a person with a view that Nifty won’t cross 10200 will short 10200 calls which are trading at Rs 132. The margin required for shorting this contract is Rs 1.24 lks. If Nifty stays below 10200, the maximum profit you can make is Rs 132* 75 = Rs 9900. The maximum return on investment is around 9% (9900 on 1.24lks), but the risk here is that your losses are unlimited if Nifty closes over 10332 (10200+132). The fact that you lose money only above 10332 (if you held till expiry) when Nifty is currently 10025 is the margin of safety.

While the odds are higher to win if you short options as compared to futures or buying options, every once in a while a big move in the market can still cause large losses. So a better way to play out the same strategy is to set a spread (Short 10200 calls, but also buy 10300 calls to cover the loss against big moves) and ensure your maximum loss is protected. This strategy of buying an insurance/hedge in the new margin framework have suddenly started making a lot more sense than before, here is why:

Check this payoff for this strategy on Sensibull

The money required for this strategy can be calculated using our margin calculator = Rs 22000 + Rs 8000 for buying options( 10300 calls) = Rs 30000. The margin calculator doesn’t show the buy option premium as it is not a margin, so you’d have to add it separately.

What this means is that even though your maximum profit on this spread is around Rs 2500 (check the payoff graph), much lesser than Rs 9900 when you took a naked short. But the return on investment (ROI) almost remains the same - Max profit of Rs 9900 on Rs 1.25lks investment vs Rs 2600 on Rs 30000 investment. So almost the same ROI as when we short options naked, but with a huge benefit of having an insurance policy, hedging the position from all big moves. This is now almost a no-brainer for people who take slightly longer views (>3 to 5 days) to shift from naked option writing to trading spreads.

Executing this strategy

The margin benefit on this strategy kicks in only after both the positions are taken, so how do you execute this strategy with only say Rs 30,000 in your account?

Clearly if you try placing a 10200 call Nifty order first, it will get rejected as the margin required is Rs 1.25lks and the account has only Rs 30,000.

So, you have to first place the buy option trade.

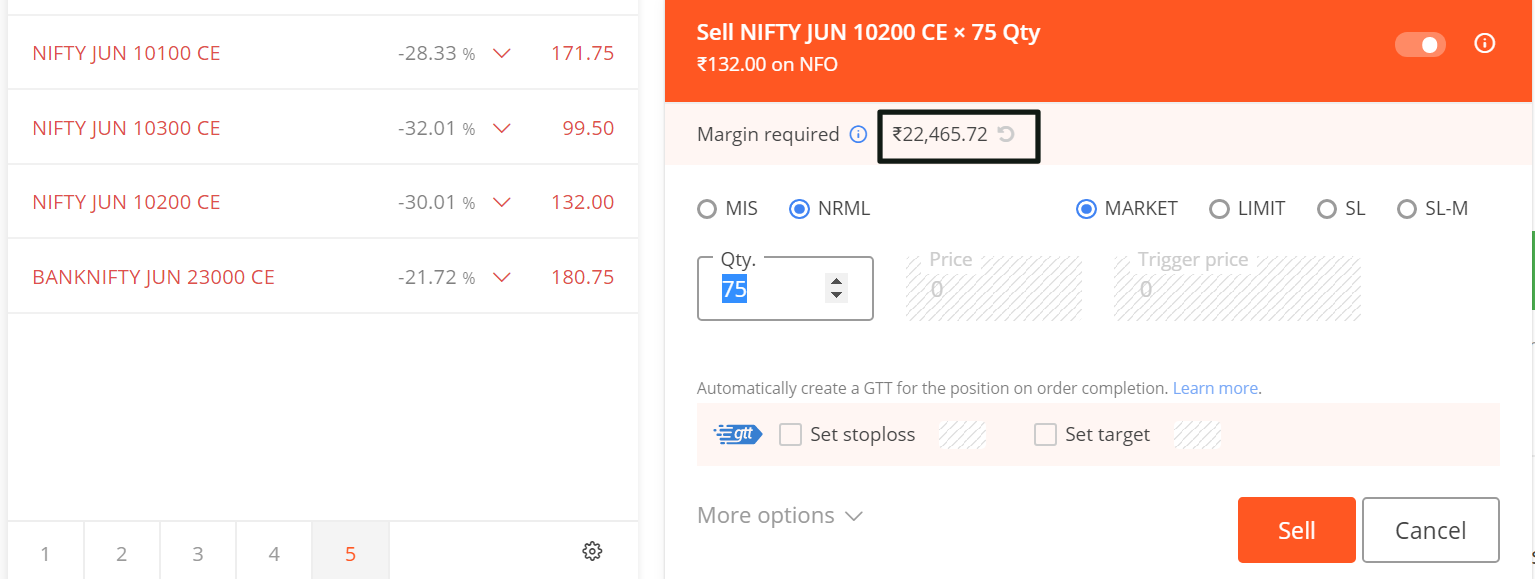

Margin for the sell option trade now reduces to Rs 22k, which would have otherwise been Rs 1.25lks.

Here is the cool bit, once you take this second short option trade, the premium received from this short trade Rs 9900(Rs 132 x 75) gets credited in your account. So technically blocking not Rs 30000, but only around Rs 21000.

One thing to note is that once you have taken the spread position if you try exiting the buy option position first either by placing a pending order or actually exiting it completely, the margin required will shoot up in your account as the position will not be hedged without the buy option position. If the margin required is higher than the account balance, you will get a margin shortfall message from us and our risk management team could potentially square off your positions. To avoid this, when exiting it is best to first exit the short option position and then the buy options.

I hope this is of help, do check out Varsity options module and Sensibull.

Best,