We publish a new episode every day to help you understand the biggest stories in the Indian markets. But we understand that you may be busy and don’t have the time to listen to the daily episodes. So don’t worry, we’ve got you covered.

Every week, we’ll publish a new episode simplifying the biggest stories of the week so that you can still look smart in front of your friends.

Check out the audio here:

And the video is here:

Subscribe on Substack to get this newsletter directly delivered to your inbox:

In this week’s episode, we look at these stories:

-

Adani vs Birla

-

SBI Cards earnings have taken a lunch break

-

F&Oh No!

-

Are the telecom wars over?

-

Love-hate relationship between India and China

-

The world’s coal addiction got a little worse

Adani vs Birla

UltraTech Cement, India’s biggest cement maker and the third-largest in the world (if you don’t count China), is making some major moves. They’re buying a controlling stake in India Cements, which is a big player in South India.

Here’s what’s going on:

UltraTech is shelling out over ₹3,900 crore to buy about a 32% stake in India Cements from the promoters. They already grabbed a 23% stake back in June. With this deal, they’ll own more than 55% of India Cements.

This is huge. It’s going to make UltraTech a dominant force in the fragmented South Indian market, boosting their market share from 12% to 23% in the region.

But this isn’t exactly a new trend. The Indian cement industry has been consolidating for over a decade. In the last 10 years, we’ve seen some big deals:

- Nirma Ltd acquired Lafarge India for ₹9,400 crore.

- Adani bought Ambuja Cement for over ₹80,000 crore.

Now, this latest move puts the Birlas, who own UltraTech, in direct competition with the Adanis, who own Ambuja Cement, ACC, and others. For context, Adani is currently the second-largest player in the cement market.

So, why is UltraTech making this move? There are a few reasons:

- India’s Development: The country is still developing, and we need massive investments in infrastructure—roads, bridges, houses, industries. And all of that needs cement.

- Economic Growth: This infrastructure push is one of the big reasons why India has been one of the fastest-growing economies in the world. In fact, India’s GDP growth over the last 4-5 years has been driven largely by government investments.

- Government Plans: The recent budget includes plans to invest ₹10 lakh crore to provide housing for one crore urban poor and middle-class families under the PM Awas Yojana Urban 2.0.

- Industry Competition: The cement industry is highly competitive and fragmented, with many smaller firms. By consolidating, UltraTech can improve its operational efficiencies.

So, UltraTech’s move is strategic. They’re positioning themselves to capitalize on India’s growth and infrastructure development while improving their own operational efficiencies in a competitive market.

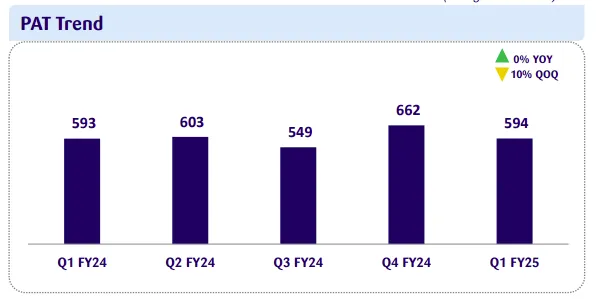

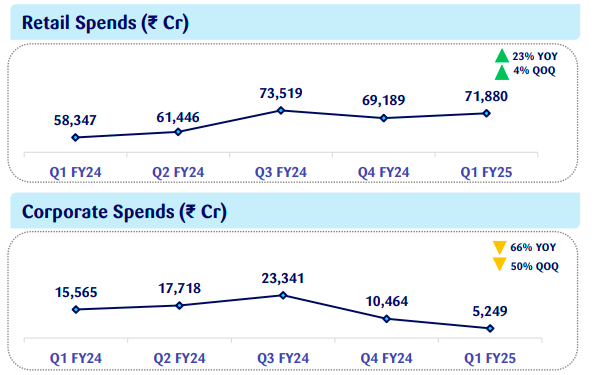

SBI Cards earnings have taken a lunch break

SBI Cards, India’s second-largest credit card issuer after HDFC Bank, just announced their latest results, and let’s just say, they were a bit of a letdown. But there are some interesting trends worth noting.

First off, profits are flat—no growth quarter-on-quarter or year-on-year. Plus, they’ve been steadily losing market share over the last couple of years. That’s definitely not great news.

Corporate spending has taken a hit, thanks to the RBI’s regulatory crackdown. They’ve banned certain types of credit card spends in the B2B space. But there’s a silver lining—retail spending is growing at a healthy pace.

Now, onto the not-so-good news. Non-performing assets, or NPAs, are on the rise. Both stage 2 and stage 3 loans are increasing. Here’s a quick breakdown:

- Stage 1: Loans overdue by up to 30 days

- Stage 2: Loans overdue by 31-89 days

- Stage 3: Loans overdue by more than 90 days

This means people aren’t just missing their credit card payments; many seem to have borrowed more than they can handle. In response, SBI Cards is taking action. They’ve reduced limits on 5 lakh credit cards this quarter after cutting limits on 15 lakh cards in the previous quarter.

But here’s the thing—this rising bad loan trend isn’t just an SBI Cards problem. It’s happening across the industry, especially in unsecured retail lending.

Now, let me share some interesting tidbits from a Kotak Research report:

- Out of all the money people owe SBI Cards, 62% is earning interest. That’s good news for SBI Cards because they’re making money off those outstanding balances.

- The share of new accounts from salaried individuals dropped from 79% in 2021 to 68% in 2025. Meanwhile, the share of self-employed individuals has gone up from 21% to 32%.

- The share of cards in Tier 3 cities has exploded. It was around 10% at the end of 2021, and now it’s about 30%. That’s a pretty significant jump.

So, while there are definitely some challenges, there are also some bright spots and shifting trends worth keeping an eye on.

F&Oh No!

SEBI has been getting pretty concerned about the number of people losing money trading futures and options (F&O). Last fiscal year, a staggering 92.50 lakh unique investors traded in index derivatives, and a whopping 85% of them ended up with net trading losses. That’s a huge chunk of people not doing so well in this space.

In response, SEBI formed a committee to come up with recommendations on how to reduce this speculative trading. The committee’s suggestions led to SEBI publishing a consultation paper just yesterday. Here’s what they’re proposing:

- Limiting Weekly Options Contracts:

- Currently, you can trade six weekly options contracts on multiple indices, like Bank Nifty (expires on Wednesday), Nifty (Thursday), and Sensex (Friday).

- SEBI wants to restrict these weekly options to only major benchmark indexes per exchange. So, for example, only Nifty and Sensex might have weekly options, while the rest will switch to monthly expiries.

- Calendar Spread Benefit Changes:

- If you hold two options on the same index but with different expiry dates, you currently get a margin benefit, known as a calendar spread.

- SEBI proposes that on the expiry day, the margin required will increase by 1-3% of the contract value. This could mean higher costs for traders on that day.

- Increasing Contract Sizes:

- The last review of contract sizes was in 2015. Since then, markets have grown a lot.

- SEBI suggests increasing contract sizes by about three times. So, the value of an index derivatives contract, currently between 5-10 lakhs, might be bumped up to 15-20 lakhs initially, and then to 20-30 lakhs after six months.

These changes are significant and aim to make F&O trading a bit less attractive for retail investors who might not fully grasp the risks involved. SEBI’s goal here is to reduce the number of people losing money by curbing speculation and making sure those who do trade are better prepared for the potential pitfalls.

Are the telecom wars over?

Before 2010, telecom was one of the hottest sectors in India. Everyone, including the biggest industrialists, wanted a piece of the action. But soon, it became clear that telecom is a capital-hungry industry, and over the next decade, we saw a lot of players fall by the wayside.

Remember Uninor, Tata-DOCOMO, RComm, and Aircel? They all either got acquired or shut down. Today, the telecom industry is dominated by just Bharti Airtel and Reliance Jio. There are a few other players like Vodafone-Idea, BSNL, and MTNL, but they’re struggling with all sorts of problems.

Interestingly, telecom stocks were some of the worst-performing investments over the last decade. But things are slowly starting to change now.

The last big shakeup in the sector was when Reliance Jio entered the market with its free plans. Thanks to its aggressive pricing, Jio quickly gained market share, mainly at the expense of Vodafone and BSNL. Today, Jio and Airtel are the only dominant players left.

Can you guess who was the market leader back in 2018? Believe it or not, it was Vodafone! They had a market share of close to 35%-40% of mobile subscribers. But due to the rise of Jio and Airtel, Vodafone’s share has now fallen to less than 20%.

Vodafone-Idea could never get its act together. With massive investments in spectrum and the pricing wars initiated by Jio, they accumulated a ton of debt and couldn’t keep up with Airtel and Jio. They were saved by a bailout from the Indian government. Things got so bad that they started paying their suppliers with shares instead of cash!

Recently, S&P published a report on the telecom sector with some interesting insights. Now that Jio and Airtel are the main players left, they can focus on improving their financials instead of constantly fighting price wars.

Telecom is a capital-heavy sector, and both companies have already invested heavily in rolling out 4G and 5G services. Any increase in tariffs will now directly improve their profitability. Jio took the first step and announced a tariff hike, soon followed by Airtel and Vodafone-Idea, with prices going up by 10% to 25%. This is the first significant across-the-board price hike since November 2021. Now, their focus is on generating more revenue per user.

Sunil Bharti Mittal, the Chairperson of Airtel, said in an interview with ET: “We have spent nearly Rs 80,000 crore on 5G spectrum and rollout. Our competition has spent more than Rs 100,000 crore and there are no additional revenues as you know. So, the time has come now to start to rationalize and repair tariffs.”

He also said: “I think we are heading towards an ARPU of Rs 300, and I hope it happens within the coming financial year, which we are entering from April 1. We need more investments into fibers, infrastructure, and rural areas.”

While price hikes can lead to some customers dropping their plans or switching to cheaper options, data consumption habits are generally sticky. Once a customer gets used to certain data usage levels, they are likely to continue using similar amounts of data even if prices go up.

Just to put it in numbers: During the March quarter, people used over 5,000 crore GB of mobile data. That’s almost double the amount of data used three years ago!

One interesting insight about the telecom sector is that every Rs. 10 increase in ARPU will translate into an annual EBITDA boost of over Rs. 2,500 crores for Bharti Airtel and over Rs. 3,000 crores for Reliance Jio. The telecom companies expect ARPU to keep rising as they implement more tariff hikes. These higher ARPUs will help them recover their investments in network infrastructure, including the recent rollouts of 5G services.

Interestingly, the government has been forced to help the smaller telecom players to keep them afloat. MTNL, another struggling company, was about to default on bond interest payments a few weeks ago, and the government had to step in to cover it because of a guarantee.

Last year, the government approved a massive rescue package worth more than Rs. 80,000 crores to boost BSNL’s 4G and 5G capabilities. They’re doing everything they can to keep these smaller players from going under.

Love hate relationship between India and China

Last week, I talked about how India wants to be friends with China again.

India and China have had a pretty rocky relationship since their border clash in 2020. But it looks like things are starting to improve. While India still wants China to sort out the border issues, it also needs Chinese technology and investments to boost its industries. Despite all the push for “Make in India,” the reality is we can’t manufacture everything at home. Whether we like it or not, we will have to rely on China for some things.

But here’s the twist—yesterday, Piyush Goyal, India’s Commerce and Industry Minister, poured some cold water on this by saying there’s no plan to support Chinese investments, despite what the Economic Survey suggested.

Even though Chinese investments in India are tiny—just 0.37% of total FDI since 2000—our trade with China is massive. China is our biggest trading partner, with trade worth more than ₹9,70,000 crore last year. We sell them iron ore, cotton, spices, and veggies and buy a lot of electronics and machinery from them.

The political tensions remain high, but there are some selective areas where things seem to be getting better. There’s a growing recognition in the government that they can’t ban everything from China. Like it or not, we need to work with China.

For example, Indian solar companies like Tata Power Solar, ReNew Photovoltaic, and Avaada Electro need Chinese experts to help them scale up their operations and meet our renewable energy goals. They are asking for visas for Chinese engineers and technicians who are crucial for their projects. Tata Power, for instance, is investing Rs 3,000 crore in a new solar manufacturing plant in Tamil Nadu and needs these experts to get it done. Without their help, projects could be delayed.

Interestingly, the Economic Survey suggested that partnerships between Indian and Chinese companies could be a good idea. These joint ventures (JVs) would let Chinese firms get around US restrictions by making goods in India and then exporting them to the US, taking advantage of India’s better relationship with the West.

But setting up these partnerships isn’t without its problems. Manufacturing in India is more expensive than in China. We also lack the necessary technical skills, infrastructure, and extended ecosystem. Plus, we have visa and import restrictions that don’t help.

To make these joint ventures work better, India needs to lower tariffs, improve the Production Linked Incentive (PLI) scheme, and make it easier for businesses to operate. By doing this, we can make these partnerships more attractive and boost our manufacturing capabilities.

So, even though there’s tension on the political front, economic needs are pushing for cooperation. Let’s see how this story unfolds in the coming weeks.

The world’s coal addiction got a little worse

In 2023, the world will hit a peculiar milestone. We generated a record amount of electricity globally from coal, yet managed to reduce coal’s share in the world’s power mix from 35.7% to 35.4%. This reduction might seem minor in absolute terms, but it’s a significant indicator that the world is starting to acknowledge climate change and is making moves to address it.

Today, I want to delve into this global shift from coal.

There are numerous reasons for the world’s transition away from coal, but two key factors stand out:

-

Coal produces the most carbon dioxide per unit of energy compared to other fossil fuels. This is extremely harsh on the environment. In 2021, coal-fired power plants were responsible for more than 20% of total global greenhouse gas emissions. If we are to prevent the total collapse of our planet and possibly humanity, eliminating coal-based power is non-negotiable.

-

Air pollution, significantly driven by coal-based power plants, kills one in 10 people. Transitioning away from coal could save millions of lives and increase economic productivity by maintaining a healthier population.

Developed countries have made notable strides in reducing coal usage. In just one year, the US saw coal generation fall by 19%, and the EU experienced a 25% drop. This decline is largely attributed to the rise of renewable energy sources like wind and solar, improvements in energy efficiency, and other technological advancements.

However, the story is quite different in developing nations. In 2023, China, the world’s largest coal consumer, increased its coal-fired generation by 5.9%. India, Vietnam, and Mexico also saw significant increases. The primary reason? Severe heatwaves and uneven monsoons, exacerbated by climate change, affected hydropower generation, a crucial part of these countries’ energy mix. As a result, they had to substitute the lost hydropower with coal-generated electricity.

Under normal circumstances, the addition of clean energy in 2023 would have reduced fossil fuel generation. However, the shortfall in hydropower led to an increase in coal generation, causing a 1% rise in global power sector emissions. Notably, 95% of the rise in coal generation occurred in four countries severely impacted by droughts: China, India, Vietnam, and Mexico.

Source: IEA

Interestingly, despite being the largest consumer of coal, China is also a global leader in renewable energy deployment, from electric vehicles to solar power. India, too, has set ambitious targets for clean energy growth in the coming years, following China’s example.

Source: Our World In Data

The main discussion isn’t about whether countries like India and China can transition away from coal, but how quickly this can be achieved without compromising their development goals. Transitioning from a source that constitutes a third of the global energy mix is a monumental task, compounded by significant human and economic costs.

Most developing countries can’t transition away from coal simply because they can’t afford alternative energy sources. Even if they did, solar and wind alone can’t meet all their energy needs. The only viable clean alternative is nuclear energy, which is expensive and has a controversial history due to incidents like Chernobyl and Fukushima. Financing remains the biggest challenge, as poor and developing countries lack access to affordable funding to go green.

Source: IEA

Despite these challenges, the benefits of moving away from coal are immense. Preventing millions of deaths caused by air pollution would not only save lives but also boost economic productivity through a healthier population.

Let’s hope we can collectively get our act together and stop harming ourselves and our planet. The shift from coal is not just necessary; it’s urgent. With the right support and global cooperation, we can make this transition a reality and secure a healthier, more sustainable future for all.

Source: Our World In Data