While we wait for @zoomtrader and others to share their views,

let me take a stab at it since i am here and have nothing better to do, right now.

Neither.

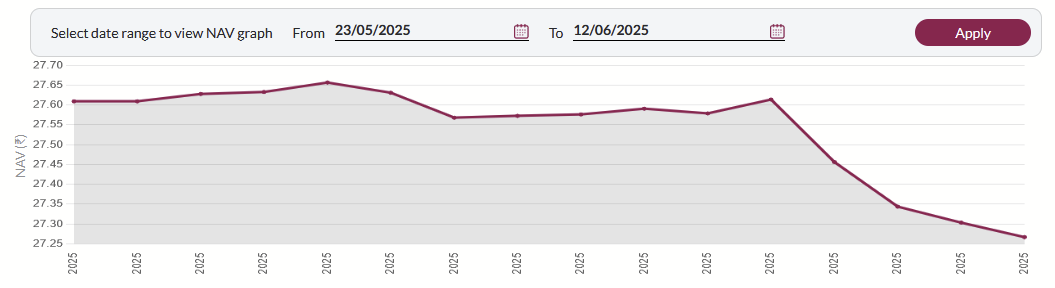

Looking at the current holdings of these debt mutual funds,

the drop is the NAV of the debt mutual-funds discussed in this topic-thread

is due to the drop in the traded price (on the secondary markets - NSE, BSE)

of atleast some of the constituents (GSECS and SDLs) of these debt mutual funds.

Since the NAV of these mutual-funds is marked-to-market,

the NAV drops irrespective of the fact that

the future cash-flows…

- periodic fixed interest payments

- fixed principal repayment upon maturity

…associated with the underlying bonds if held to maturity continue to be the same.

The lower NAV of these debt mutual funds reflects the expected lower price if the underlying assets were attempted to be sold in the market today.

Note that some of the underlying GSECs and SDLs of these specific mutual funds are illiquid and their recent LTP (which is being used to calculate the NAV) is NOT an indicative price if one were to actually attempt to sell such illiquid instruments in the secondary market. Marking to market a debt-fund’s NAV using LTP of the underlying illiquid bonds, is a “least wrong out of the various available options” approach to evaluate a debt fund.

No. The recent change in repo-rate announced by RBI has no impact on the interest that these fixed-coupon GSECs and SDLs pay-out. Irrespective of any changes to the prevailing RBI repo-rate, these fixed-coupon securities will continue to pay-out the exact same rate-of-interest until they mature.

In fact, conventional wisdom states that,

when repo-rate falls, existing bonds will increase in value,

i.e the NAV of debt funds holding such bonds should increase.

Here's the *chain of logic* behind the above conventional wisdom -

-

Repo-rate reduced.

-

The cost of borrowing from RBI is reduced.

-

All subsequent fund-raising using debt instruments will be cheaper.

- why? Because if a lender gets their funds from RBI cheaper (due to 2 above), they can afford to lend at cheaper rates while retaining their margin.

-

Even sovereign bonds (Govt. borrowing using GSEC/SDL debt instrument) is cheaper

- Any GSECs/SDLs issued now are expected to have lower interest-rate/coupon-payments.

-

Any previously issued GSECs/SDLs having higher interest payments are now more attractive to hold as they pay more interest than currently issued GSEC/SDL.

eg. Consider a 10yr GSEC issued in 2020 vs. a 5 year GSEC being issued now,

- the issuer is the same = same sovereign risk.

- whichever offers a higher coupon rate = higher return at the same risk.

-

Increased demand for previously issued GSEC/SDL results in higher prices for them until the YTM (effective rate of return) is similar to the rate of return current GSEC/SDL.

-

The increased price at which previously issued GSECs/SDLs were traded, result in a higher NAV for any Debt mutual funds holding them.

Debt mutual funds expecting a repo-rate cut would have deployed a Duration strategy i.e. invested in bonds that are maturing in the distant future, whose prices are expected to be the most significant to increase following a repo-rate cut,

For more details of the math/accounting behind this,

checkout Duration sensitivity and Present value of future cash flows.

So,

in the light of the repo-rate drop announcement by RBI

contrary to conventional wisdom,

why did the NAV of popular debt funds fall?

One aspect to check is whether the current unexpected LTP of the underlying illiquid GSECs / SDLs is backed by any significant volume/number of trades. If not, then the current NAV is based on an anomalous trade and will soon be righted. However, this is not trivial to determine unless one is already monitoring the underlying debt instruments on the secondary market. This is what was alluded to earlier in this topic-thread -

If sticking with conventional wisdom, one would wait for the next upcoming sovereign bond issue, and if as expected they end-up with lower yields, one would then expect the previously issued GSECs/SDLs held by these debt mutual funds to recover their value due to increased demand at higher prices. Probably this is what was being alluded to by this comment. (or maybe other aspects exist that i am overlooking).

However, that is NOT a guaranteed scenario.

If the overall demand for debt itself reduces, due to a significant shift to equity from debt (Which BTW, is also one of the expected outcomes due to the current change in RBI’s stance and expecte increase in inflation in the near term), then the lower prices of these debt instruments (and lower NAV of debt mutual funds holding them) will stick around for longer, until some of the macroeconomic factors change. But, at this point, we are in pure speculation territory.

Coming back to reality,

If one has the patience and know-how to review the price-history, traded-volumes, ask-bids history of the constituent GSECs and SDLs of the debt mutual funds discussed in this topic-thread, then there is potentially some money to be made in the near future. Potentially.

References: