Welcome to the midweek edition of The Long and the Short—a show where you can expect an honest take on trading. Something you won’t hear elsewhere. I’m Sandeep Rao.

Somewhere on the internet right now, there is a market where people are placing real money bets on whether a particular Indian political party will win a state election. Or whether India’s GDP growth will cross a particular threshold this year.

And here’s the twist — none of this is happening in India. The platforms running these betting markets are based in the US. The traders placing these bets — well, nobody quite knows where they are. Indian law doesn’t allow us, its own citizens, to participate. And yet, these events being priced, the outcomes being speculated on, are all of direct relevance to India.

This is the world of prediction markets. And whether you and I can legally participate in them or not, they are already thinking about us.

This edition is about what prediction markets are, where they came from, the extraordinary intellectual foundation behind them, the billion-dollar battles being fought over their legality, and most importantly, what all of this means for India and for us.

What is a Prediction Market?

A prediction market is a venue that lets you place a bet on a specific future event — but with one important condition. The event has to have a clear, verifiable outcome. It can’t be vague. It can’t be open to interpretation. It has to be something where, on a particular date, the world can look at the result and say: yes, this happened, or no, it didn’t.

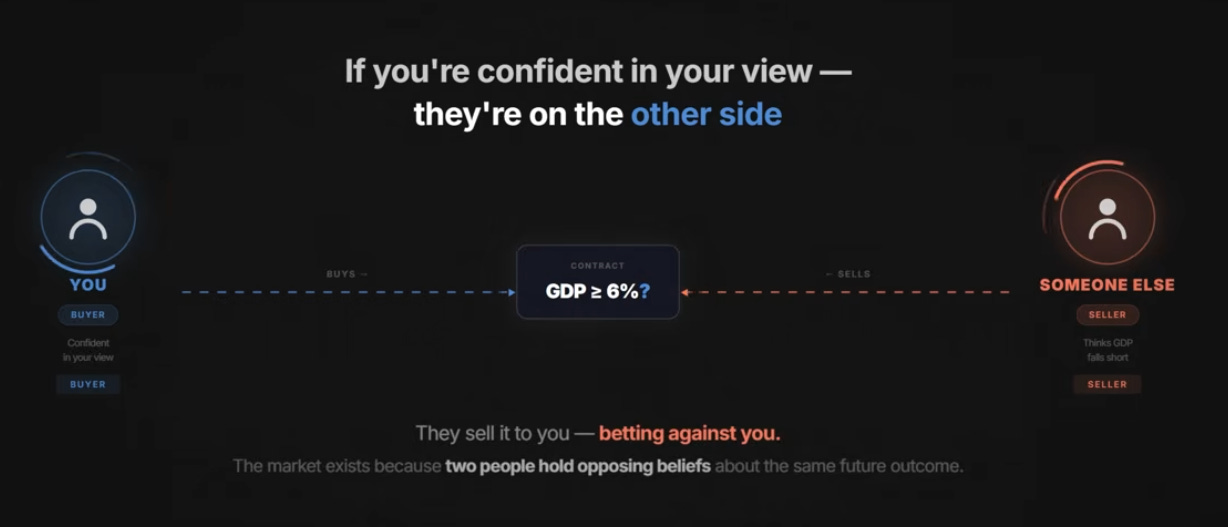

Take an example. Suppose you believe India’s GDP growth will come in at 6% or more in the coming year. In a prediction market, that gets structured as a simple binary contract — a contract that pays you ₹100 if GDP hits 6% or above, and pays you nothing if it doesn’t.

If you’re confident in your view, you buy that contract. If someone else thinks GDP will fall short, they sell it to you, betting against you.

How is the opening price determined? The platform — say Kalshi or Polymarket — looks at all publicly available information on that question: historical GDP trends, RBI forecasts, IMF estimates, whatever the consensus is. And based on that, they set a starting price — think of it like an IPO price, set before trading begins, reflecting everything the world already knows. Let’s say the opening price is ₹50.

From there, the crowd takes over. Buyers and sellers, each acting on their own private information and judgment, eventually find a balance. Let’s say at ₹63.

Here’s the simple math: the contract pays ₹100 if you’re right. If you bought it at ₹63, your potential profit is ₹37. Your potential loss if you’re wrong is the ₹63 you put in. One way to read it is that the market is implying a 63% probability that GDP hits the target — because ₹63 out of a possible ₹100 payout is simply 63%. The price is the probability, expressed in rupees.

One more thing worth clarifying: does every contract open at ₹50, like a coin flip? Not at all. ₹50 would only be the opening price if the event is genuinely uncertain and nobody has any prior edge. If public information already points strongly in one direction — say, a very popular incumbent contesting an election they’re widely expected to win — the platform might open that contract at ₹75 or ₹80 straight away. The opening price is always anchored to what the world already knows. What trading does is refine it further, incorporating everything the world is still learning.

A Very Human Impulse

Betting on future outcomes is not a modern idea. It’s not a Wall Street idea — or even an American one. It goes much further back. In many ways, it’s deeply human.

The moment we became capable of imagining the future — of asking “what will happen next?” — the natural follow-up was: “how confident am I?” And the moment two people had different answers to that question, the conditions for a bet were created.

The Greeks wagered on the outcomes of the Olympic Games. The Romans bet on chariot races at the Circus Maximus. In medieval Europe, people speculated on wars — who would win, how long they would last — and even on harvest outcomes. Closer to home, we have the Mahabharata. The game of dice between the Pandavas and the Kauravas is one of the most consequential wagers in Indian mythology. The reason that the story has endured for thousands of years is not just the scale of its consequences, but the emotion behind it. The feeling of being so certain about something that you’re willing to stake everything on it.

That impulse — to put something real behind a belief about the future — is deeply, almost uncomfortably, human.

But historically, there has always been a moral lens applied to gambling. For most of human history, it was viewed as a vice — something to be regulated, taxed, banned, or at best, tolerated quietly. The framing was almost always negative. So much so that even participation in equity markets is sometimes dismissed as “jua” in more conservative settings in India.

But over time, that perception has evolved. People have come to recognise the value that capital markets bring — to entrepreneurs, to the economy, and to society at large. Markets serve as mechanisms for capital allocation, and when regulated well, they become a net positive. And in many ways, something similar is now beginning to happen with prediction markets.

The Intellectual Foundations

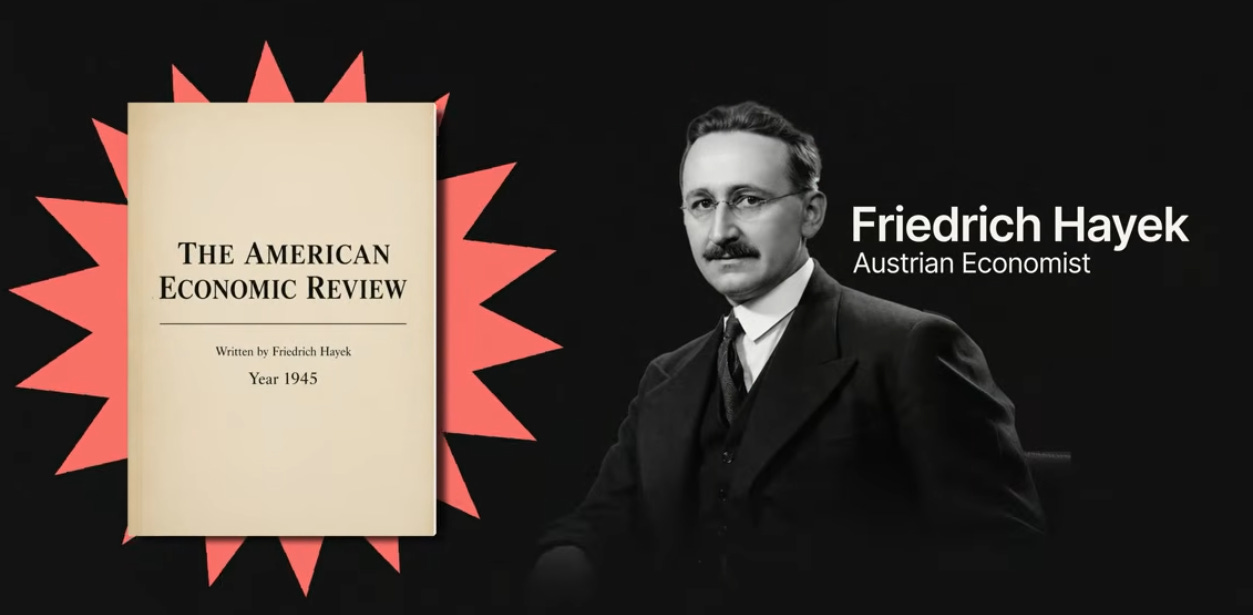

Friedrich Hayek — The Use of Knowledge in Society (1945)

The story starts in 1945, in the pages of the American Economic Review, with a short paper titled “The Use of Knowledge in Society” by the Austrian economist Friedrich Hayek. It’s worth reading — short and clear, and it may change how you think about information flows. Apparently, it was also this paper that inspired Jimmy Wales to found Wikipedia.

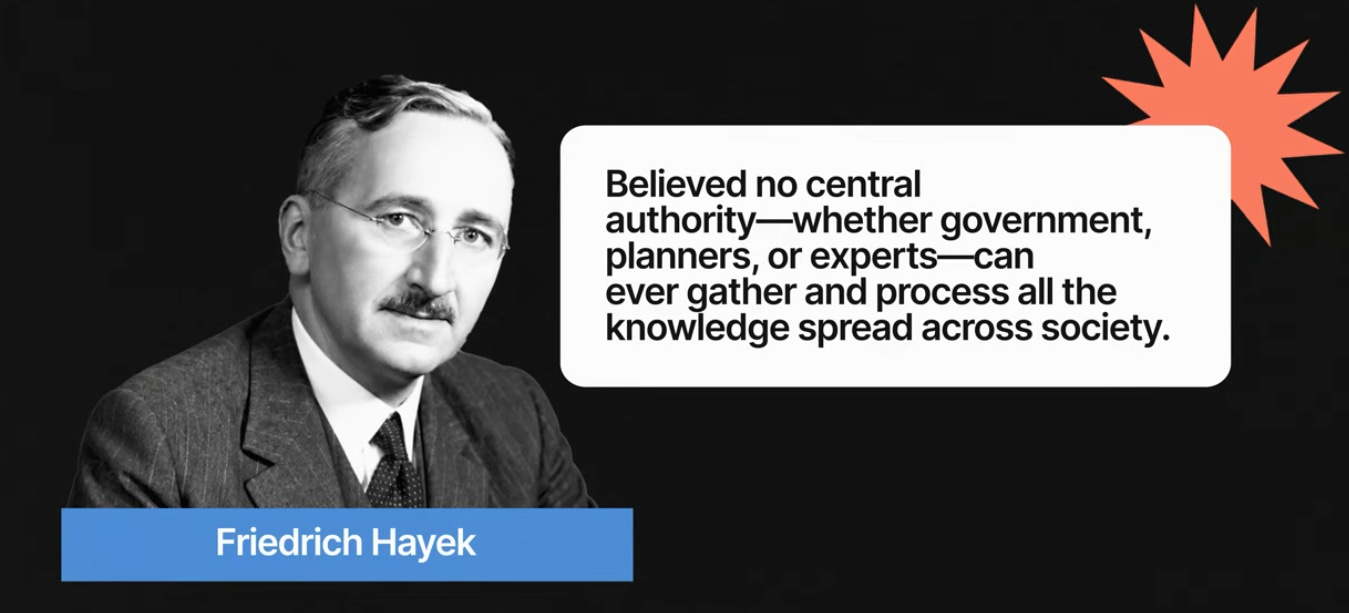

Hayek’s argument was simple and profound: no central authority — no government, no planning committee, no body of experts — can ever collect and process all the information that exists across an economy or a society. Information is scattered across millions of individual minds, in local contexts, in tacit knowledge that simply cannot be written down or transmitted. A farmer in Vidarbha knows something about cotton that no bureaucrat in Delhi can ever know. A trader in Surat knows something about diamond prices that no ministry report can ever capture.

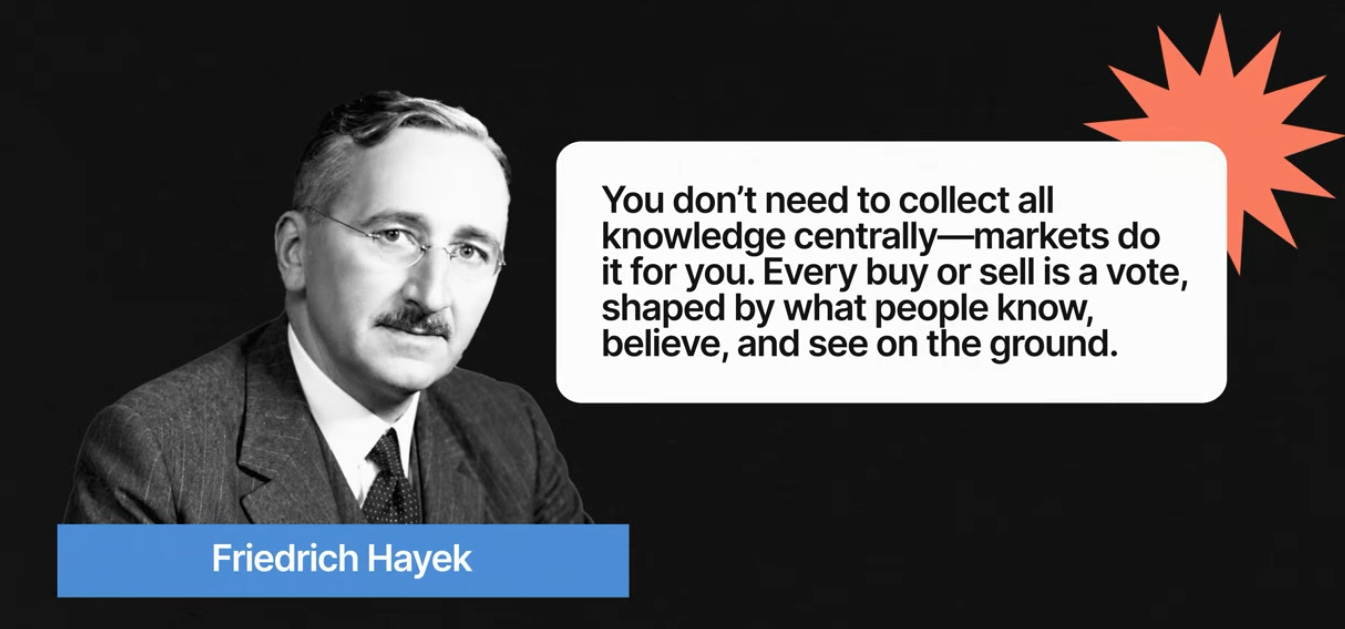

But here’s where the beauty of markets comes in: you don’t need to collect all that information centrally. Markets can do it for you. Every time someone buys or sells, they are essentially voting with their money — based on what they know, what they believe, what they’ve seen on the ground. And the price that emerges from all that trading is a compressed signal of everything everybody knows, collectively. Prices embed information within them — information that is perhaps most honest and most efficient.

This idea is the foundational philosophical backbone of every prediction market ever built.

Kenneth Arrow — State-Contingent Securities (1953)

The next piece came from Kenneth Arrow, the Nobel Prize-winning American economist. Arrow introduced a concept called a state-contingent security — which sounds complex but is actually quite simple. Imagine a contract that pays you one unit of money if it rains in Mumbai on a specific date, and pays you zero if it doesn’t. Its entire value comes from whether a specific future state of the world occurs.

Arrow showed mathematically that with a complete set of such contracts — one for every possible future state of the world — you could, in principle, price any uncertainty. What he was describing, without using the term, was the framework of a modern prediction market contract.

Eugene Fama — Efficient Market Hypothesis (1960s)

The third piece came from Eugene Fama — the Efficient Market Hypothesis. The idea that asset prices already reflect all available public information, and when new information arrives, prices adjust immediately — faster than any analyst or newspaper can. If that’s true for stocks and bonds, there is no reason in principle that it couldn’t be true for political events, policy outcomes, or economic forecasts.

Robin Hanson — Decision Markets and Futarchy

By the 1990s, all of these threads were pulled together by Robin Hanson, an economist at George Mason University. Hanson asked: if markets aggregate information better than experts, why don’t we deliberately engineer markets to answer specific questions? Not just “what will oil prices be?” but “who will win the next US election?” or “will this drug get approved?” or “what will India’s current account deficit be next year?” He called these decision markets.

He went even further — proposing a governance model called futarchy . The idea: vote on values, but bet on beliefs. A nation, through voting, decides the outcomes it wants to achieve — say, 10% GDP. That’s the values part. Then, instead of politicians deciding policy based on ideology and intuition, prediction markets estimate which policy is most likely to achieve that desired outcome, and the nation implements whatever the market prefers. Radical, yes. Possibly impractical. But it got me thinking hard about the deeper value of prediction markets.

Hanson also made a deeply practical contribution: he invented the Logarithmic Market Scoring Rule (LMSR) — a mathematical mechanism that ensures a prediction market always has liquidity. It means a prediction market operator can always offer a price, and traders can always buy or sell, even when there aren’t enough natural buyers and sellers on both sides. It became the engine inside most of the prediction market platforms that exist today — Polymarket, Kalshi, and others.

A Brief History

The early days. Organised presidential election betting markets operated on the New York Curb Exchange from the 1880s through the 1930s — and were quite accurate, correctly calling 11 out of 15 presidential elections. Three things killed them: scientific polling arrived (George Gallup correctly predicted Roosevelt’s 1936 landslide when almost everyone else got it wrong), anti-gambling sentiment grew politically powerful across the US, and New York legalised horse-race betting in 1939, giving gamblers a cleaner, legal alternative.

The Iowa Electronic Markets. In 1988, three economists at the University of Iowa — Robert Forsythe, George Neumann, and Forrest Nelson — were sitting at a bar in Iowa City, frustrated by how badly polls had performed in the Democratic primaries that year. They decided to build a real-money market on the outcome of the presidential election. With modest funding and just 192 initial traders drawn from the university community, they launched the Iowa Political Stock Market — contracts that paid $1 if Bush won, $0 if he lost, and vice versa. The result? The market predicted George H.W. Bush’s popular vote share to within 0.2 percentage points, outperforming virtually every major poll.

In 1992, the CFTC issued it a formal no-action letter: “We see what you’re doing, we’re not going to shut you down — but keep it small and keep it academic.” Investments were capped at $500 per person.

The decade of experimentation (1999–2013). Intrade launched in 1999 out of Dublin — deliberately outside US jurisdiction — and became the most famous prediction market in the world, correctly predicting Saddam Hussein’s capture, Obama’s 2008 victory, and 49 of 50 states in 2012. In 2003, the Pentagon’s research arm, DARPA, funded a project to use prediction markets to forecast geopolitical instability in the Middle East. When two senators went public, calling it a “terrorism futures market,” the project was cancelled within 48 hours. The CFTC eventually sued Intrade in 2012, and in March 2013, the platform collapsed entirely — not really from regulation, but from a financial scandal involving diverted client funds.

From 2018 onwards — going mainstream. Two MIT graduates, Tarek Mansour and Luana Lopez Lara, both with backgrounds in quantitative finance, took a different approach: seeking to get regulated first. After three years of back and forth with the CFTC, they obtained approval for what is known today as Kalshi — the first fully licensed event contract exchange in the United States, which publicly launched in 2021.

Today, Kalshi is valued at $22 billion, both founders are billionaires, and Luana is the world’s youngest self-made woman billionaire.

Around the same time, Shayne Coplan, a 20-year-old New Yorker, founded Polymarket — built on the Polygon blockchain and denominated in USDC stablecoin. After regulatory back and forth with the CFTC, Polymarket acquired QCX (a CFTC-licensed entity) and obtained the regulatory standing to operate legally in the US.

Today, Polymarket is valued at close to $9 billion.

The 2024 elections as a turning point. Two regulatory battles played out. One — won by Kalshi against the CFTC — made election contracts on licensed, regulated exchanges legal in the US for the first time in a century. The second, around sports contracts, involves a constitutional confrontation between federal and state jurisdiction that is still ongoing, with a restraining order currently in place.

What Does This Mean for India?

Quite a bit, actually.

If you look up any of these prediction markets today, you will find India-specific events actively listed and traded — state assembly elections, economic data outcomes, even sporting events — all being priced in real time on platforms based thousands of miles away.

Sports betting is not legal in India. As Indian citizens, we cannot participate on these platforms either. But information doesn’t respect borders. It never has.

Think about who is on the other side of these trades. Foreign institutional investors who have billions of dollars parked in Indian equities and bonds. Global macro funds deciding whether to go risk-on or risk-off on India this quarter. For them, prediction market prices on Indian events are live signals — real-time intelligence on political continuity, policy direction, and economic momentum. The kind of ground-level information that no Bloomberg terminal can give you.

Will India ever have its own prediction markets? The honest answer is: not anytime soon. Our existing derivatives markets are still maturing. The regulatory frameworks around them are still evolving. Prediction markets would need a far more sophisticated ecosystem — in terms of market infrastructure, regulatory clarity, and investor sophistication.

But here is the encouraging part. The fact that the American regulatory system is now formally recognising prediction markets — that a body like the CFTC is actively debating, litigating, and ultimately legitimising them — is a signal that this is no longer a fringe idea. It is becoming mainstream financial infrastructure. And if history is any guide, ideas that get legitimised in the US have a way of eventually finding their footing in the rest of the world. India included. We may not be there yet. But someday, yes.

A Word of Caution

The logic of prediction markets — the wisdom of crowds — works when participants are diverse, independent, and dispersed. But when a small number of large, ideologically aligned traders dominate the market, you end up amplifying a concentrated view that could be far from reality. This is a real limitation. It does not invalidate the idea. But we should not take prediction market prices as gospel either.

Recommended Reading

Two books that shaped the thinking in this edition:

- The Wisdom of Crowds by James Surowiecki — a very readable introduction to the core idea.

- Superforecasting: The Art and Science of Prediction by Philip Tetlock and Dan Gardner — their findings about what separates accurate forecasters from everyone else, directly relevant to understanding what prediction markets are trying to replicate at scale.

Do share your thoughts in the comments — they all get read, and responses will follow.

Thank you — and as always, be careful with your capital.