Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Birla buys a renewable firm from Shell for $1.8 billion

- What does iron ore really cost?

The Chatter by Zerodha

Our team at Markets spends a lot of time reading earnings call transcripts and listening to management interviews. Along the way, we come across plenty of interesting insights that are worth sharing.

That’s what The Chatter is for.

It’s a weekly newsletter where we dig through what India’s biggest companies are saying and bring you the most interesting insights into businesses, industries, and the wider economy.

Aditya Birla buys Sprng Energy from Shell for $1.8 billion

Aditya Birla Renewables, a subsidiary of Grasim Industries, made headlines recently for acquiring a renewable company from Shell for ₹17,200 crore ($1.8 billion).

Obviously, this sounds like a really big deal. But before touching that number, if you are wondering when Birla entered the renewables space, we did too. Turns out, they have been in this sector for quite some time, having silently built up a portfolio of roughly 4.4 gigawatts of capacity.

However, perhaps one reason their renewables division hasn’t made all that noise is because, up until now, they essentially acted as an internal utility provider. They set up wind and solar farms almost entirely to run their own sister companies. Their UltraTech Cement plants and Hindalco aluminium smelters are power guzzlers, so it probably only made sense to build captive power capacity for them.

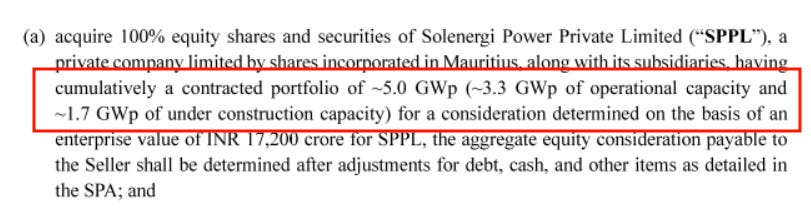

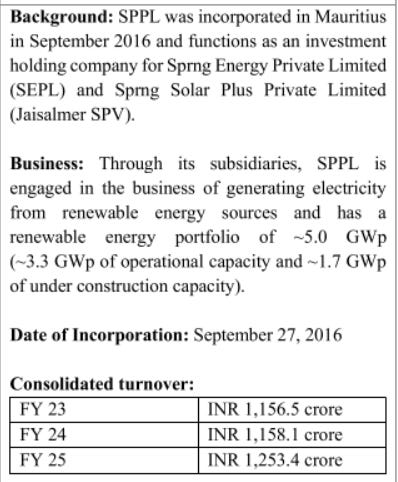

On the other side of the equation, Shell has been trying to get rid of Sprng Energy for a while now. Technically, what Birla is buying is Solenergi Power, a Mauritius-registered holding company that owns the Sprng Energy group of companies. But what matters is what sits inside it: a portfolio of 5 gigawatts. About 3.3 gigawatts of that is already operational and generating power, while another 1.7 gigawatts is under construction.

When you add Sprng’s 5 gigawatts to Birla’s existing 4.4, you get a combined portfolio of around 9.3 gigawatts. The deal flips Aditya Birla Renewables from a business that mostly built solar and wind farms to power the group’s own factories, into one of India’s larger commercial power producers, selling bulk electricity to the state grid under long-term contracts.

And they aren’t stopping there. The group had set itself a 10 gigawatt target, which this single deal nearly completes ahead of schedule.

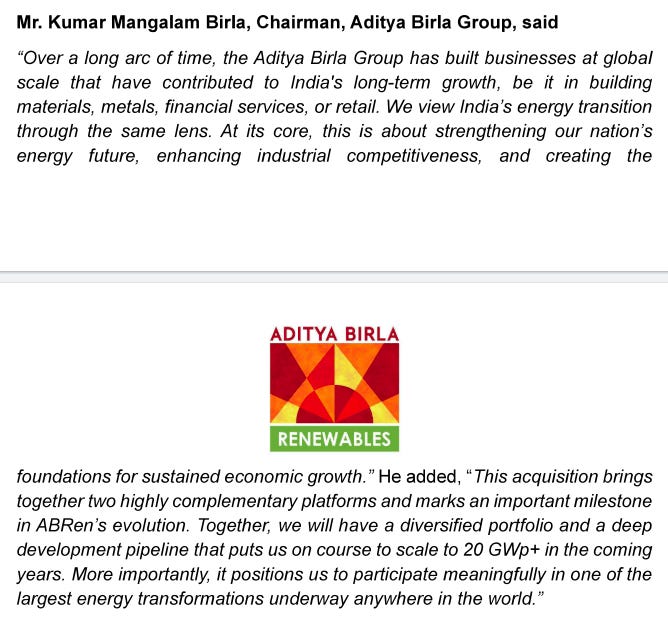

Chairman Kumar Mangalam Birla laid out where they go next:

“Together, we will have a diversified portfolio and a deep development pipeline that puts us on course to scale to 20 GWp+ in the coming years. More importantly, it positions us to participate meaningfully in one of the largest energy transformations underway anywhere in the world.”

Crude reality

Now, we come to that $1.8 billion headline figure.

What’s funny is that, just 4 years ago, Shell bought Sprng for roughly $1.55 billion (₹12,000 crore ). Back then, it only had 2.1 gigawatts up and running. Over the next four years, Shell burned capital to build that up to 3.3 gigawatts. When you add the construction bill to the original purchase price, Shell’s total spend likely comes close to the $1.8 billion it’s getting today, and may even cross it.

Essentially, after four years of holding this business, Shell is walking away roughly flat, maybe worse. But, probably to them, selling the business at that price seems like a better option than holding it any longer.

The party that actually made money here was Actis, a private equity firm that built Sprng from scratch starting 2017. They acquired the land, fought the red tape, won the contracts, and then sold the finished business to Shell.

So why would Shell sell when everyone is getting in on this space? Because Shell in 2026 is a very different company from Shell in 2022. To understand what changed, you have to remember what 2020-2022 felt like for oil companies.

For one, the pandemic had crushed oil demand so badly that US crude prices briefly went negative. There was lots of doubt on how quickly these prices would recover. In general, over the past decade, there were signs that oil prices would continue to remain low because the world structurally faced a glut of oil. This, as we’ve covered before, reduced the pricing power that OPEC countries had over oil, and likely even depressed the profits of conventional oil firms like Shell.

But secondly, and more existentially, trillions of dollars were flowing into ESG funds, and money managers wanted their oil stocks to show a plan for a post-oil world. The pressure wasn’t just from markets either. In May 2021, a Dutch court ordered Shell to cut its emissions 45% by 2030, and in the same month, a tiny activist fund called “Engine No. 1 ” managed to win three board seats at ExxonMobil on a climate platform.

The message to every oil major was clear: show us your green future or we’ll force one on you.

So they all moved at once. BP promised to cut oil production. Total went as far as renaming itself TotalEnergies. And it was at the peak of this ESG wave that Shell bought the business from Actis because it was the fastest possible way to look green.

Then, the world flipped again, as Russia invaded Ukraine in 2022. Oil and gas prices soared, and the American majors that had ignored the green pressure and stayed loyal to fossil fuels posted record profits while their shareholders got rich. The European majors that had pivoted away watched their stocks lag.

Under its current CEO, Shell’s priority has flipped entirely to shareholder payouts. It has promised to return 40 to 50% of its operating cash flow to investors, even as its net debt jumped from $45.7 billion (₹4.3 lakh crore) to $52.6 billion (₹5 lakh crore) in the first quarter of this year.

Shell began to exit green projects everywhere, from a $1 billion (₹8,800 crore) write-off on a US offshore wind project, to pulling out of home electricity retail in the UK and Germany. Sprng was roughly four-fifths of everything Shell owned in renewable power generation. When a company needs cash that badly, a flat exit is a good exit.

How Sprng makes money

To understand both sides of this trade, you have to understand how a company like Sprng earns its revenue.

When Sprng builds a solar farm, it signs a power purchase agreement, or PPA, typically for 25 years. Under this contract, the buyer agrees to purchase every unit the farm produces at a fixed price for the entire period. The buyer is usually a state electricity distribution company (or DISCOM), which are often broke, partly because of its PPAs with India’s legacy coal plants. A central agency like NTPC or SECI often sits in the middle because banks won’t lend against the promises of DISCOMs. We’ve covered them extensively in the past.

Then, the central agency buys the power from the farm, sells it onward to the states, and its credit rating is what makes the project financeable in the first place.

In a way, this is what a fixed-price annuity looks like. The tariffs are locked, with some of Sprng’s older contracts at rates as low as ₹2.17 a unit, so revenue only grows when a new plant comes online. This structure explains everything about Sprng’s numbers: as per the deal filing, the company made around ₹1100-1200 crore in the last 3 years.

Birla is paying an enterprise value of nearly fourteen times revenue, which sounds absurd until you remember that what it’s really buying is 25 straight years of contractually-guaranteed cash flows .

And by the market’s own yardstick, the price seems somewhat reasonable. Over the last eighteen months, a joint venture of ONGC and NTPC bought Ayana Renewable Power’s 4.1 gigawatt platform for ₹19,500 crore, and JSW Energy bought O2 Power’s 4.7 gigawatts for about ₹12,500 crore.

What Birla actually bought

So Birla has the money and the ambition. But why buy an existing company instead of building from scratch?

Well, building a new solar or wind farm, what the industry calls a greenfield project, is no easy feat in India. You have to buy massive tracts of land, settle local disputes, get environmental clearances, and import thousands of panels. That whole process can take more than a couple of years.

But the worst bottleneck isn’t the land or the panels, but the grid, which is something we’ve covered in a previous story.

India is installing solar panels far faster than it is laying the high-voltage lines needed to carry the electricity. The grid is severely choked. It has gotten so bad that state grid operators routinely call solar farms in the middle of the day and order them to shut off, because the wires simply cannot handle the surge. The industry calls this curtailment , and for the company it means power that was generated but can never be billed.

Adani Green, the biggest player in the space, told its investors it lost an estimated ₹500 crore in a single year because it was forced to throw electricity away.

The grid is also administratively blocked.

Under rules from 2022, developers could reserve a spot on the national power lines simply by showing a letter saying they had won a government bid, even if they didn’t have the money or the final contracts to actually build. But by mid-2026, the government realised that up to 22 gigawatts of grid capacity was blocked by these stalled ghost projects, while companies that were ready to build couldn’t get permission to plug in.

So on July 11, the electricity regulator CERC stepped in with an ultimatum: developers holding stalled reservations have 60 days to either prove they are building, or surrender their grid access. Do nothing, and heavy penalties kick in. Whatever gets surrendered will be auctioned off to companies that can actually build.

Sprng’s plants are already legally connected to the grid, which means Birla skips most of this grind.

Conclusion

India crossed 50% non-fossil fuel capacity in June 2025, five years ahead of its own target, and sits at roughly 280 gigawatts of non-fossil capacity as of March 2026, racing toward 500 gigawatts by 2030.

Oil majors tried to get a piece of this renewable build-out in a bid to “go green ”, but that hasn’t panned out for them very well. Indian conglomerates, however, are leading the solar charge: Adani, Tata, JSW, NTPC and ONGC, and now Birla, which is helped along by new RBI rules that, for the first time, let Indian banks fund up to 75% of an acquisition like this one.

Shell looked at single-digit returns and a choked grid and decided its money was better spent elsewhere. Birla looked at the same asset and saw 25 years of guaranteed cash flows, plus a grid connection that money alone cannot buy quickly. Both can be right.

Whether this deal ends up a steady annuity or an expensive queue ticket depends on the one thing neither company controls: distribution.

What does iron ore really cost?

On July 13, the Supreme Court upheld the royalties India demands from iron ore miners. We know, this seems like an unforgivably dry, technical matter — and it would be, except that thousands of crores of rupees hang in the balance.

The matter hinges on a formula . Kirloskar Ferrous Industries, an iron-ore miner and pig-iron producer, challenged the way the Indian government calculates the royalties owed by iron ore producers. Their argument, fundamentally, was that the government’s formula forced companies to pay a charge on top of a charge. Those royalties are computed on a base that already contains a royalty.

The court settled the matter in the government’s favour. The government claimed their way of doing things helped prevent underpayment, and the burden it placed on individual miners was not so onerous that it delegitimised the formula. The Supreme Court concurred, settling the legal question.

Did it come to the correct answer? We aren’t sure.

Then again, this is a space filled with distortions. Consider this: between August 2022 and January 2023, Odisha’s official benchmark for iron-ore lumps with 51–55% iron content fell by roughly half. The wider iron ore market hadn’t moved nearly as much. Individual mines were still quoting prices in broadly the same range they had been before. But the benchmark — the number the government uses to calculate what it is owed — had halved. The government’s revenues took a direct hit.

Mining is an opaque, slippery world. It operates within an unusual permitting regime. It is replete with bad solutions chasing bad problems. This is the story of one such situation.

Not mine, but ours : the royalty problem

In principle, the minerals under India’s land belong to all of us.

The government — our representative, at least in theory — only gives miners the right to extract them. It extracts a cost for this privilege, however; miners must pay the state royalties for whatever they dig out. These royalties are charged ad valorem , that is, according to the ore’s value. For iron ore, those royalties are charged at fifteen percent.

Calculating royalties

Fifteen percent of what , however? How do you calculate the “value” of ore? There’s no one price for it; the price that ore is sold at can vary — by the state, by its grade, by the mine. How do you benchmark it?

For this, the government looks at the ‘Average Sale Price’, or ‘ASP’ — a monthly benchmark published by the Indian Bureau of Mines. This is a weighted average, broken down by grade and state, built on prices and quantities the miners themselves report in monthly returns they file with the government.

There are extra charges atop this royalty. For one, miners pay an extra 10% of the royalty amount as their mandatory contribution to the ‘District Mineral Foundation’, or DMF — a body that looks after communities that live around mines. In addition, they pay an extra 3% of the royalty amount to the National Mineral Exploration Trust, or NMET, which finances the exploration of new mining sites.

And finally, there’s an “auction premium” — a little sweetener miners offer to the state. Since 2015, most new mining leases in India have been auctioned. Bidders compete with each other on the share of the ore’s value they’re willing to give the state.

The amount a miner must pay in these extra fees, like the base royalty, depends on the all-important ‘ASP’ figure the government announces. And that, in turn, depends on the data miners give the government. This set-up is at the heart of the case before the Supreme Court.

Getting to a ‘right’ price

This fee structure exists because the government faces a fundamental problem: it wants a fair value for mineral resources a private entity extracts. Except, it doesn’t actually sell any ore. It has to construct a price for a commodity it doesn’t deal in. To do so, it needs data, and a formula to turn that data into a price.

The easiest solution is to charge a single flat fee per tonne. This would be easy to administer, and hard to game. At the same time, a standard price would struggle to deal with the difference in quality coming out of any mine. A miner that dug out a tonne of low-grade rubble would pay the same amount as someone that drew out a tonne of high-grade ore, even though the market would reward them very differently.

Alternatively, you could plug in a lot of data to construct an index. Coal has something like this: the government tracks a National Coal Index, built atop notified public-sector prices, auction prices and import prices. These inputs are hard to spoof, making this index hard to game.

But you don’t find that quality of data everywhere. India doesn’t have a clean domestic index for iron ore prices, for instance. It’s hard to know what price any one grade would attract. The best available benchmark is the price of cargo delivered to China, and that might bear little connection to the price or quality of ore Indian miners actually have.

This is why India collects miners’ self-declared transaction prices to get to a royalty figure.

Pliable benchmarks

The government takes in data given by the mines in an area, and then averages the price out. These averages are weighed by quantity . Consider a market with two consignments of supply — one with a hundred thousand tonnes, and the other with just a hundred. The average price will take the quantity of each consignment into account, along with the price they attracted.

These average prices aren’t drawn from the whole Indian iron ore market. They’re calculated separately, for each grade, in each state, every month. There are often just a handful of mines feeding into any one number. Miners, as a result, are benchmarked to a narrow slice of the market.

Perversely, if you’re one of the big miners in your area, this lets you move your own benchmark. The royalty, the DMF, the NMET, the auction premium you’re expected to pay — everything is tied to just that month’s benchmark. With some planning, you can change this amount meaningfully.

This is especially true of captive mines: for instance, when a steel-maker owns their own iron ore mines. You can simply declare your dispatches at times when the ASP has fallen, and pay lower royalty.

That is what the Indian Bureau of Mines found in Odisha. Mines that had reported the highest ex-mine prices in their band in one month would make no despatches, or very few, in the months that followed. As long as their prices turned out to be above the average, it made sense to hold back on declaring sales, so that they didn’t hike the ASP. This is why the ASP could halve in a short period, despite the outside market looking the same.

In fact, the larger the premium you’ve agreed to part with in the mining auction, the greater is your incentive to play this game.

A charge on a charge

Now, we come to the rule Kirloskar challenged — one that had been part of the framework since 2016.

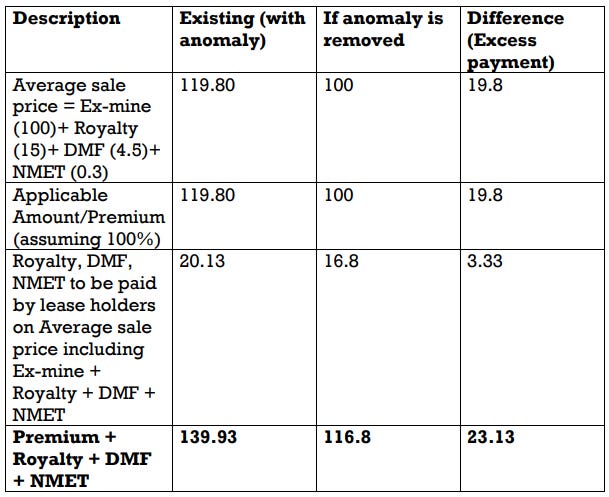

When the government was calculating the “sale value” feeding into the ASP, it did not deduct royalty, DMF or NMET. Effectively, the fifteen percent was calculated against a number that already contains the levies.

Imagine a mine has sold ore worth ₹100. If you were to plainly add royalties and other fees to that amount, a simple calculation would tell you that the miner would owe the government roughly ₹17. But the government doesn’t take those ₹100 as the base. It takes a higher figure — one that already includes all these fees. It is a royalty, charged on a rate that already includes the very same royalty! That, in itself, adds a few percent to what the government is owed.

This effect is magnified even further when you add auction premiums to the equation — when the difference could be as high as a quarter of the actual value of the ore they’re sitting on.

The government, meanwhile, defends this as protection against the revenue it loses because of how miners manipulate the ASP.

On the surface, these differences might sound small. But they are calculated on a massive base. India’s iron ore output in the year ending March 2024 was worth roughly ₹1 lakh crore. According to the government, if this rule is removed, states’ revenues from mining could fall by about ₹6,200 crore every single year . Over the lifetime of these mining leases, this is cumulatively a question of lakhs of crores.

What the court did

In its judgement, the Supreme Court upheld the formula the government used.

At its heart, this is a fair call to make. Courts are poorly placed to design royalty formulas. For a court to invalidate economic regulation, the bar it must cross is deliberately kept high. A fee might look weird as policy, but that doesn’t make it unconstitutional .

Moreover, entities that had bid for mines already knew this formula. More than 585 mineral blocks have been auctioned since 2015. Every winning bid was made under this definition of ASP. They should have calibrated the premium they were willing to pay according to this formula. One way or another, ten years of auctions have embedded the rule in the price of these leases. Changing the formula now would improve the winner’s economics after the contest was over — which would be unfair to those who made losing bids.

Somewhat problematically, however, the court didn’t stop at saying that. Instead, it justified the government’s claims, endorsing the notion that iron ore miners were evading their dues, and this was a measure meant to counter evasion.

In doing so, it didn’t attempt to match the measure to the problem it was trying to solve. Protecting one’s revenue, after all, is different from preventing evasion. The government’s concern was that miners could report artificially low values and reduce what they owed. That, however, was a matter of how the weights in the ASP were determined. The question of whether royalties should be charged on top of royalties barely had any bearing on this. A miner can still vary their reported despatch according to the prevailing ASP — the formula does little to address that.

The anomaly gets a second life

In 2022, the government’s own expert committee — chaired by a retired IAS officer, with members from NITI Aayog, the ISI, the Steel Ministry and the Bureau of Mines — concluded that the formula does charge royalty on top of royalty. It called this an anomaly, and proposed a fix: exclude royalty, DMF and NMET when determining the ASP.

Then, the government reversed course, deciding not to amend its rules after all. Its stated reason was that doing so would seriously impact the revenue of the states. States such as Odisha and Jharkhand, after all, rely heavily on mineral revenue.

The court, however, went further than that — instead of accepting that this is the way things are run, it endorsed the rule. Where the government’s own committee saw an anomaly, the court saw a defence against evasion. Instead of weird hold-over from an old rulebook, in this framing, a royalty atop a royalty became a stated tool of government policy.

Tidbits

- Hero MotoCorp approved a fresh cash investment of up to ₹1,000 crore (about $104 million) into the electric scooter company Ather Energy. Hero is already the biggest shareholder in Ather and is making this move to boost its position in the fast-growing electric vehicle market.

Source: Reuters

- The cost of items sold in bulk (wholesale) in India jumped by a record 9.9% in June, mostly because food and fuel prices went up. This puts a lot of pressure on companies making goods, which could eventually make everyday items more expensive for regular shoppers.

Source: ET

- US politicians changed a proposed law to lower threatened taxes on countries buying Russian oil, like India and China. Instead of a massive 500% tax, the highest tax is now capped at 100%. This helps avoid breaking trade ties with India and China while still putting some pressure on Russia.

Source: NDTV

- The long-awaited trade agreement between India and the United Kingdom officially starts on July 15. The deal will remove or lower taxes on many goods traded between the two countries. This is expected to create new jobs and make it much easier for businesses to grow in both places.

Source: Deccan Herald

- IKEA plans to invest over ₹21,000 crore in India by 2030, which is double what they originally planned. They want to open around 30 stores, sell more items made locally in India, and grow their online shopping business.

Source: BS

- This edition of the newsletter was written by Krishna and Pranav.

Points & Figures by Zerodha

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s retail lending landscape has transformed, using credit bureau data to reveal why lenders are moving away from unsecured loans and betting increasingly on collateral-backed credit.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops so that you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()