Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

Today on The Daily Brief:

- Paytm’s Rollercoaster Quarter

- Can Rural India Rely on Farming as Expenses Keep Rising?

- The markets, according to Stanley Druckenmiller

Paytm’s rollercoaster quarter

In our first story today, let’s talk about Paytm. This quarter has been a big one for Paytm, mainly because of issues with their banking unit, Paytm Payments Bank Limited (PPBL).

In case you missed it, a few months ago, the Reserve Bank of India (RBI) took strict action against PPBL, stopping it from adding any new customers. This was a major blow because onboarding new users is one of the main ways Paytm attracts new customers who then use other services like UPI payments or loans.

The RBI’s crackdown came after PPBL reportedly had lapses in two key areas: security protocols and KYC (Know Your Customer) processes.

This setback slowed down Paytm’s growth and gave its competitors, like PhonePe and Google Pay, a chance to gain a larger share of the UPI market.

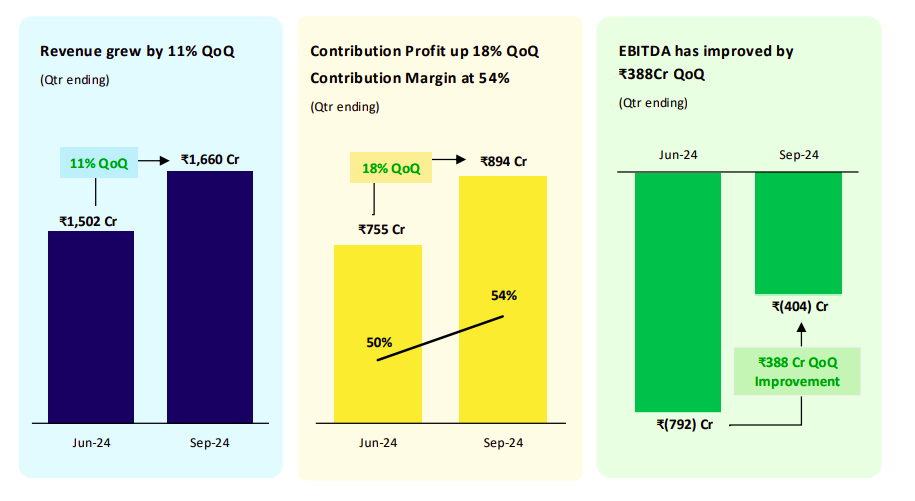

But despite these challenges, Paytm managed to turn a profit of ₹930 crore this quarter. If you’re wondering how, it’s mostly due to a one-time event: the sale of their ticket-booking business, Paytm Insider, to Zomato for ₹1,345 crore.

Source: Paytm

Paytm decided to sell Insider because it wasn’t central to its main business. By selling it, they could focus more on their core services, like payments and lending. The sale also boosted Paytm’s cash reserves, which now stand at a strong ₹9,999 crore. It allowed them to bring in cash and sharpen their focus on the areas that drive growth.

Even without the proceeds from the sale, Paytm’s performance has improved. Their EBITDA loss dropped significantly, from ₹792 crore in the previous quarter to ₹404 crore this quarter.

Looking ahead, Paytm is putting a lot of effort into growing its lending business. To support this, they’ve introduced a Default Loss Guarantee (DLG) model.

So, what does this mean? In simple terms, when Paytm connects lenders like banks with borrowers, it promises to take on some of the risks. If a borrower doesn’t repay the loan, Paytm agrees to cover part of the loss.

This setup encourages banks to lend more through Paytm’s platform, knowing that Paytm will share some of the risks if things go wrong. And so far, this approach seems to be working. In the second quarter of FY25, Paytm disbursed ₹3,300 crore worth of loans to merchants, up from ₹2,500 crore in the previous quarter. What’s interesting is that 50% of these loans went to repeat borrowers, suggesting that both lenders and borrowers trust the system.

However, there’s a downside to this model. If too many borrowers fail to repay their loans, Paytm will have to absorb those losses, which could hurt future profits.

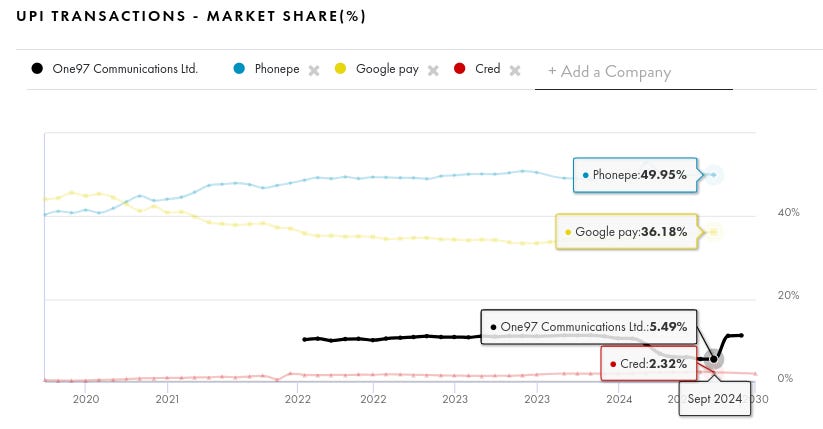

While Paytm’s lending business is gaining momentum, its UPI services have faced a bit of a setback. Paytm saw its Monthly Transacting Users (MTUs) drop from 7.8 crore to about 7 crore this quarter.

Source: Tijori Finance

This dip is linked to the RBI’s restrictions on Paytm Payments Bank, which, as we mentioned earlier, also impacted related services like UPI. Once these regulatory hurdles are cleared, Paytm is expected to push hard to regain its lost market share. But for now, the UPI segment remains a challenge.

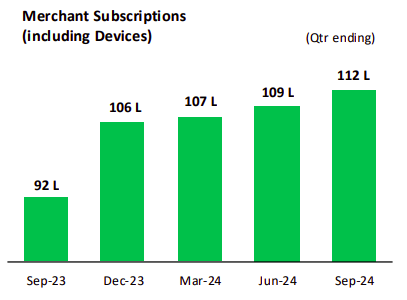

On the bright side, Paytm continues to do well with merchants. Over 1.12 crore merchants now use Paytm’s services, and the company has found creative ways to make money from this base.

Source: Paytm

One of their most interesting innovations is the Soundbox device. If you’ve ever been to a store that uses Paytm, you’ve probably heard the device that announces payment confirmations out loud. Recently, Paytm has started using these devices to play ads for brands like Coca-Cola, Meesho, and Dabur. This turns a simple payment notification tool into a new way for Paytm to earn extra revenue through advertising. Whether or not people will welcome this change remains to be seen.

Overall, while Paytm faces challenges, it’s also finding ways to adapt and grow, even in tough times.

Can rural India rely on farming as expenses keep rising?

In this story, let’s focus on rural India. This topic is crucial because, even though we often talk about India’s rapid urbanization, the heart of the country still beats in its villages. Mahatma Gandhi once said, “The soul of India lives in its villages,” and that statement holds true even today. Around 65% of India’s population still lives in rural areas, making it a vital part of our economy, with agriculture playing a key role in these regions.

To truly understand the rural economy, we need to look closely at how these communities earn, spend, and manage their money. That’s where the NABARD All India Rural Financial Inclusion Survey (NAFIS) comes in. It offers a detailed look into the financial lives of rural households, helping us see how things are changing.

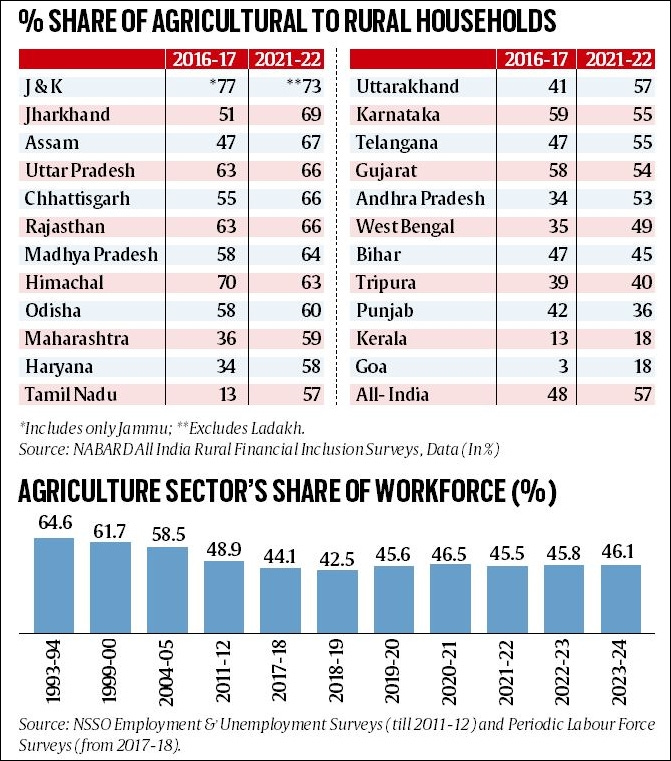

One surprising trend is the increase in people returning to farming. For many years, we saw a steady decline in farming as rural folks moved to cities for better opportunities. But between 2017 and 2022, the percentage of rural households involved in agriculture jumped from 48% to 57%. Much of this shift can be traced back to the COVID-19 pandemic.

Source: IndianExpress

During the pandemic, many migrant workers lost their jobs and had no choice but to return to their villages. With limited options, many families turned to farming again—even if it wasn’t their main source of income before. This “reverse migration” pushed households back to agriculture, not by choice, but out of necessity.

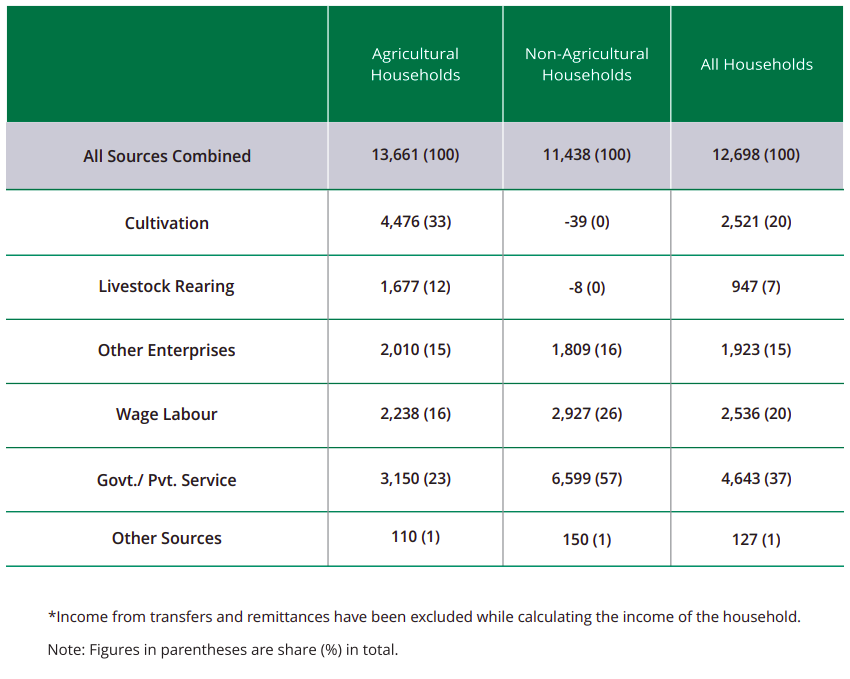

However, even though more rural households are engaged in farming, it isn’t their primary source of income. In fact, more than half of agricultural households now earn most of their money from non-farming activities. Jobs like wage labor or roles in the private and public sectors have become crucial for rural earnings.

Looking at all rural households—both those involved in farming and those that aren’t—only about 27% of their total income comes from agriculture. In comparison, 37% of rural income now comes from non-farming jobs, especially government and private sector employment.

Source: NABARD

So, while farming is still a big part of rural life, the reality is that the rural economy is changing fast, with people increasingly relying on other ways to earn a living.

Why is this shift happening? One major reason is the shrinking size of landholdings. In 2017, the average rural landholding was 1.08 hectares, but by 2022, it had dropped to just 0.74 hectares. As land gets divided and fragmented, it’s becoming harder for families to earn enough from farming alone. Farming is less productive and more expensive, pushing households to seek additional sources of income.

But despite these challenges, there’s some good news. Rural incomes have been rising. Between 2017 and 2022, the average household income in rural areas grew at a rate of 9.5% per year. To put this in perspective, India’s overall GDP growth during the same time was around 9%. So, rural incomes have grown at a slightly faster pace than the national average.

However, like any story about income growth, there’s a catch. Household expenses in rural areas have gone up even more. Between 2017 and 2022, average monthly spending shot up by 69%, outpacing income growth. A notable shift is that more of this spending is now directed toward non-food items. In 2017, households spent 51% of their income on food, but by 2022, this dropped to 47%, showing a move towards spending on other needs or lifestyle improvements.

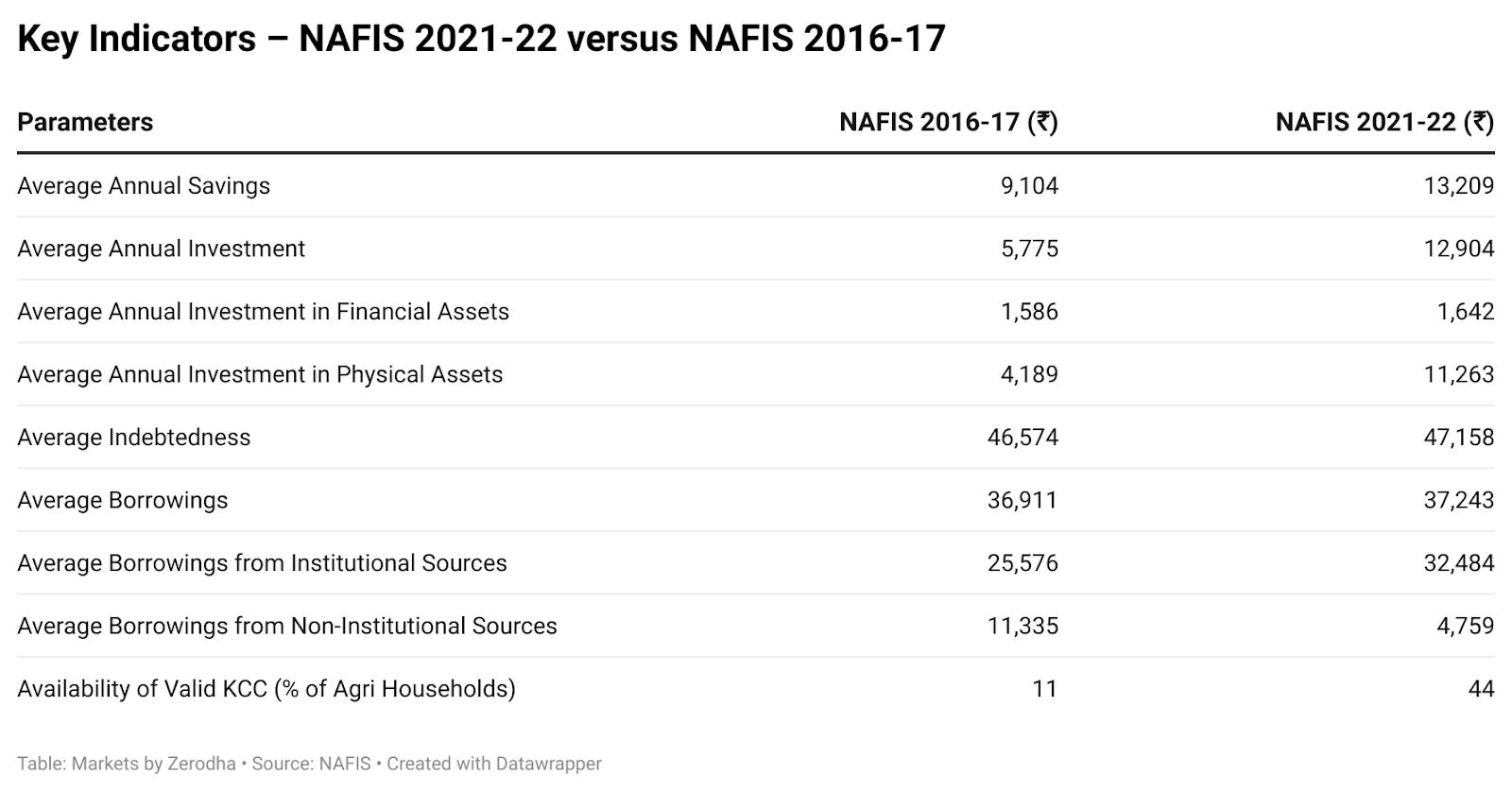

You might wonder—with rising expenses, what’s happening to savings? Surprisingly, savings have increased. In 2022, 66% of rural households reported saving money, compared to just 51% in 2017. And not only are more households saving, but they’re saving more too. Average financial savings per household rose from ₹9,104 in 2016-17 to ₹13,209 in 2021-22.

Source: NABARD

So, how are people managing to save more while also spending more? This shift largely comes down to changes in how people handle their money, much of it influenced by the pandemic. The uncertainty caused by COVID-19 made people more careful about their finances, leading to an increase in precautionary savings. But at the same time, with expenses rising faster than income, many households have had to rely on borrowing to bridge the gap.

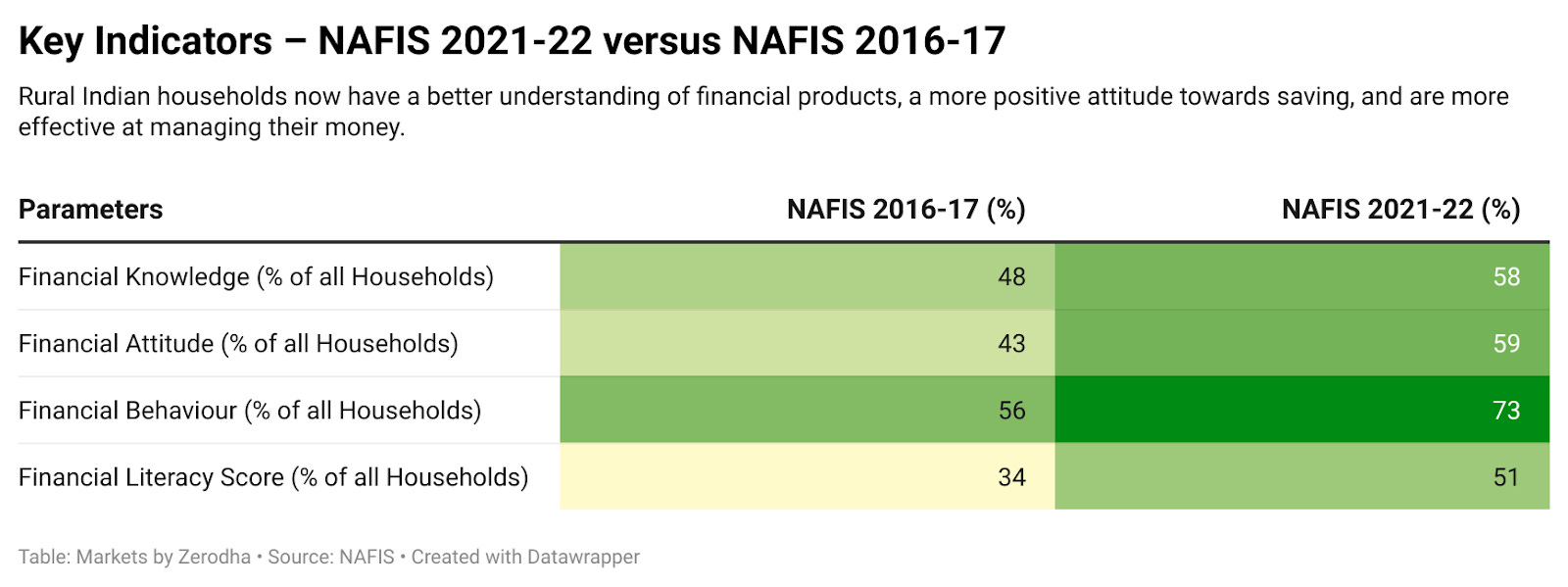

Access to credit has improved significantly in recent years, thanks in large part to schemes like the Kisan Credit Card (KCC) and other loans from banks. The survey found that the average borrowing per household increased slightly, from ₹36,911 in 2017 to ₹37,243 in 2022. What’s interesting is where this borrowing is coming from. There’s been a clear shift towards formal sources, with loans from banks and other institutions rising, while borrowing from informal sources—like moneylenders—has dropped significantly. This suggests that rural households are becoming more financially aware and are starting to use formal financial services more confidently.

In summary, rural India’s financial landscape is changing in ways that aren’t always obvious. More households are turning to farming, but they’re also heavily dependent on non-farming jobs for their main income. Rising expenses are being managed through a mix of borrowing and better financial planning, allowing many households to save more despite higher living costs. Improved financial literacy and better access to formal loans are helping households adapt to these changes, but whether this balance can hold in the long run is still uncertain.

The markets, according to Stanley Druckenmiller

Let’s talk about a recent interview that investor Stanley Druckenmiller gave, which has been creating quite a buzz in financial circles.

For some context—Druckenmiller isn’t just any investor. He’s been incredibly successful for over 30 years without a single losing year. Because of his track record, whenever he shares his thoughts, people pay attention.

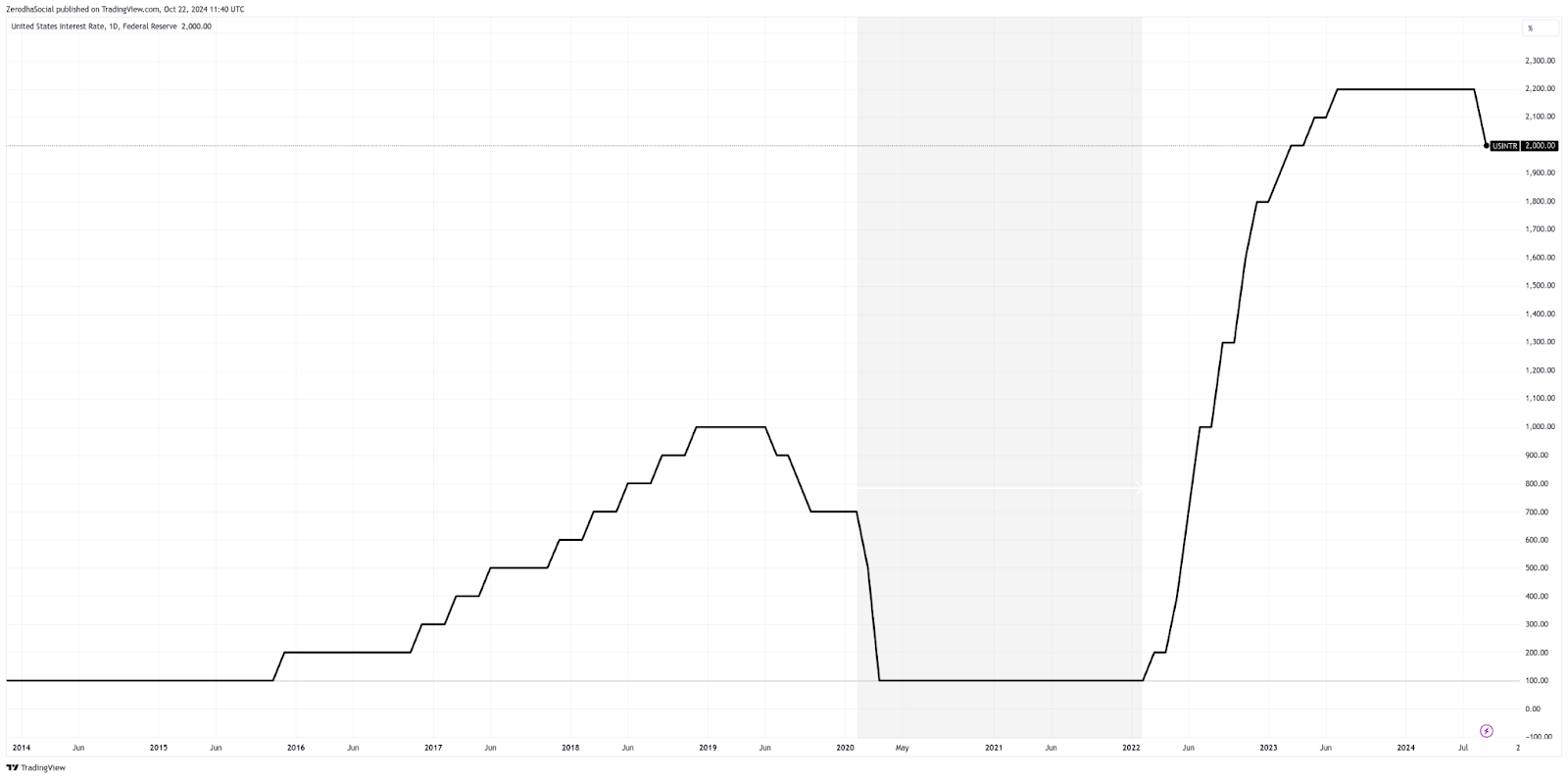

Now, back to the interview. In his latest conversation, Druckenmiller expressed serious concerns about how the Federal Reserve is handling the U.S. economy. To understand his perspective, we need to look at what the Fed has been doing over the past few years.

When COVID-19 hit in 2020, the U.S. economy faced severe challenges. Businesses shut down, people lost jobs, and things looked grim. The Federal Reserve (often called “the Fed”) stepped in quickly by cutting interest rates and injecting trillions of dollars into the economy to keep things afloat.

Druckenmiller supported these actions at the time, believing the Fed did a good job of helping businesses and families through the crisis.

But here’s where it gets tricky. Druckenmiller thinks that by 2021, the Fed should have started to ease off on those measures. The economy was recovering, yet the Fed kept interest rates low for too long. Now, he believes they’ve put themselves in a tough spot.

One of the key points Druckenmiller discusses is “forward guidance.” This is when the Fed gives hints to the public and markets about what it plans to do with interest rates in the future. Businesses and investors rely on these signals to plan their next moves.

In the interview, Druckenmiller argues that the Fed has become too reliant on forward guidance. Instead of making decisions based on what’s actually happening in the economy, they stick to their past promises, even when those promises no longer make sense.

Fast forward to today, and Druckenmiller is still worried, but for different reasons.

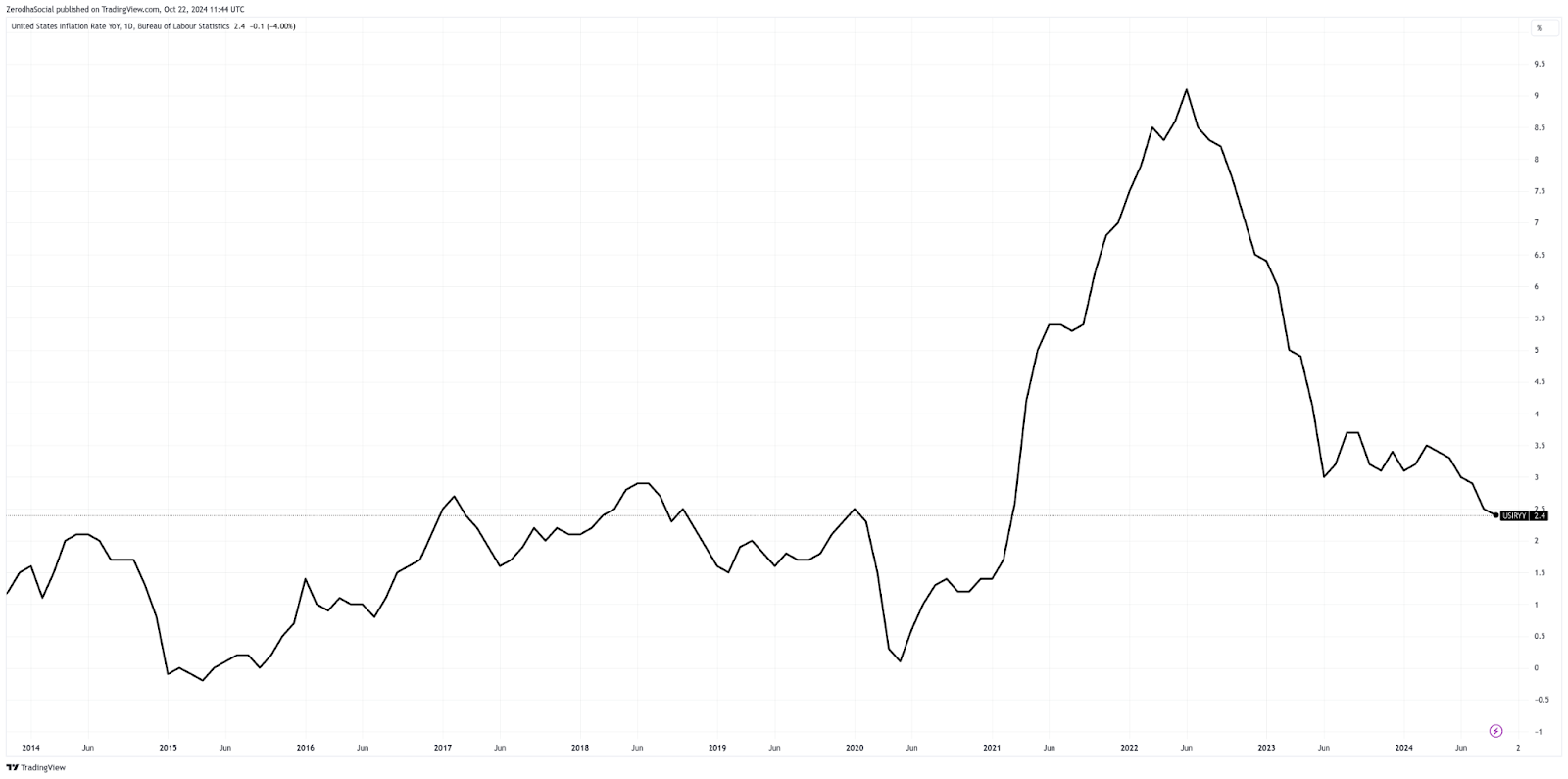

Inflation is higher than the Fed would like, hovering between 2.5% and 3.25%. The Fed has been raising interest rates, trying to slow down the economy by making borrowing more expensive. The idea is that if borrowing costs more, people and businesses will spend less, which should help bring inflation down.

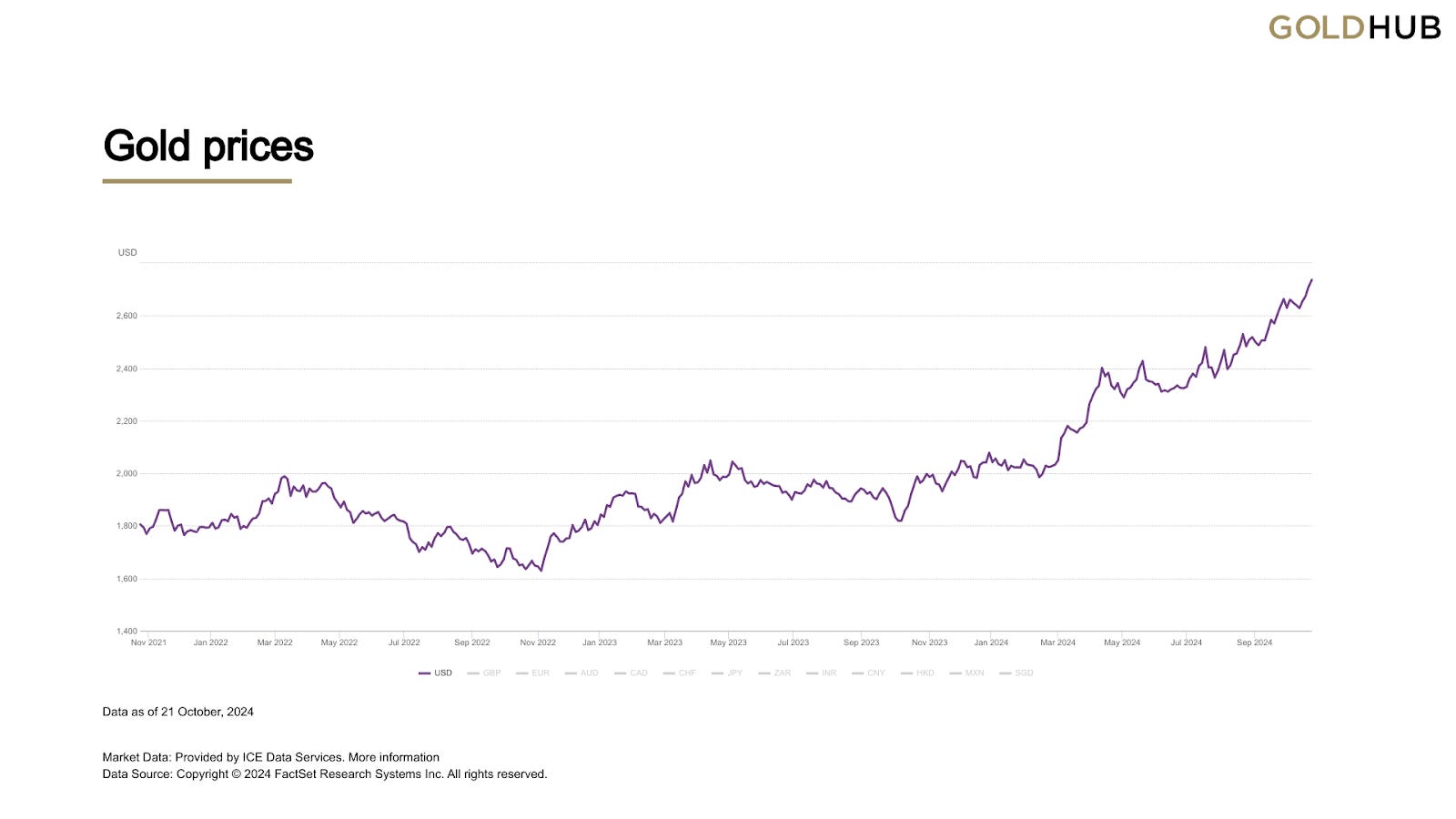

But Druckenmiller thinks this isn’t working. He points out that the economy is still going strong—stocks are climbing, gold prices are hitting record highs, GDP growth is above average, and even cryptocurrencies are performing well.

Source: Blackrock

Source: Gold.org

All of this suggests that the economy hasn’t cooled down, despite the Fed’s rate hikes.

Meanwhile, the Fed has already cut interest rates by 0.5% and hinted that more cuts might be on the way. Druckenmiller believes this is a mistake. He thinks that by signaling these cuts, the Fed might be acting too quickly and heading in the wrong direction.

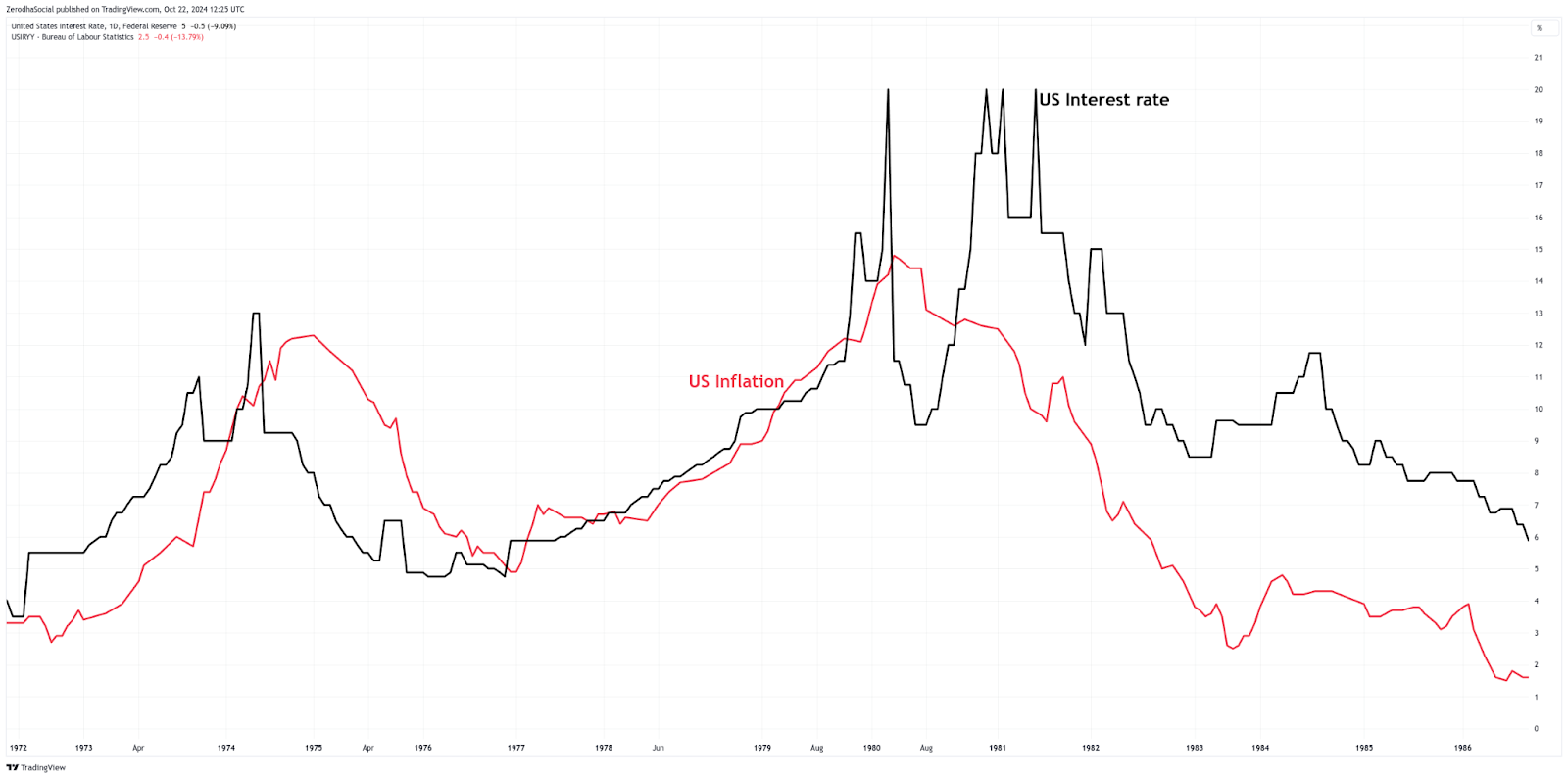

To explain his concerns, Druckenmiller brings up the 1970s. Back then, inflation was a major issue, just like today. At one point, the Fed eased up on interest rates too soon, and inflation came back even stronger. It wasn’t until the late 1970s, when Paul Volcker, then the Fed chair, raised rates to nearly 20%, that inflation was brought under control. It was tough for the economy, but it was necessary.

Druckenmiller isn’t saying we’re facing the exact same situation now, but he worries the Fed could make a similar mistake by easing up too early.

Druckenmiller also touched on the upcoming U.S. election. While he says he’s not too focused on politics, he believes the market seems to be expecting a Trump win. He points out that rising bank stocks, climbing cryptocurrencies, and gains in other stocks that usually benefit from deregulation suggest that investors are betting on a Trump victory.

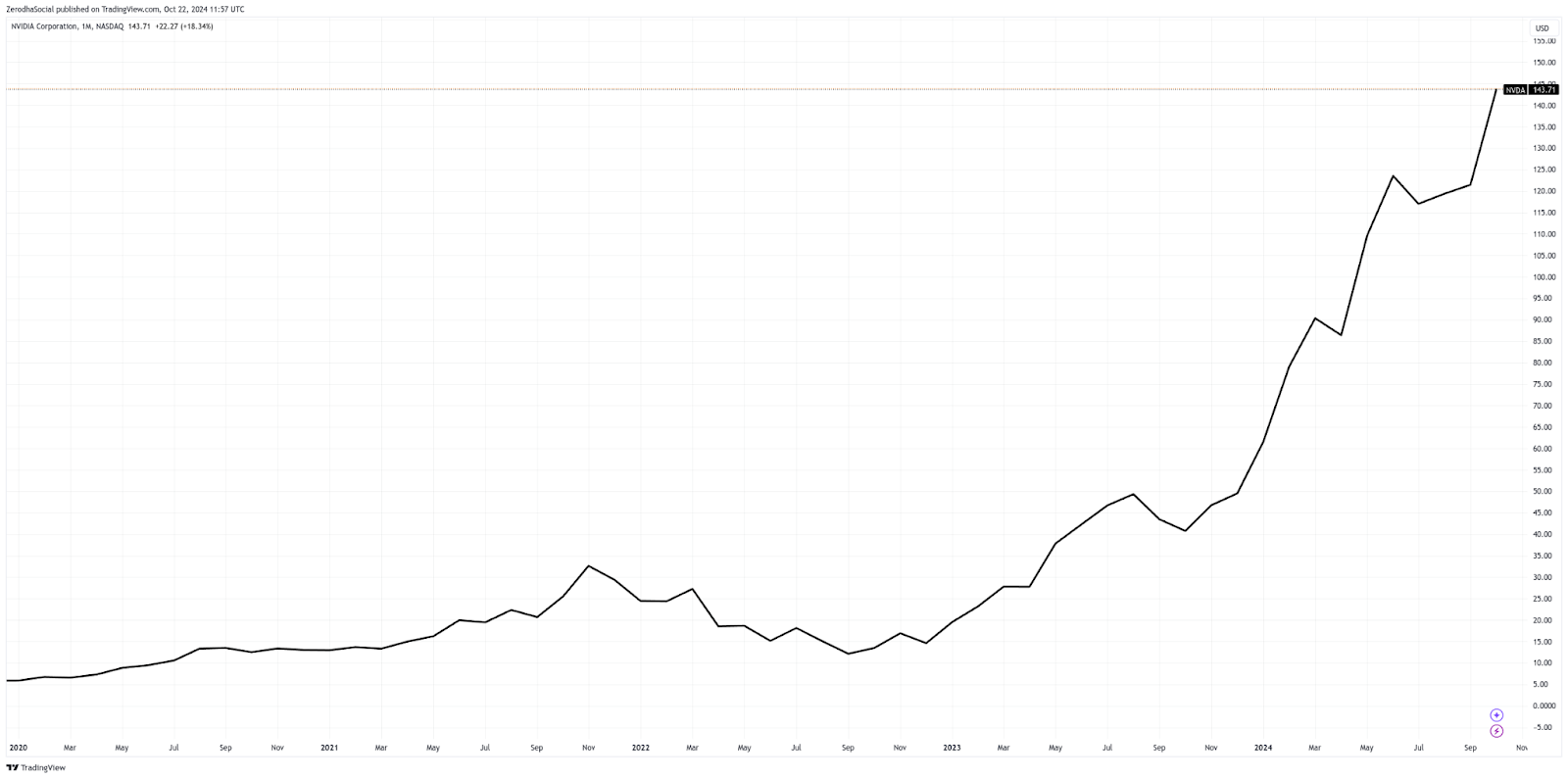

Druckenmiller admitted to a mistake he made with NVIDIA, selling his shares after the stock tripled because he thought it was overvalued. Today, the stock has gone even higher, and he acknowledges the misstep. However, he remains confident in AI and is now focusing on investing in the infrastructure that supports its growth.

Finally, Druckenmiller spoke about his next big bet—shorting bonds. To put it simply, he’s betting that bond prices will fall, which would cause bond yields to rise.

His reasoning is that if inflation keeps climbing, bond yields could rise significantly. And even if the Fed is right and inflation doesn’t spike, he believes the downside risk is small. He’s basing this strategy on the idea that the 10-year bond yield tends to follow the trend of nominal GDP, which is currently around 5.5%.

In summary, Druckenmiller’s interview raises some serious concerns about the direction the Fed is taking. He’s worried about inflation, thinks the Fed might be making a big mistake, and is positioning himself for what he believes could be some significant changes in the financial landscape.

Tidbits

- Ambuja Cements is acquiring a 46.8% stake in Orient Cement for ₹8,100 crore, at a price of ₹395.40 per share. This move boosts Ambuja’s market share and brings its capacity closer to 100 MTPA by FY25.

- PB Fintech’s subsidiary has received approval from the RBI to operate as an Account Aggregator. This expands its fintech offerings and strengthens its position in India’s financial ecosystem.

- Hyundai Motor India’s shares listed at a 1.3% discount, despite strong demand from institutional investors. Analysts, however, remain optimistic about the company’s long-term growth potential.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()

If you have any feedback, do let us know in the comments