If you’ve watched Zindagi Na Milegi Dobara, I’m sure you’re familiar with the term BPL (Bum Pe Laath). I’m just trying to bring some context to BNPL (Buy Now Pay Later) and BPL (Bum Pe Laath). We’ve seen so many players from across industries starting BNPL, which is evidently a massive industry. Why I thought about writing this piece is because of my frustration hitting the roof on this because of Apple Pay.

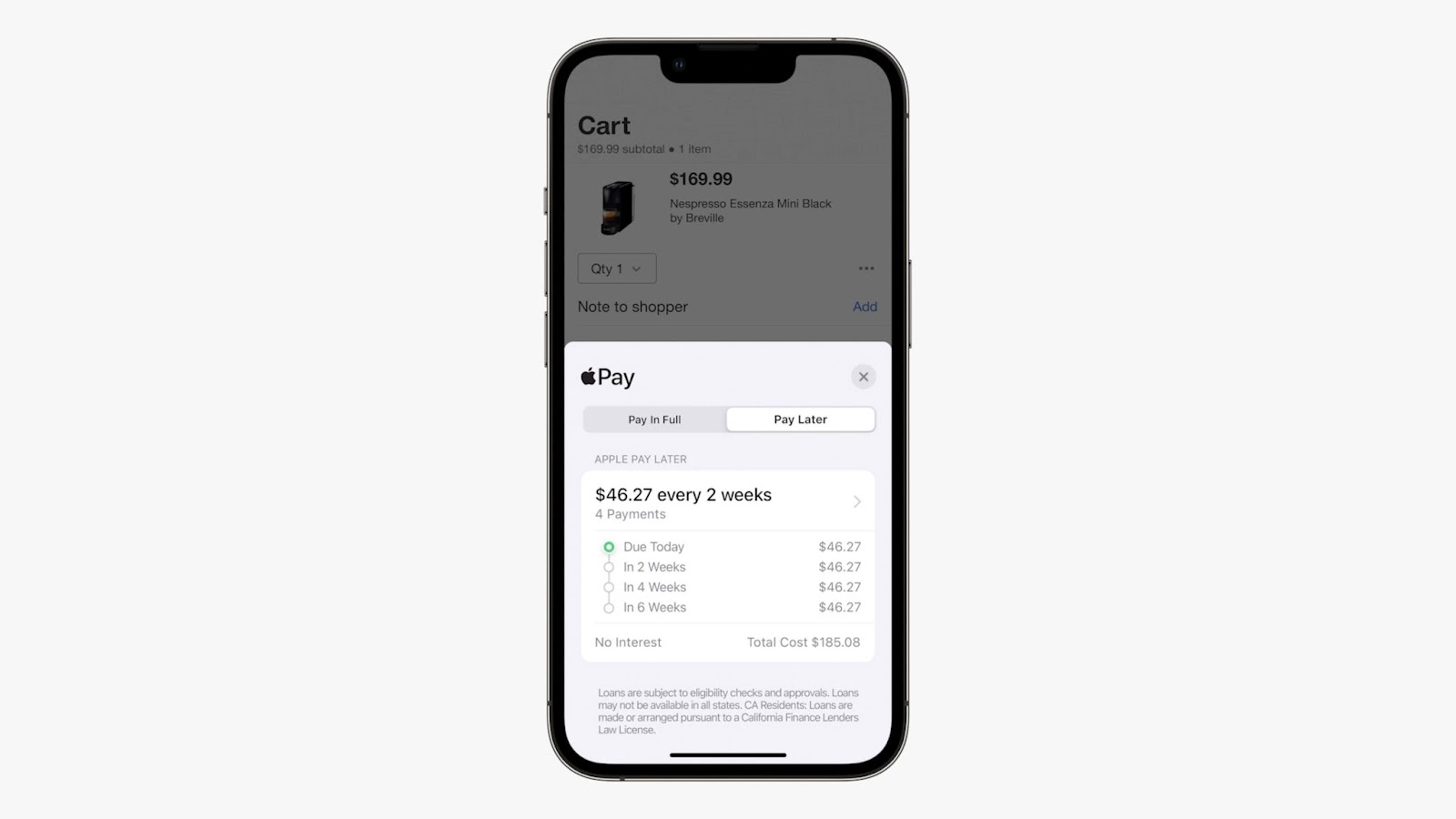

Apple just announced that you can split up your purchase on Apple Pay into four payments at no interest, I realized I just had to vent this out. Apple Pay has just announced a major update called Apple Pay Later, which will allow users to split the cost of an Apple Pay purchase into four equal payments over six weeks without interest or late fees. The new financial product–which was rumored ahead of its debut at Apple’s 2022 Worldwide Developers Conference (WWDC)–marks Apple’s move into the enormous and growing buy now, pay later (BNPL) industry.

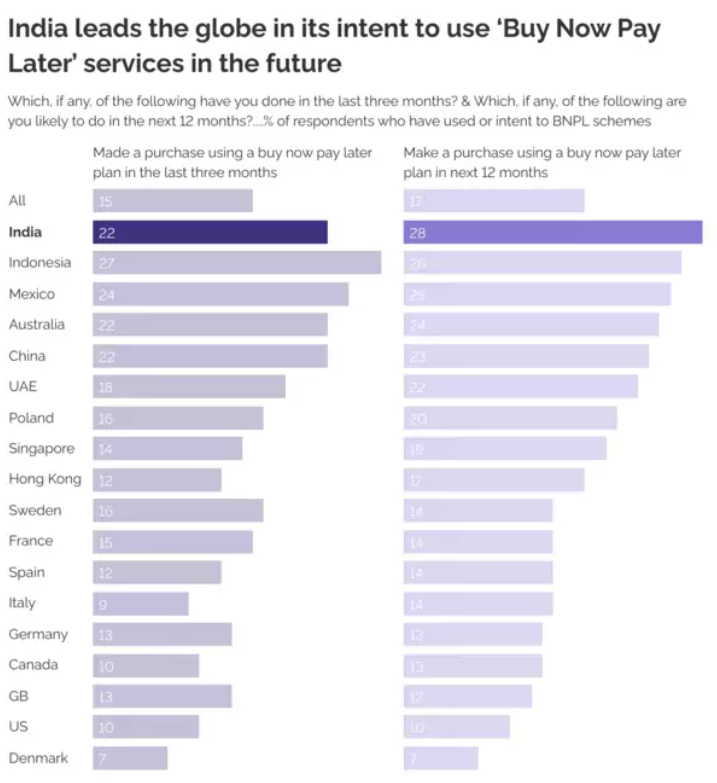

Even in India, BNPL is becoming seemingly gigantic. With the likes of Simpl, ZestMoney, LazyPay, Amazon Pay Later, Paytm Postpaid, Flipkart Pay Later, etc., BNPL payment in India is expected to grow by 89.5% on annual basis to reach US$ 6.92 billion in 2022. That is huge! While the BNPL services have been around for quite some time, it is the global pandemic that has propelled the adoption and growth of the BNPL industry in India. With over a billion consumers and a large credit-averse population, BNPL is expected to disrupt the payments sector in India.

Risks Associated with BNPL

BNPL is not without some risks. To begin with, there is credit risk, which can be further subdivided into customer risk and merchant risk. The customer may not be able to make the payment due to a lack of funds or even forget to pay. The BNPL provider takes full ownership of both customer and merchant risk, and so stands to lose a considerable amount of money.

Now, this part is scary; the space does not yet have regulatory frameworks governing it. This could lead to overcharging by the provider. The absence of regulatory checks could allow providers to take advantage of loopholes in consumer protection laws to provide illegal loans. Here’s a nice discussion on BNPL, and if it’s better than Credit Cards.

For example, BNPL is sending the TikTok generation into a tizzy! This is a very interesting yet concerning article. In 2021, Americans spent more than $20 billion through buy now, pay later services, an ever-increasing chunk of the $870 billion-a-year online shopping pie.

“In California alone, 91% of all consumer loans issued in 2020 — defined by the California Department of Financial Protection and Innovation as loans for “personal, family or household purposes” such as car, utility or medical loans — were buy now, pay later loans, also known as point-of-sale loans.”

Don’t do it.

What to take away from this article is simple, don’t be a simp for products or services you cannot afford. BNPL marketing is such that these companies marketing these products suck on every little wound you expose. While I’m a guy who doesn’t even spend on a lot of things even if I can afford them, I do realize how tantalizing it is to be shown a product you know you cannot afford and end up owning it. Instead, invest. Invest the money so it grows and gives you a free hand in buying these products without having to put yourself into debt. With the current market storm we’re riding, BNPL as a product is a huge risk. With job recession, inflation, etc., in the line, these services should ideally be a no-no. It is definite BPL later.

It might be done on the spur of the moment, but…