I did some math and want to validate this with people here and get expert comments

I invested in a GS-Bond for regular income with a coupon rate 7.35% for next 40 years(2064) now the yearly interest payout comes to 12k… and the cost of bond was 2.5L

Now if get Debt MF with 8% for the same amount 2.5L and do start a SWP after initial 3 years(to work around exit load) say for 12k annual… at the end of the of 40 years i will have 23L compared to 2.5L of bond…

If you look at the Tax implications they are the same for both instruments, with 2023 rule applied.

Now i know the difference is power of compounding etc etc, but the question is why are people still buying bonds??

How is a bond with coupon rate of 7.35% giving you less than 5%?

if you bought Rs. 2.5L bonds you should be getting around 18,375 as interest.

Check again, you are missing something.

This is extremely hypothetical, because you are completely ignoring interest rate risk

Debt MF might be giving 8% today, there is no guarantee that it will give 8% for next 40 years. Chances are over the years interest rate will fall and your math will change completely.

This is 30% tax adjusted So 18k become 12K should have cleared that…

You are right for Fixed vs Variable Interest part even if i move it down in the range of 5 to 8% compounding is still winning, also when i say debt MF these are Credit Risk Debt if you look at CAGR for ICICI Pru over lifetime its 7.5% and again i can swap out debt to equity for more volatility but higher rate…

What i wanted to convey was 2.5L investment are inflation adjusted when they are returned back to me in 40 years compounded with whatever the interest rate vs bonds which will be fixed at face value approx 2.5L with this understanding why bonds?

This is another reason right here

Not everyone is in the 30% income-tax bracket.

With the first 5L income (or is it 7L now?) being tax-exempt?

someone without any other source of income

can invest upto 70L (1Cr now?) into such GSECs at 7-8% returns annually,

and not have to pay any income-tax on the GSEC interest income, right?

Yes.

I was trying to highlight that the math needs to be redone.

Just because you end-up with 12K in-hand doesn’t mean everyone would.

…and the folks who end-up with 18K in-hand, have a stronger reason to prefer GSECs. (or a weaker reason to prefer Debt-funds, depending on how one looks at it)

Can you redo the math with 18K SWP

and share the relative difference of the remaining lumpsum at the end ? (likely the difference is significantly lower than the diff between 23L vs 2.5L)

Next we review

whether that difference

is worth the difference in risks between the 2 financial instruments.

Without even knowing the exact specific debt-fund being evaluated,

IMHO GSECs score favorably compared to debt-funds,

in terms of these two risks -

risk of not being able to lock-in the current interest-rate?

risk of some mishap/mismanagement in the debt-fund house?

Depending on how one evaluates such risks,

there will be other differences between the risk-profiles of these 2 financial instruments.

PS: These days, when comparing investment opportunities, my favorite goto is -

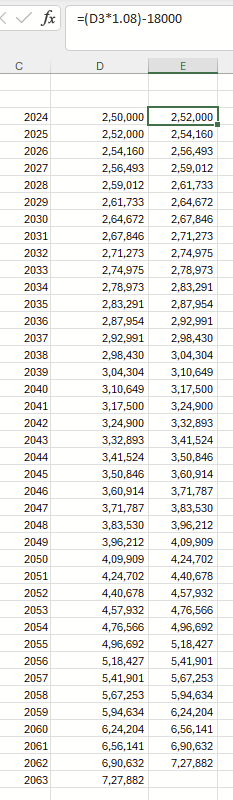

It come to 21L instead of 23L Given 8% compounding Staring with 2.5L No withdrawals for first 5 years then SWP for 18K/year

Comparing GSEC (Non Compounding) and Debt(Most stable Compounding) i see hardly issue again on paper given the reward to risk ratio

This can be subjective topic if stretched out and end up in analysis paralysis…

Again you are missing the risk.

If your question is why bond? My question is why Credit risk debt fund, simply go for equity fund you will get much better return over 40 years then what a credit risk fund can ever provide.

And then some smart kid who just started their investment journey will come and say why invest in equity fund, just do option trading you will be billionaire in 40 years

Point I am trying to make is from guaranteed return offered by almost risk free Gsec to credit risk bond fund to equity fund → risk changes.

And each investor has a different risk profile, so what works (or does not work) for you may not work for someone else.

Beside remember, such long dated Gsec are mainly bought by insurance companies, annuity provider etc. They have a need to get guaranteed cash flow and this product satisifies that need.

I would agree with you, but this is stretching conversation to the far end of the scale…

P.S: I am a kid when it comes to investments

I compared GSecs to DebtMF cause they give you almost same risk profile… but it has a magical 8th wonder as people describe it “Compounding” which Bonds lack.

Anyhow i understand the following from our conversation:

Risk is different (but more or less same in my opinion)

Returns are variable (but they will always be linked to inflation so final sum is still somewhat guaranteed to be close to inflation adjusted)

That’s an additional 90K that one does NOT have access to for the first 5 years.

Another major difference.

Can you find out what happens to the lumpsum number at the end

once we remove this initial 5-year lock-in (18K x 5)?

_(Sure, no actual financial instrument exists that supports this.

And once we see the numbers resulting from this change, we will see why

the ~21L comes down to ~7L if i am not wrong.

This is not a debt fund that invests only in Govt. securities.

So, we are introducing additional risks

risk of losing one’s entire invested capital (or a significant chunk of it).

risk of volatility (and the emotional impact of it).

risk of NOT having access to the funds when one needs them.

risks that

Essential even your principal is at additional risk here.

Unlike GSECs with sovereign guarantee.

Another difference is that GSECs can be pledged for trading margin.

That is something a lot of folks would use

I get the risk part i think everyone spoke of that enough…

Whats this didnt understand how 7L?

There is an exit loaf for MF not sure if i am hitting those percentages and STGC which is 1 to 3 yrs so playing safe and starting from 5yr onward, as mentioned in the original question…

What now you are asking me to play intraday or options with it for a guy who is asking GSEC and Debt MF

Updating the cash-flow match you had shared to - +8% - 18,000 starting from year1 (instead of a 5 year no-withdrawal clause)

to bring the cash-flow in-line with what is available with GSECs

that provide interest from year1.

Ok, if you feel that way, I can’t really change your opinion.

I will just share one example, and close this from my side.

Not sure if you ever heard about Franklin Templeton debt fund crisis around Covid period. If not, just google it and study it.

In short, FT debt funds were known to provide industry leading returns and were extremely popular with very high AUM.

Got massacred in Covid and they stopped redemption for almost two years. Eventually money was returned, but for almost 2 years, people could not access their own money.

Now if you want that 12K every month to pay monthly bills, how would you survive for 2 years if your SWP is stopped?

As a retiree I would prefer that I get guaranteed cash flow with peace of mind rather than being happy about a corpus I will get at end of my life

Oh yes. Absolutely.

Am genuinely excited to share whatever i could think of

The “almost” is doing a lot of heavy lifting in that sentence.

Using that measure, this dude is “almost” chilling freely.

BTW, this is a known issue with human estimation/intuition. (similar to how traditional physics no longer apply,

as a body approaches a black-hole or the speed of light)

It is not immediately obvious (until one does the math)

that eliminating the no-withdrawal clause of 18K for the first 5 years (of the 40 years),

will result in a drop of 14L (21L → 7L) lumpsum at the end of 40 years.

Similarly,

comparing something that won’t happen 99.9% of the time

with something that won’t happen 99.99% of the time,

in such scenarios that are at such “extreme edges” in the universe of possibilities, It is not intuitive that a drop in 0.09% (99.99 → 99.9) makes something 10 times (10x) more likely to occur.

That “almost” is not “just 0.09%”, it is “just 10x” !

The 5 year clause is to avoid STGC and Exit load it can be 3 but a buffer to let compounding do the magic…

Again in my case and in most of users case no one retires like tomorrow so this clause is like the insurance that you have to buy years ago before office kicks you out of the group medical to reduce the premium so plan is word here for that 5 yr clause.

So i am less worried for the first 5 year.

This is where you are in my domain now , The thing is 99.99% where it wont happen and ya take 10x relative to that doesn’t move much of the needle…

But see i get it Risk is higher when you compare both of them and i agree to that…