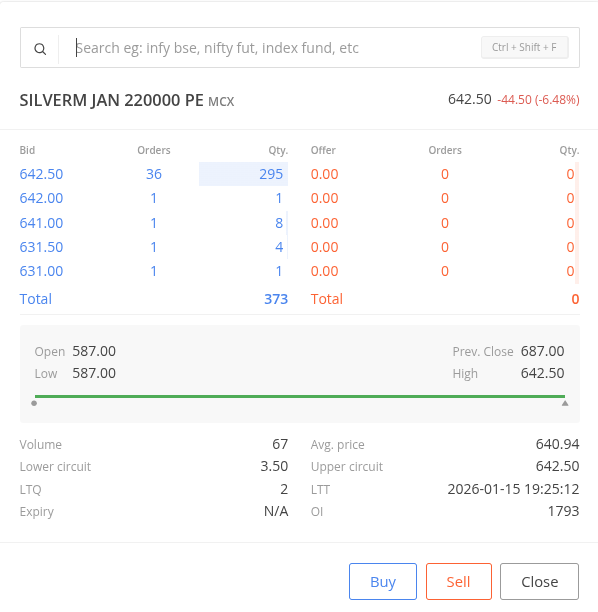

Pray tell me how this makes sense. Upper circuit is lower than previous closing price. It is stuck at this price for more than hour but the circuit still hasn´t moved.

As we receive circuit updates from the exchange, we have sent an email seeking clarification. The previous close may be correct since it’s based on the theoretical price, but we’re checking why the circuit was revised late or at that specific time.

3 Likes

Thanks @Adarsh_Patil for checking.

The previous close price in this case is mostly correct. It is usually the case with deep ITM options that the theoretical price is required, but this is a liquid OTM option.

thanks

We haven’t received a reply yet, but here’s the answer:

The upper and lower price bands are determined using a statistical method based on the Black-76 option pricing model and are relaxed in accordance with movements in the underlying futures contract; it has nothing to do with the previous close. In the event of frozen price ranges even without a corresponding price relaxation in the underlying futures, the Exchange may relax the Daily Price Limit if deemed necessary, considering volatility and other factors in the option contract.

This didn’t just happen that day. You’ll see the previous close is above the upper circuit today as well.

This is actually fair because for deep out-of-the-money (OTM) options, the exchange has allowed trading within the fair price range.

4 Likes

hmm… don’t think I agree with them. In this case, the expected volatility is clearly high, though the actual volatility of recent past might be lower. People are waiting for events and need to buy these options for hedging or other purposes, but unable to do so. At least they should give a higher spread around their calculation of the fair price.

1 Like

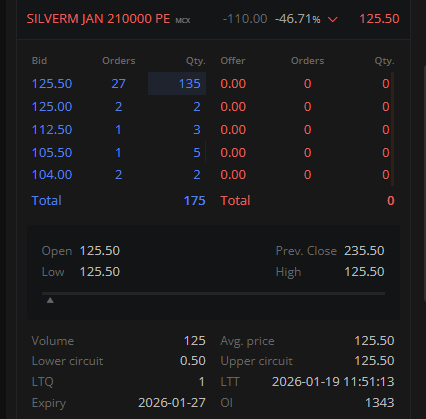

Silver trading at 303,917 and Strike at 210,000, the market is 93,900 points away from the above strike. Mathematically, with only 8 days left to expiry, even with 60% volatility, the Black-76 theoretical value of this option is only ₹0.52

The current limit is ₹175.50. That means the exchange is allowing the option to trade at 35,000% of its fair value. They have built in a safety buffer for a 18% Silver crash in a single day (using a 4.8 Sigma stress test, far higher than the standard 3.5 Sigma).

If they widened the limit further, they wouldn’t be helping hedgers; they would be allowing retail traders to buy a ₹0.50 asset for ₹300. The circuit is there to prevent a liquidity trap where buyers pay phantom prices that have no mathematical reality.

4 Likes

I think you underestimated silver volatility at 60%, where 11% drop from high just happened a few sessions back. A quick 2-3 such serial sessions “could” drop it well beyond strike price. The ATM option is already trading at 80% volatility. Deep OTM option generally do command higher volatility. Even ATM US COMEX silver options trade at 86-90% expected volatility. I think volatility of USDINR should also be taken into account. At 175 for 210000PE, market expects a volatility of 112% for that option. This is similar to COMEX options at 64$(~210000PE/8dte). While I agree that this is probably because of low volumes and that it is heavily overpriced rather than the actual expected volatility, I disagree with the quantum that the actual fair price is as different as 0.5 and 300…

1 Like

18% in a day… you say?

Oh really?!

Yesterday was one of those rare days, and we might see the same tomorrow

That’s what the exchange says, at least. In India, regulators have a lot more control over these things compared to other markets. Personally, I believe a free market shouldn’t have circuit limits, but I know that comes with a cost. The exchanges use them to prevent errors and protect traders from scams or extreme manipulation.

1 Like