Financial preparedness is a crucial parameter to consider while investing. An emergency fund can help you tide over unforeseen costs and ward off debts.

These unforeseen costs could be in the form of:

- Medical expenses

- A job loss

- Repair work to your home or car

- Unexpected travel expenses

In short, an emergency fund portfolio should meet this checklist:

-

Is it liquid : Liquidity refers to how quickly your investments can be converted to cash. Invest in instruments that do not attract high penalties or exit loads.

-

Does it prioritize safety over returns: It needs to be relatively less risky during market ups and downs. Avoid saving in instruments that have a high risk for capital erosion, instead, prioritize safety over returns.

-

Low correlation with other asset classes: Your investment portfolio has several asset classes, it’s important to evaluate how your emergency fund fits in with the rest of your portfolio.

-

Does it match your risk appetite : If you are conservative and have a low threshold for risk, you might want to consider a higher sum dedicated to your emergency fund.

-

Is it separate: It should be separate from the funds dedicated to long-term or short-term goals. This keeps you from tapping into mutual funds reserved for long-term goals.

Where to invest

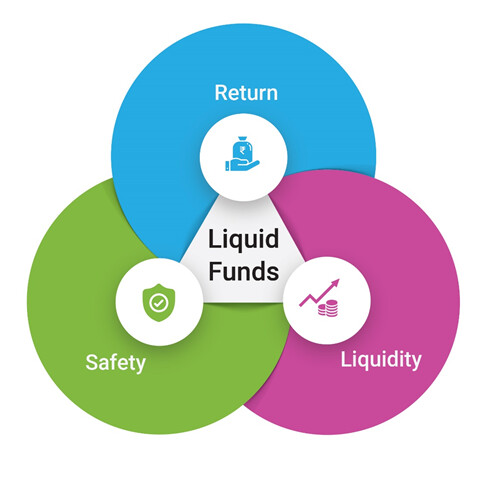

Consider financial instruments that follow the SLR (safety, liquidity, and return) philosophy while building this corpus. In short, you need to prioritize the safety and liquidity of your money over returns.

Consider switching to Liquid Mutual funds for building your emergency corpus.

What is a Liquid Fund

A Liquid Mutual Fund is a debt fund that predominantly invests in liquid money market and debt securities which are of short duration maturity of upto 91 days. The invested money is parked in market instruments such as Certificate of Deposits (CD), Commercial Papers (CP), Government securities (G-secs), Treasury Bills (T-Bills), and so on.

Liquid Funds are named so because it offers high liquidity of the capital for its investors. Some liquid funds can be redeemed within 1 business day. It is not overly sensitive to the interest rate changes due to its short duration and is relatively less volatile than other types of mutual funds.

How do you start

You can have an emergency fund as the base of your investment portfolio. It is the first step that you need before you plan to invest in other avenues that help you achieve your goals.

How much to set aside

The size of your emergency corpus must be in tandem with your lifestyle and risk tolerance.

If you are a very conservative person, you might want to keep a higher sum to deal with any financial emergency. if you are young and have no significant financial obligations and dependents yet, you may set aside only six months of expenses for emergencies.

As a general guideline, you need to have enough money to keep up with your consumption pattern for at least six to 24 months. For example, if your monthly expenses are Rs 100,000 then your emergency fund could be 100,000x12 = Rs.12,00,000.

If you are beginning to save, you can start with one month and then gradually build it up from there.

In short, an Emergency fund acts like your backup plan and works like a reset button to get your financial health back on track.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.