Hi,

I want to know what can be the reasons for increasing or decreasing the spreads between current month and near month futures.

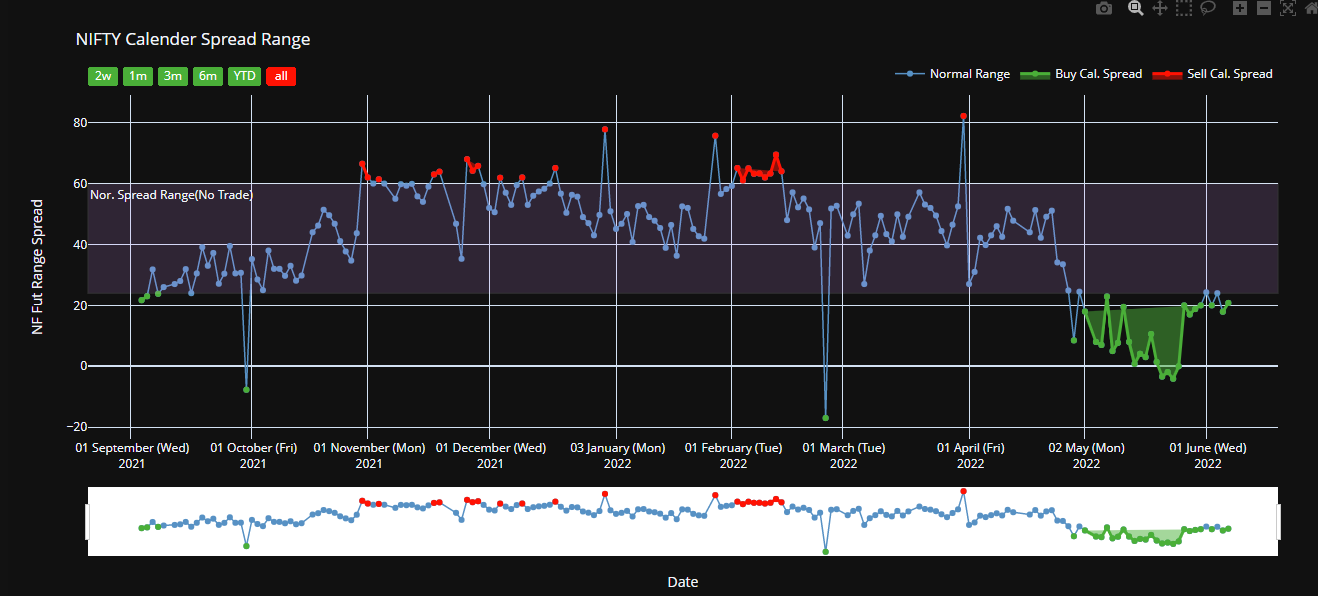

I read about calender spreads on Zerodha Varsity.

NF Futres continuous chart which is determining when to execute calender spreads based on last 8 months of data.

https://divyankm.github.io/Stock-Exchange-Data-Analysis/html%20files/NIFTY_FUT_Calender_Spread.html

Snap-

++1

Some more charts and literature on calender spreads:

Queries:

-

I want to know what can be the reasons for increasing or decreasing the spreads between current month and near month futures.

-

Will current month Fut contract requires additional margin on Day of Expiry for Calender Spreads as well, though it is hedged with Next month Future Contracts?

Margin Policy: What is Zerodha's policy on the physical settlement of equity derivatives on expiry?

Our margin policy

| Day (BOD-Beginning of the day) |

Margins applicable |

| E-4 Day (Friday) |

10% of VaR + ELM +Adhoc margins |

| E-3 Day (Monday) |

25% of VaR + ELM +Adhoc margins |

| E-2 Day (Tuesday) |

45% of VaR + ELM +Adhoc margins |

| E-1 Day (Wednesday) |

25% of the contract value |

| Expiry Day (Thursday) |

50% of the contract value |

https://divyankm.github.io/Stock-Exchange-Data-Analysis/frontend_html_files/cal_spread.html