Dear All, I am very new to options. has been watching closely all the activities. Tried to understand the option greeks but still noob.

my query is that when expiry comes near, why call premiums are so different for both PE and CE even having same strike price.

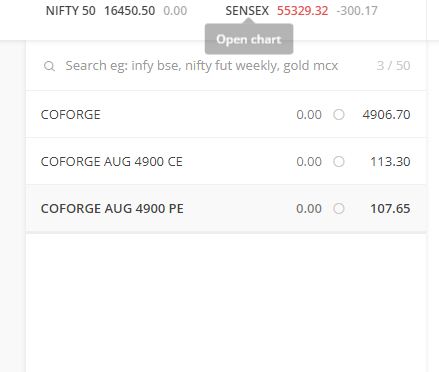

for example

today 21 aug 21

4900 coforge AUG CE is 113.3 but the cost of 1 lot is 68000 appx and

4900 coforge AUG PE is 107.65 has the cost of 21000.

both have 1 lot of 200 shares.

why is this difference when the prices are very close and same strike price.

when I see same strike price for Sept expiry, the price is approx same for both CE and PE.

please assist me . thank you.

First, let me correct you if the CE price is 113.3 then the cost to buy will be 200*113.3 = 22,660, not 68000. The same way also cost for PE is incorrect.

I doubt you provided the correct CE and PE price. I think it must be CE = 107.65 and PE = 113.3.

Now come to the original question, why do prices differ?

See the options prices depends on many factors such as time left for expiry and Implied volatility.

Generally implied volatility (IV) for PE is always higher than that of CE. That means that people are always fears of falling of share and therefore they keep the higher premium for the PUT option.

You can see the effect of various parameters on option prices using the Black Scholes Calculator.

I am attaching the link for the black Scholes calculator. Zerodha - Black & Scholes calculator

Thank you

I really appreciate your prompt reply Sir. attaching the SS taken just now. CE is 113 and PE is 107 and if you check on kite, CE is of 67000 and PE is of 21000.

See, these stock option are not so liquid and these price are LTP (Last Traded Price) which are keep

fluctuating at the last minute (because of supply and demand) of closing and therefore this could happen.

The cost (margin) is high because these contract will be physically settled on expiry (if you not squared off before expiry) and therefore requires additional physical delivery margins.