Suppose I am a salaried employee and also have Non-speculative and speculative income.

Profit in Non-speculative business = 5.5 lakhs

Profit in speculative business: 2 thousand

Salary Income = 43 lakhs

Other income: 2.5 lakhs (dividend and FD)

Turnover 58 lakhs

Last year’s non-speculative loss = 2.3 lakhs

Last year’s speculative loss = 1 lakh

Questions:

Can I opt for presumptive taxation 44AD in this case? (salary income + trading income). I want to opt for presumptive taxation as I will have to pay tax only 6% (online transactions) for the trading which is 3.5 lakhs which is less than my actual profit of 5.5 lakhs

What happens to the last year’s non-speculative and speculative loss if I opt for presumptive taxation? Will I be able to carry forward it?

What will be the turnover in my case? 58 lakhs (only trading turnover) or the 58+43 lakhs (Salry + trading turnover)

What would be my total taxable income if I opt for presumptive taxation? (58lakhs + 45.5 lakhs (salary and other source income) = ~1.1Cr) % 6% = ~ 6 lakhs?

OR

Is the preemptive taxation calculated only on business income? and do I need to pay taxation on my salary income separately?

Please suggest which option is suitable for me considering the above case

Here are answers to your various queries (Assuming the data is for FY 2022-23/AY 2023-24 under the old regime).

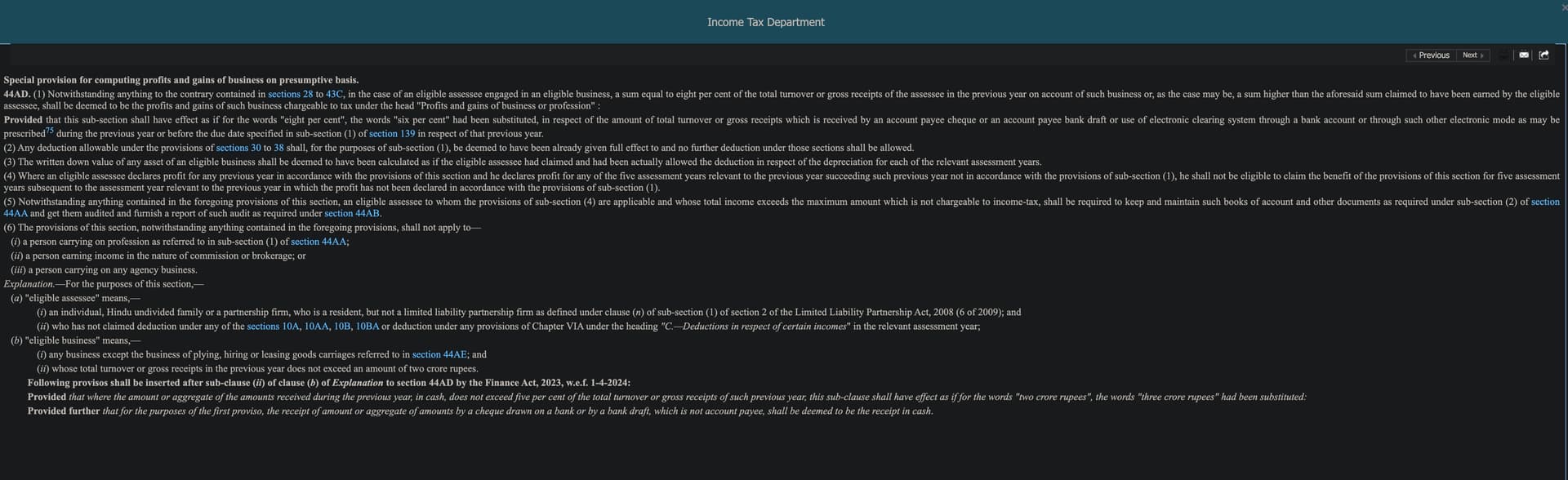

The Presumptive taxation scheme u/s 44AD is for small taxpayers with income under “Income from Business & Profession”. A person engaged in a business u/s 44AD can opt for the scheme if the turnover is up to ₹2 crores. They must declare profits of 8% / 6% of the turnover or actual profits, whichever is higher.

So, yes, you can opt for Section 44AD for online trading business. And, if your actual profit is 5.5 lakhs you have to report that instead of 6% of turnover.

Yes, brought forward losses will be first adjusted against current year profits, and if any remaining will be carried forward to future years which can be set off against the same head of income.

Turnover is only for business income. So it’ll be 58 lakhs only. Salary income shall be taxable under the “Income from Salary” head of 43 lakhs.

Presumptive taxation can be opted only for non-speculative business income. Salary income will be taxed separately.

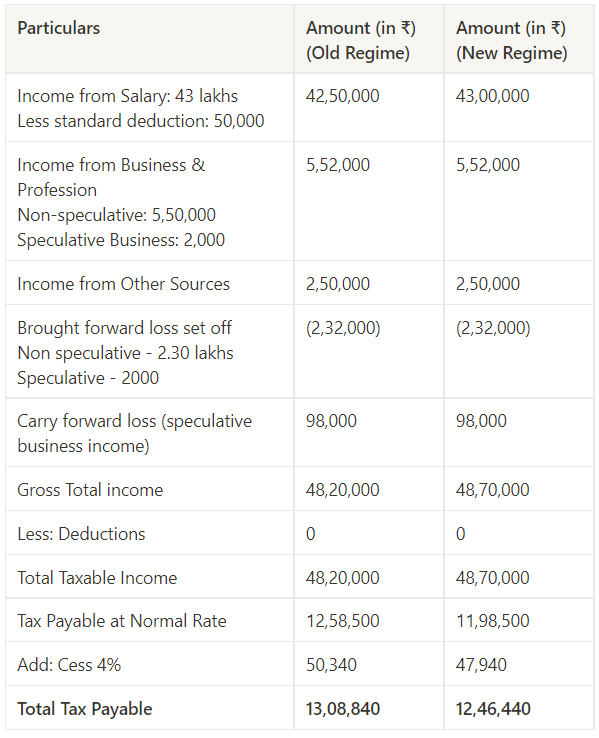

Computation of total taxable shall be as below under the old regime for FY 2022-23 if opted for the presumptive taxation scheme.

Thanks. Sorry I didn’t understand the below points

So, yes, you can opt for Section 44AD for online trading business. And, if your actual profit is 5.5 lakhs you have to report that instead of 6% of turnover.

My turnover is 58 lakhs and the profit is 5.5 lakhs. Why should I show 5.5 lakhs profit instead of 6% of 58 lakhs (turnover)? What is the advantage of opting for presumptive taxation then? I want to opt for presumptive only so that I will have to pay less tax (6% of 58 lac instead of 5.5 lac)?

Is presumptive taxation applicable only to the old tax regime?

This is dangerous, you might get IT notice. Report actual profits as all the trading related activity is through your PAN.

You cant (you can, but might get IT notice) show less profits when you know your profit is 5.5 lakh.

But then what is the advantage of opting for presumptive taxation? Only to skip bookkeeping and audit?

I saw many people on youtube have mentioned that we should use it to save tax. The main purpose of it is to save tax as well as the bookkeeping and audit.

Presumptive taxation scheme was introduced keeping in mind small traders/freelancers. It gives relief to the taxpayer of not maintaining any books of accounts.

As per the Income Tax Act, a taxpayer should declare at least 6%/8% of the turnover as profit and pay tax on the same if he is opting for the presumptive scheme assuming he is not maintaining books of accounts. However, if your actual profits are higher than 6%/8% you must pay tax on the same.

Presumptive Taxation scheme can be opted for under the old regime as well as the new regime.

Boss don’t go by everything youtube people say. Consult a CA. I highly doubt a qualified CA will advice you to evade tax by declaring low profits from trading in the markets. All transactions have paper trail. I really don’t know how the youtube people if they are doing it have not yet gotten any notice from IT department.

It isn’t explicitly mentioned that you have to declare the higher profits (word used is ‘voluntarily’), if it was, this issue wouldn’t always keep coming up.

Even CAs have differing opinion about this, so it’s really upto you, though it isn’t really advisable & you should be mentally prepared to receive a notice if you do decide to go for it…

As a trader you should be taking care of risk management. And an IT notice say 5 years down the line is a major risk - because you cant just say 'oh my bad, here’s the pending amount" - instead you will have to pay it with interest and maybe fine. That could be disastrous!

@Quicko@Jason_Castelino

Hi,

I am a fulltime regular profit making F & O trader since 7 years. I have no other income. I am posting here to clarify whether i am in the right path. Since FY 2021-2022, I am filing under presumptive taxation. I take the help of nearby CA for tax filing. Prior FY 2021-2022 I filed under regular business. In the middle of that financial year, I have closed my trading and demat account with a broker, and I had only the profit and loss statement excel and since the account is closed with the broker, i don’t have access to ledger statement of the broker. I contacted the broker, but they said since the account is closed, they cant do anything. I contacted CA and he said since the ledger is not available, i can opt for presumptive taxation and i don’t need to keep book of accounts and filed tax under presumptive taxation, my turnover was around 65 lakhs and gross profit was around 12 lakhs, and after deducting brokerage and other expenses, the profit came around 10 lakh and i paid taxes for 10 lakh income. For FY 2022-2023 i did the same for income of 11.5 lakhs and my return was processed. I am showing profits well above the 6 or 8% threshold, may be around 18 to 20%. i have interpreted 44AD profits as whichever is higher, so i have shown real profits.

My queries are

Q1. I saw in some of the posts in this forum, deductions are not allowed in 44AD, in that case do i have to show my gross profit without deducting my brokerage and other expenses like internet and telephone bills?

Q2. my CA quoted there was an advantage with 44AD that i can pay advance tax around by march 15, by which I can come to a conclusion, how much my income will be there for the current FY. In f&o trading, incomes are not consistent, for 3 qtrs. i may be in loss and in 4th qtr. i may be in heavy profits. This makes me pay advance tax with penalties if not opted for 44AD. for FY 2019-20 i had huge profits for the first 3 qtrs, i paid advance tax around 2 lakhs. 4th qtr was a disaster and i ended up with no tax liability. i had to wait around 1 year to get my refund, which was huge. already loss in 4th qtr and with 2 lakh dues to come, it was difficult for me to manage finances. So i was attracted to the method of advance tax in section 44AD. So is the advantage of advance tax without penalty true in 44AD?.

Q3. Apart from the broker related expenses, I incur additional expenses like attending traders meet or some kind or seminar at least twice in a year [digital transaction] . I have rented a small room situated in upstairs of a known person’s house, to work in it as a office by paying 5k per month including electricity expenses [cash transaction]. This was paid in cash. As the amount is less, the houseowner demands it to be given in cash. both the other expenses mentioned above, i.e. digital transaction not reflected in broker’s profit loss statement of around 30 to 40K and cash transaction of 60K [ no receipt] was deducted from the gross income and filed. Is this allowed ? My CA clarifies not to worry if rent receipt is not there , in 44AD as these are minor expenses.

will be happy and thankful to see my queries answered.

What you have mentioned is correct, section 44AD is for individuals whose turnover is up to 2 crores and they have not maintained any books of accounts. With regard to your query,

As per section 44AD since books of accounts are not maintained, one can not determine their business expenses. Hence while filing the ITR you just have to report your gross turnover/ receipts and actual net profit excluding all actual expenses incurred (subject to a minimum of 6% of your turnover as all transactions are digital). In the case of trading income, the financials can be maintained conveniently and hence actual profits can be reported under regular business income.

Note: If you opt out of the presumptive taxation scheme, you will be required to get a tax audit done and you will not be able to opt into the scheme for the succeeding five FYs.

Yes, 100% of advance tax can be paid until 15th March if you opt for the presumptive taxation scheme and there will be no penalty levied on the same.

If you report income as per 44AD then in the ITR you don’t have to give a breakup for your expenses and hence you can enter the actual profits after reducing expenses. However, if you maintain regular books of accounts then you have to give a breakup of expenses and in case any scrutiny arises, the onus will be on you to provide proof to the ITD relating to such transactions.

Have read the full thread and have below questions. FY24 is my first year of reporting F&O income. In previous years I have had minor losses but have not bothered reporting them, given daunting nature of reporting (I refer to non-presumptive and was not aware about 44AD then)

Since 44AD assumes presumptive income as a minimum fixed percentage of turnover, is it really possible to report losses under it? Logically you cannot have losses when there is presumptive income. How is it possible to setoff against losses in that case in later years. You also mention once we select a particular mode of reporting (presumptive), we are better off not changing it next year’s. So my concern that I select the right option to begin with.

Since presumptive income comes under ITR4, should we filing ITR4 and not ITR3 (everywhere on internet it’s mentioned F&O is business income and needs to be reported in ITR3)

Also hear experts in livemint etc saying 44AD is for small traders who don’t maintain books of account. But in our case broker keeps all accounts. Non-broker Expenses are separate, but does IT expect F&O Traders to consider their income as Presumptive? Although we report real profit and not 6% as stipulated as min under 44AD, will IT reject filing if we go for presumptive?

I would have preferred to go with non-presumptive but interest levied on taxes not advance paid quarterly is really troublesome. Ideally tax dept should change this rule since F&O income is not predictable within the year unlike Capital gains.

Under section 44AD, you need to report 6% of the turnover as profits or actual profits, whichever is higher, as income. Moreover, you can not report losses and hence, you cannot carry them forward either.

ITR-4 can be filed when you have income from presumptive business or profession, salary/pension, one house property, and interest up to INR 50,00,000. However, if you have income from capital gains as well, you need to file ITR-3. But, you can declare presumptive income in ITR-3 as well.

You can report the actual profits. Moreover, if you opt for presumptive taxation, you need to opt for it for the next 5 financial years continuously. If you opt out, you will not be able to opt back in for next five AYs.