Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Is India’s Economy as Strong as It Looks?

- Green Steel: India’s Game Plan for Sustainable Growth

Is India’s Economy as Strong as It Looks?

Over the past few days, we’ve been researching and writing about India’s performance in 2024 and its outlook for 2025. Both stories had a positive tone—not by choice, but because that’s where the data led us.

The Indian economy has shown steady growth, supported by strong foundations, resilient financial institutions, and companies with healthy balance sheets.

But history reminds us not to get too comfortable. As Murphy’s Law puts it: “What could go wrong, will go wrong.” So, we decided to dig deeper and see what risks might be lurking beneath the surface.

The recently released RBI Financial Stability Report gave us some answers. Think of this report as a detailed health check for India’s financial system. It looks at everything—from banks and households to market risks—helping us spot potential cracks before they grow into serious problems.

Here are three risks that could throw India’s economy off course. These might never happen, but staying informed and prepared is always better.

Household Finances Look Shaky

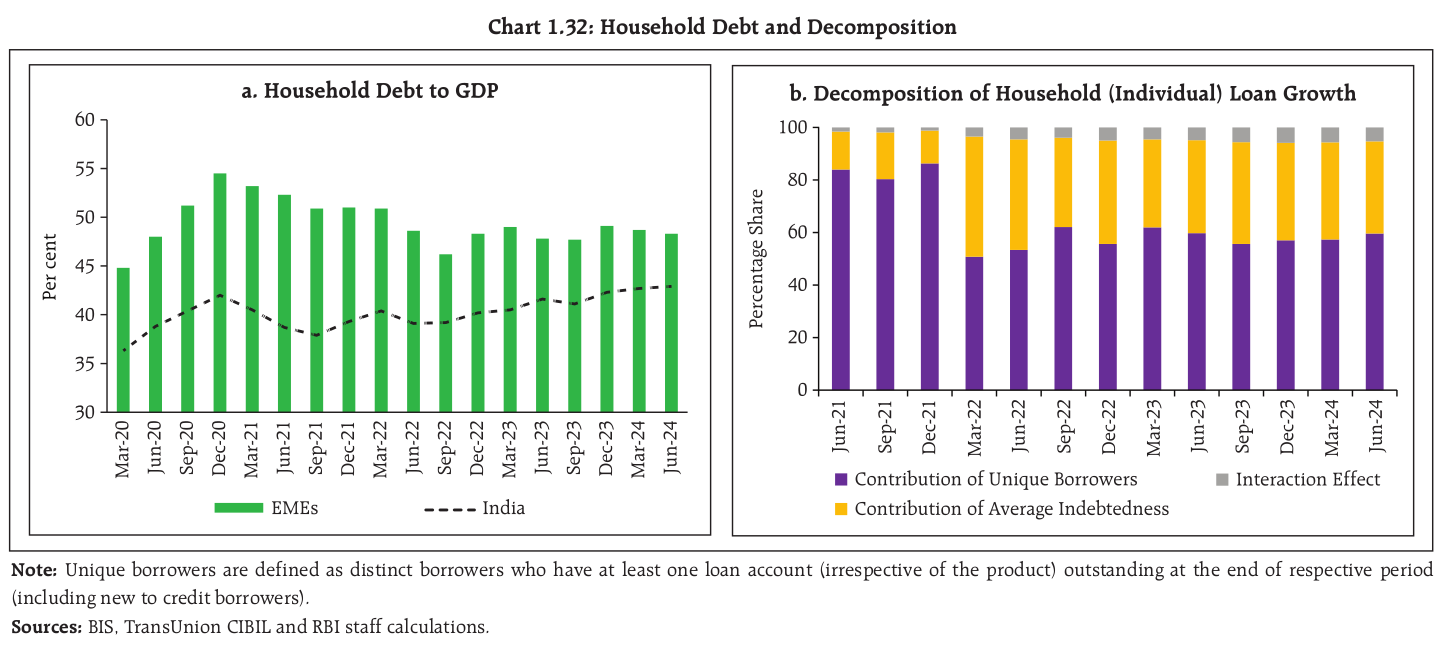

India’s household debt, at 42.9% of GDP, is still lower than in many other emerging markets, which often hover around 50–60%. However, this number has been creeping up over the past three years, even as household debt in other countries has been going down. Interestingly, this rise is due more to an increase in the number of borrowers than larger individual loans, which indicates better access to credit—a good sign.

Source: RBI

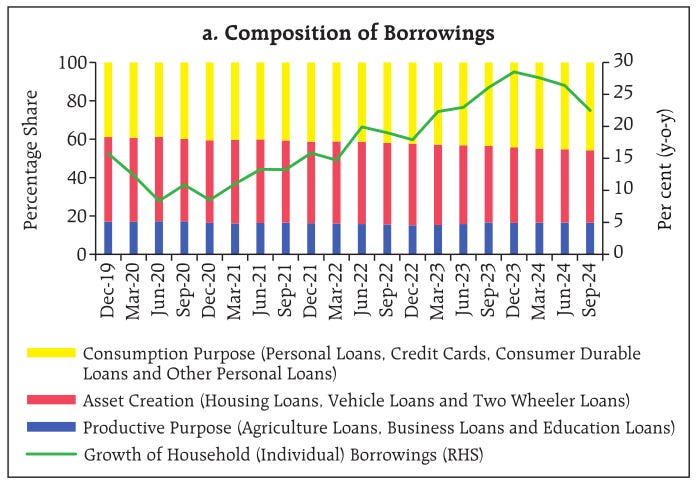

When we look at how these loans are being used, three main categories stand out: consumption (like personal loans, credit cards, and consumer durable loans), asset creation (such as mortgages and vehicle loans), and productive purposes (like funding agriculture, businesses, or education).

While consumption loans haven’t spiked, they are gradually increasing, suggesting that more households are borrowing to cover everyday expenses.

Source: RBI

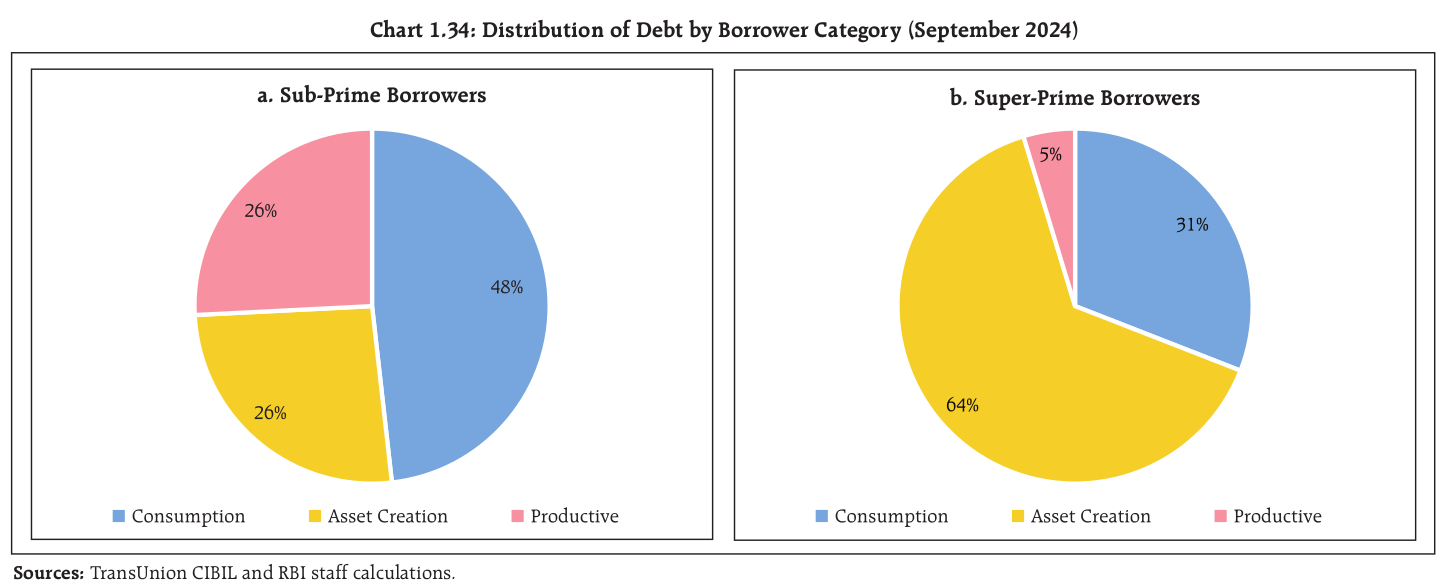

Another important factor is the type of borrower. Subprime borrowers—those with lower credit scores—spend 48% of their loans on consumption, compared to super-prime borrowers—those with excellent credit—who only use 31% of their debt that way.

The rest of the super-prime debt is typically invested in assets, especially housing. This contrast shows that wealthier, low-risk borrowers are more likely to build assets, while less financially secure borrowers may take on riskier debt that doesn’t generate long-term value.

Source: RBI

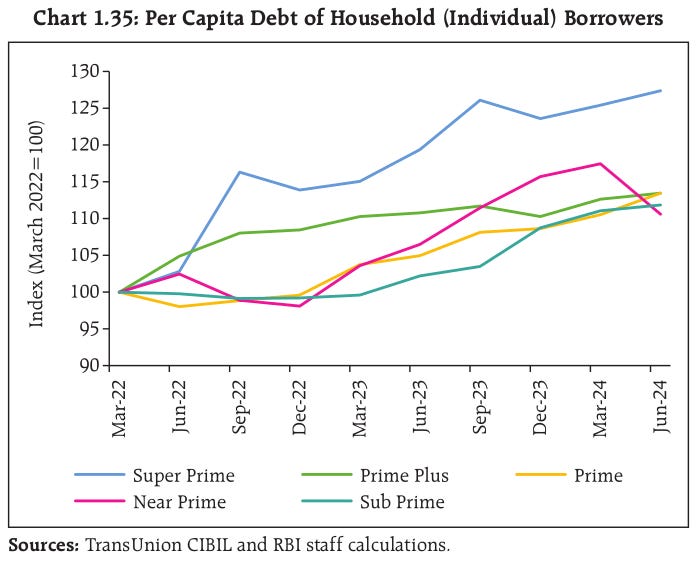

Per capita debt for super-prime borrowers has risen sharply, while it has remained relatively stable for other risk groups. From a repayment perspective, this is encouraging: high-rated borrowers are mostly using their debt to create assets, which strengthens their ability to repay.

However, the growing reliance on consumption loans among subprime borrowers could pose risks if they struggle to keep up with repayments. Keeping track of these trends is crucial for the overall stability of household finances.

Source: RBI

Pricey Valuations and Weak Corporate Earnings

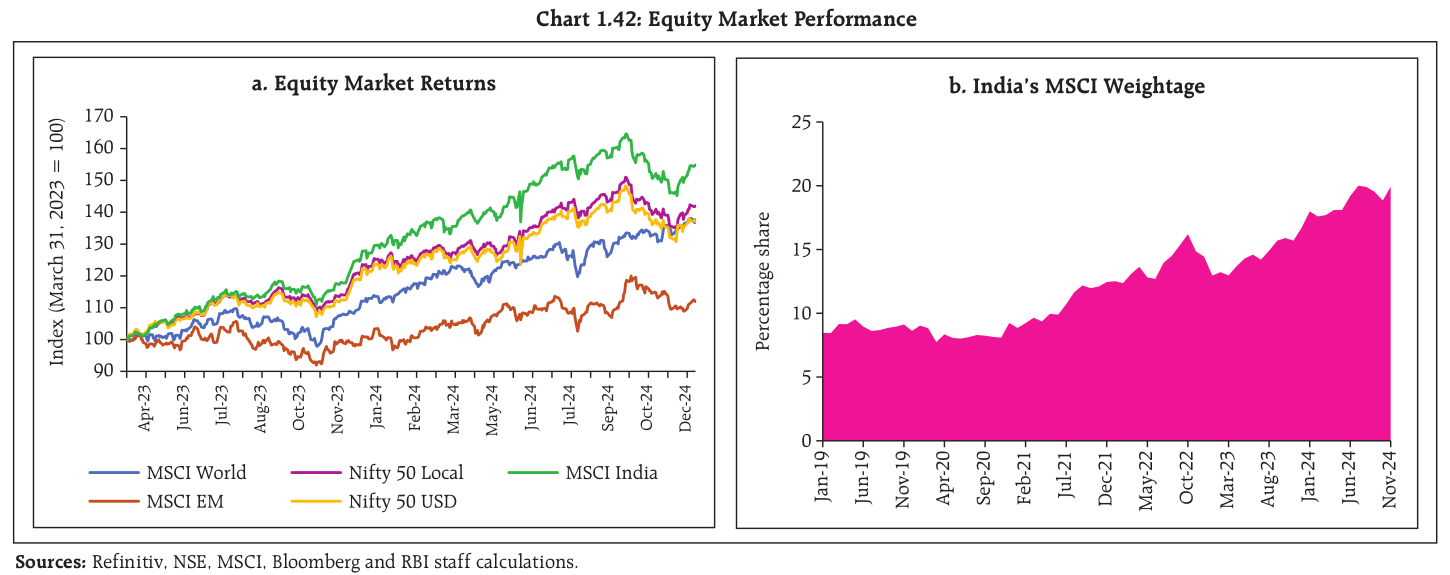

The Indian equity market hit record highs in late September 2024 but has since corrected due to slower corporate earnings growth and concerns about high valuations. Even with this pullback, India’s market outperformed its emerging market peers in 2024.

The MSCI India Index delivered a 19.5% return compared to 8.3% for the MSCI Emerging Markets Index (MSCI-EMI) as of December 12, 2024. This strong performance has more than doubled India’s weight in the MSCI-EMI.

Source: RBI

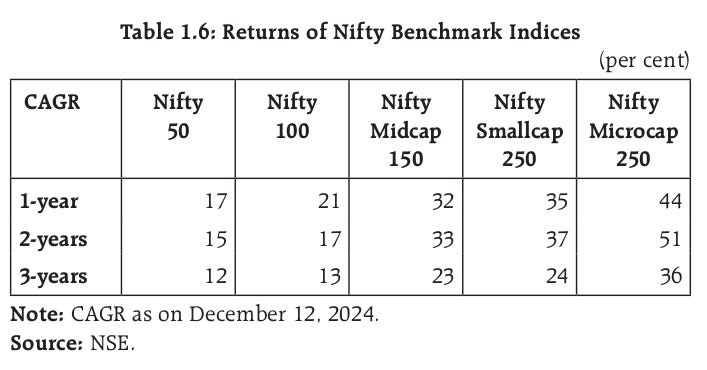

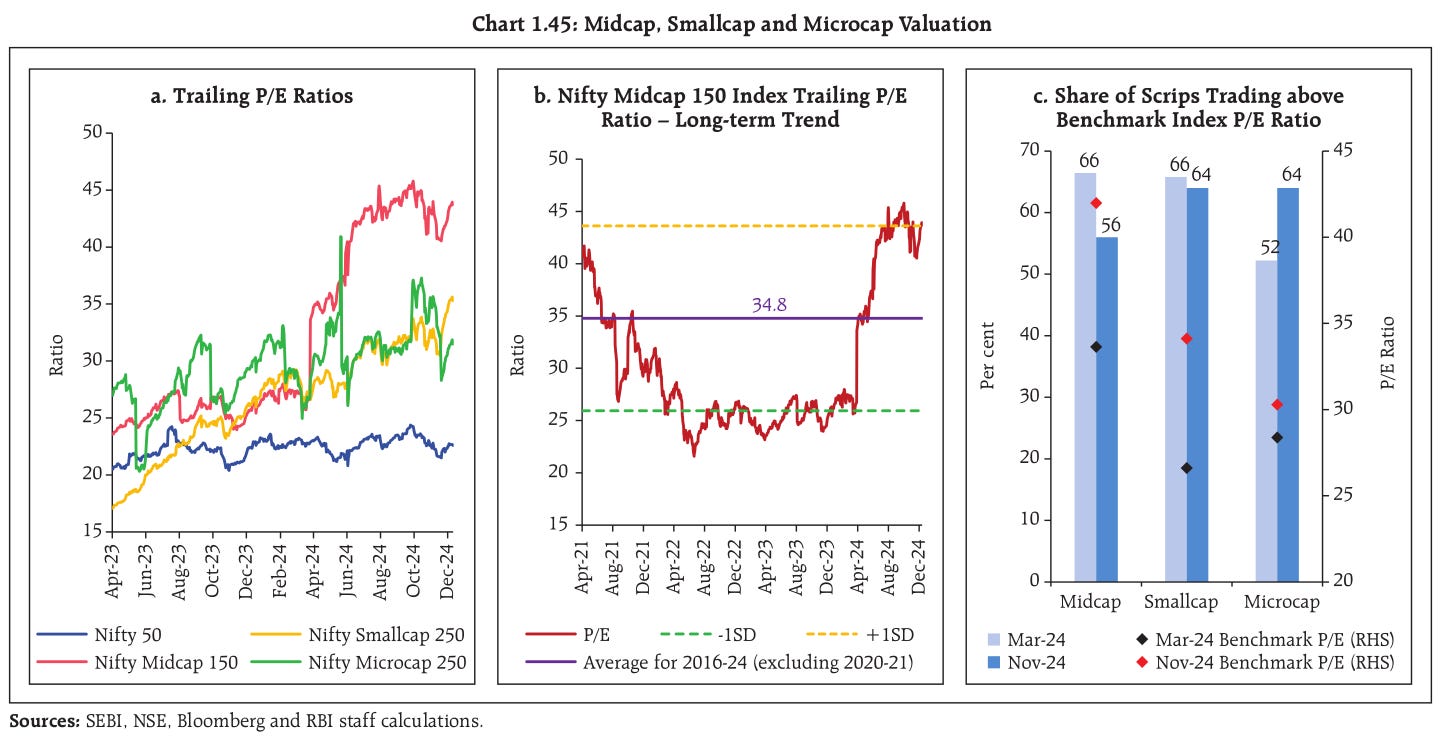

Midcap, small-cap, and micro-cap stocks have been the frontrunners, with returns exceeding 30%, far outpacing the Nifty 50 Index’s annualized return of 17%.

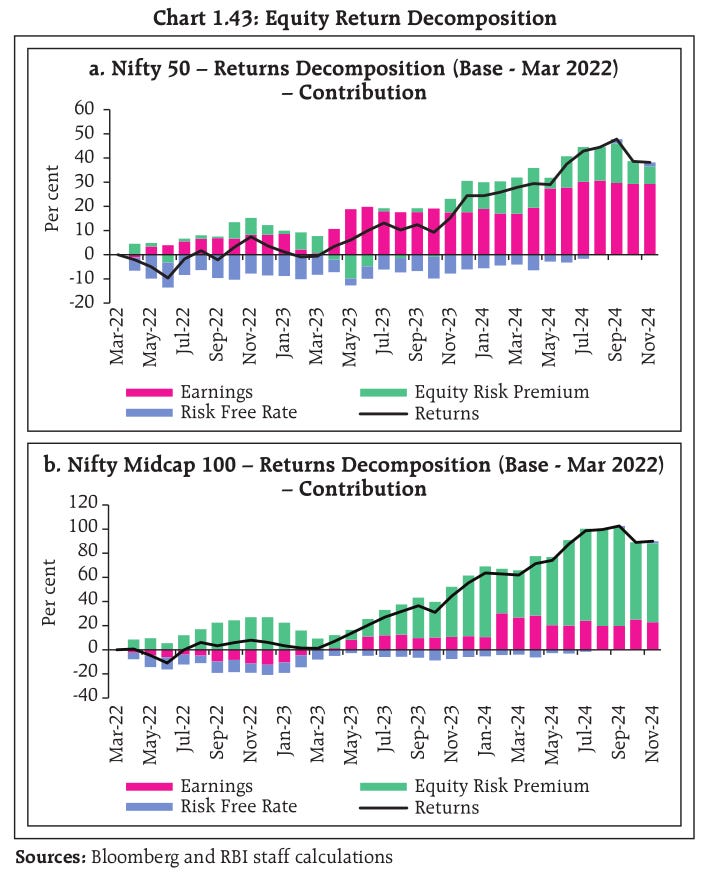

A discounted cash flow model in the RBI’s Financial Stability Report points out that a higher equity risk premium—indicating stronger investor appetite for risk—has driven the Nifty Midcap 100 Index. On the other hand, the Nifty 50 Index’s gains are more closely tied to actual earnings growth.

Source: RBI

What this tells us is that midcap and small-cap returns are being fueled more by bets on future potential than by actual earnings growth. While this shows strong optimism, it also comes with more uncertainty. If investors become cautious, midcaps could face sharper swings since their valuations rely heavily on sentiment rather than proven performance.

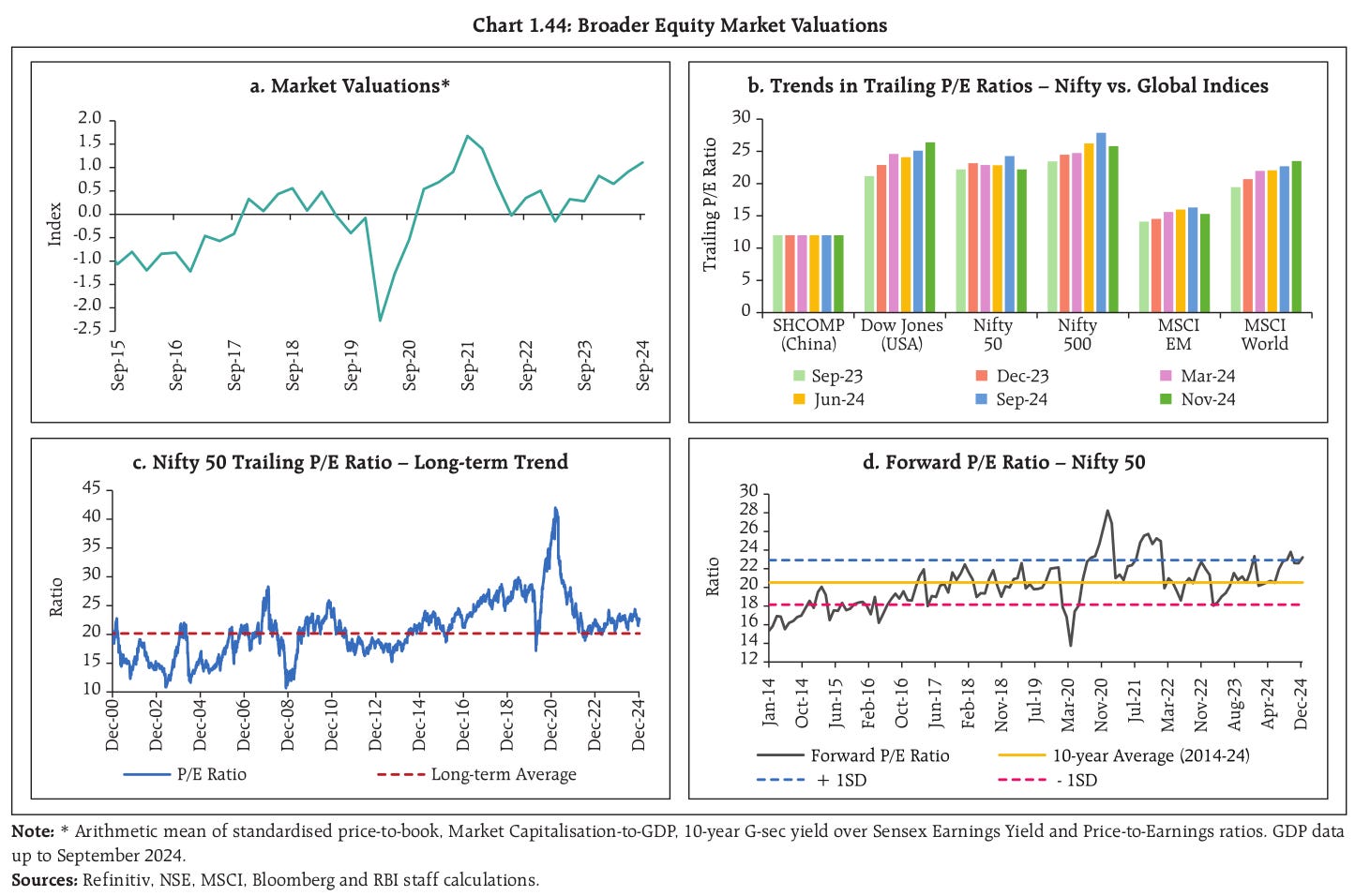

Even after the recent correction, equity valuations across several metrics remain stretched. This includes trailing and forward price-to-earnings (P/E) ratios, market-cap-to-GDP, and earnings yield. The small- and midcap segments are particularly overvalued.

Source: RBI

Source: RBI

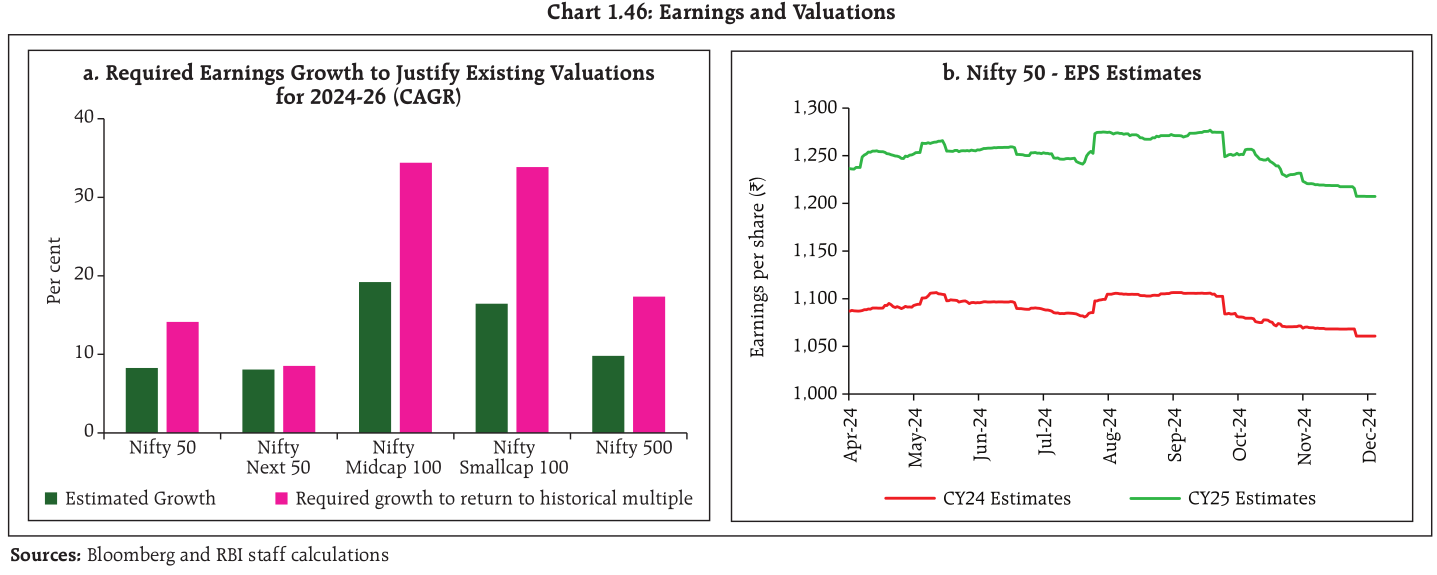

The RBI’s Financial Stability Report warns that these high valuations will only hold if earnings growth surpasses already lofty expectations. Otherwise, markets could see a swift correction. Recent Q2 2024–25 corporate results show slowing earnings growth, as reflected in EPS estimates.

For example, Nifty 50’s earnings growth is expected to remain below 10%, but it needs to hit around 14% or higher to justify current valuations. The gap is even larger for pricier indices like midcap and small-cap, underscoring their vulnerability if growth falls short of investor expectations.

Source: RBI

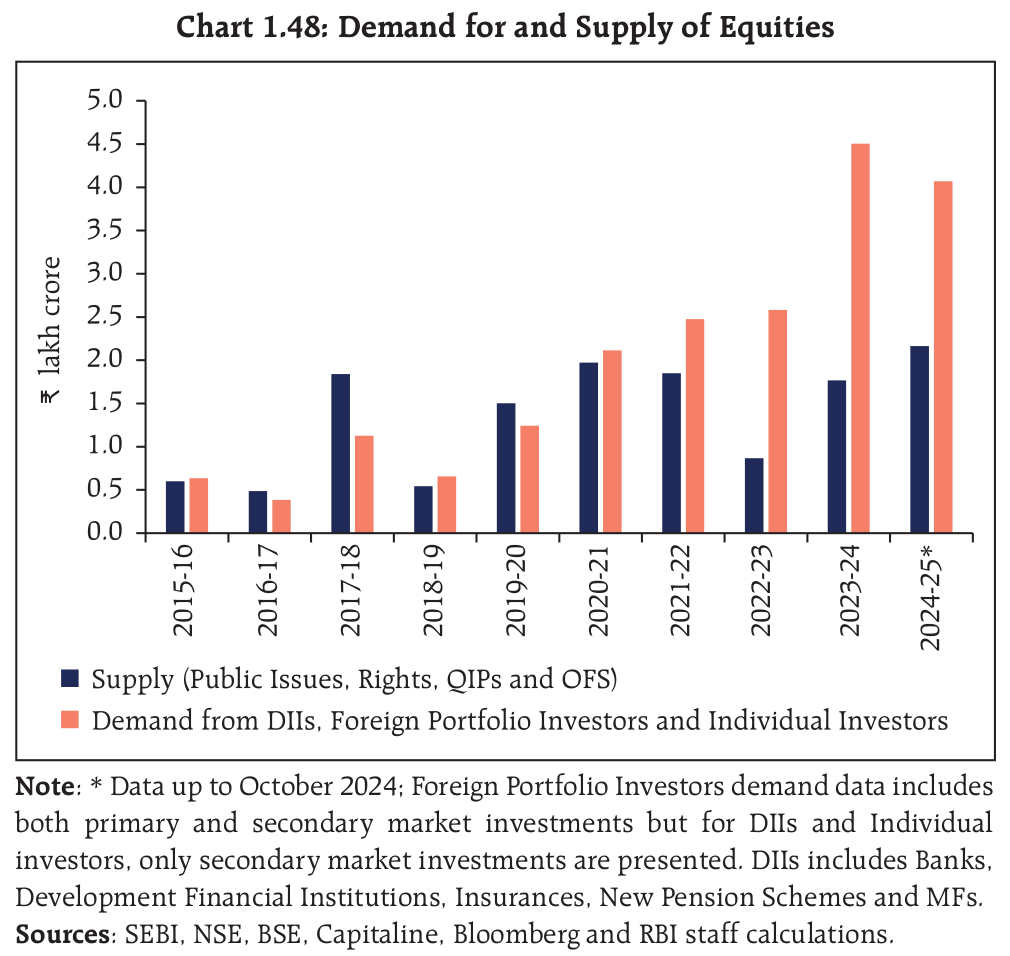

One reason for this disconnect is the strong domestic demand for equities, which has outpaced the supply of new shares from IPOs, FPOs, QIPs, and OFS since the pandemic.

Source: RBI

SEBI Whole Time Member Shri Ananth Narayan G has addressed this issue, saying, “Prolonged mismatches of this nature can leave us with more of asset price inflation, rather than capital formation.”

Dicey Banking System

This is where some serious risks are starting to emerge. While the banking system looks healthy overall, three banks—representing about 15% of total assets—are showing vulnerabilities across several risk indicators. A year ago, this number was much higher, so there’s been improvement, but it’s still a concern.

The way banks are handling deposits is changing fast, and this shift is important to understand. There’s been a move from low-cost CASA deposits to term deposits, particularly those with higher interest rates. In fact, term deposits accounted for 82% of the new deposits raised in the first half of 2024–25. Banks are also increasingly relying on higher-cost certificates of deposit to cover funding gaps.

To put it in perspective: since March 2022, banks’ cost of funds has gone up by 148 basis points. This is squeezing their net interest margins, which are shrinking across all types of banks. Yet, surprisingly, both return on equity and return on assets improved in September 2024.

Now, here’s where the bigger risks start to show—asset quality. At first glance, the numbers look great. The overall gross NPA ratio is at a 12-year low of 2.6%. But a closer look reveals worrying trends, especially in retail loans.

Let’s break it down. The gross NPA ratio for retail loans is 1.2%, which seems stable. But the concerning part is that 51.9% of new NPAs in retail loans are coming from unsecured loans like personal loans and credit cards. What’s worse is the sharp rise in write-offs by private banks, which could be hiding the true extent of the problem.

Stress indicators are flashing warnings. Special Mention Account (SMA) loans—those overdue but not yet NPAs—are rising, especially for large borrowers. Public sector banks, in particular, have seen a notable jump in their SMA-2 loans for this group.

For context, SMA-1 loans are overdue by up to 30 days, while SMA-2 loans are overdue by up to 60 days. These are early warning signs of loans at risk of turning into NPAs.

What’s keeping risk managers up at night is the growing overlap between borrowers. Nearly half of those taking credit cards and personal loans already have another loan, often a big one like a housing or vehicle loan. If they default on their personal loan, it could trigger defaults on these larger loans too, creating a domino effect.

The regulatory measures introduced in November 2023, like raising risk weights on consumer credit, have helped slow growth in retail loans and lending to NBFCs. Growth in these areas has dropped from 26.9% and 28.7% to 13.0% and 6.4%, respectively. But the big question remains—will this slowdown be enough to prevent systemic risks? The answer is still unclear.

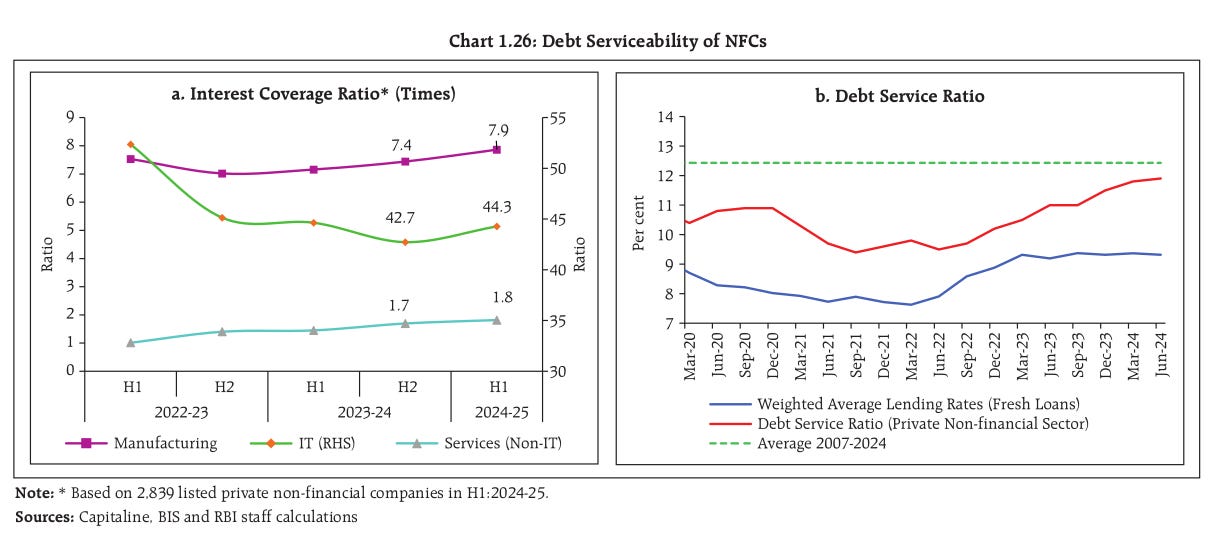

Corporate India

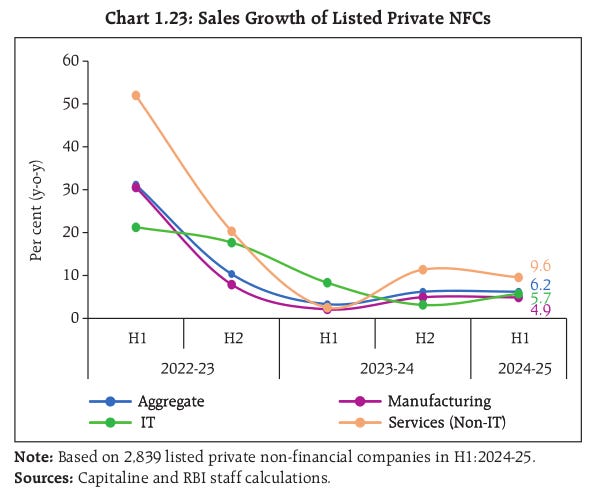

The headline numbers look good: sales went up by 6.2% in the first half of this fiscal year. But if you take a closer look, some interesting trends start to show. Operating profits for manufacturing companies dropped to 4.3%, mainly because of higher staff salaries and rising input costs. On the other hand, IT services grew by 5.7%, and non-IT services saw an even bigger jump of 9.6%.

Source: RBI

One thing that really stands out is the cost of borrowing, which hit an average of 9.2% in September 2024. Even with these higher borrowing costs, many companies are handling their debt well. Debt-service ratios are below historical averages, and the debt-to-equity ratio has been steadily improving since 2018.

Source: RBI

When you compare India’s corporate debt-to-GDP ratio to other emerging markets, India looks to be in a fairly solid spot. That said, even a small misstep can cause problems, so staying cautious is essential.

With all these risks in mind, the truth probably lies somewhere in the middle. It’s not all sunshine, but it’s not all doom and gloom either. We’ve done our part by giving you a report card for India—highlighting both the wins and the challenges.

Now, it’s your turn: what do you think 2025 holds for India? Will the nation continue its upward climb, or will these risks slow down the progress? One thing’s certain: the road ahead is bound to be full of surprises.

Green Steel: India’s Game Plan for Sustainable Growth

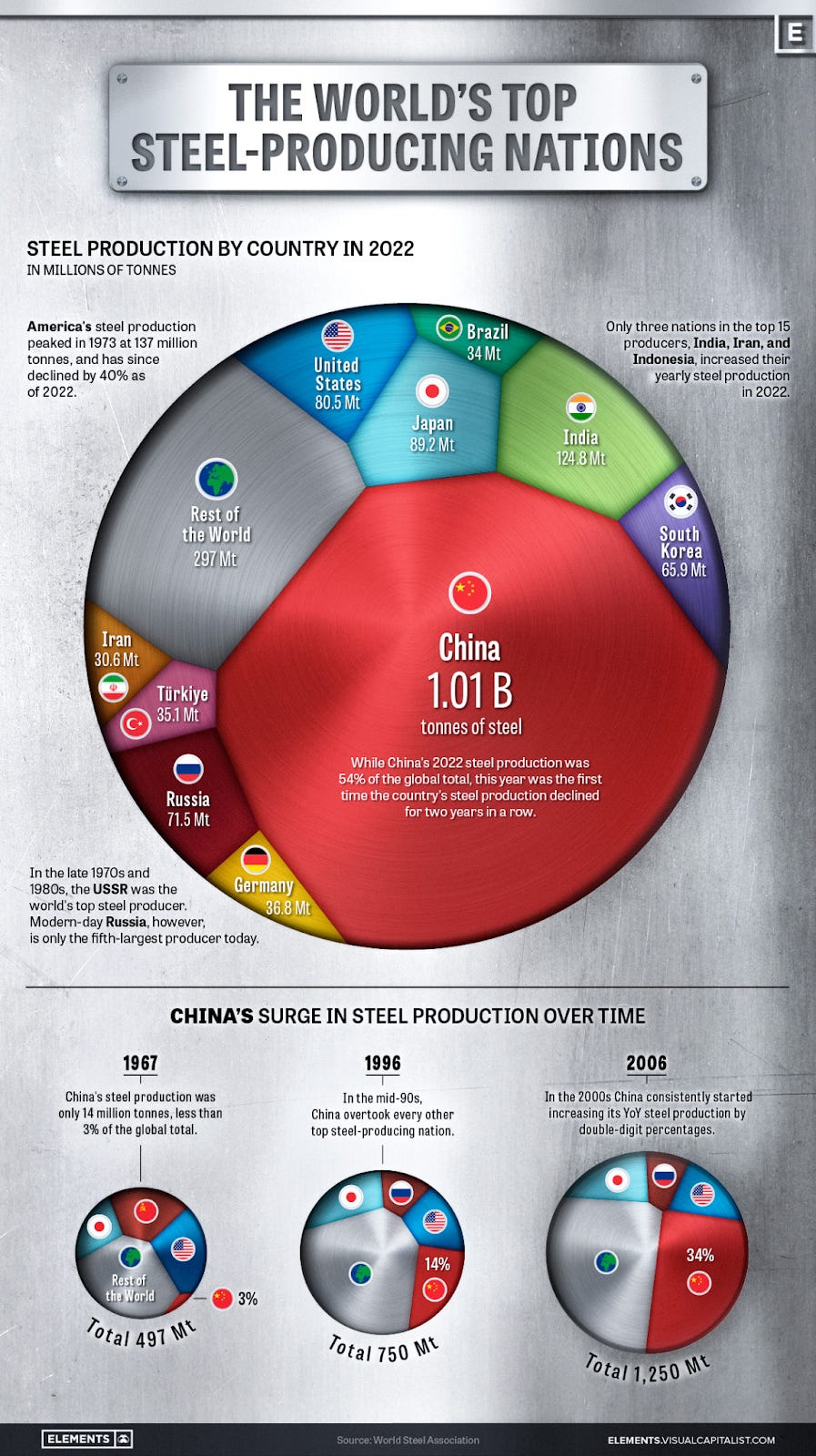

The Indian government is rolling out a ₹15,000 crore Green Steel Mission to transform the steel industry into a low-emission powerhouse. As the world’s second-largest steel producer, India is taking a big step to decarbonize one of its most polluting sectors.

Source: Visual Capitalist

This mission focuses on integrating renewable energy and green hydrogen into steel production, requiring government purchases of green steel, and promoting innovation. Alongside this, the Production-Linked Incentive (PLI) scheme for specialty steel is already in motion, drawing over ₹27,000 crore in investments so far.

But why is the government doing this?

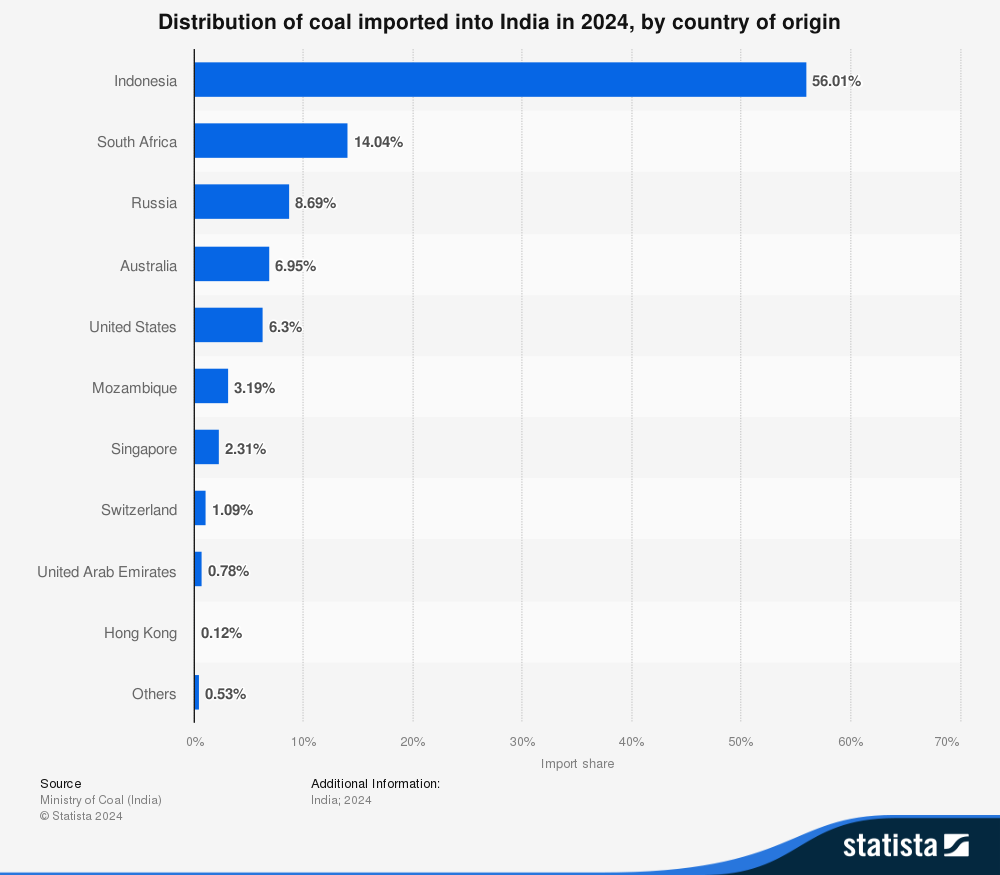

To understand the importance of this move, we need to zoom out and look at the bigger picture. Steel production is responsible for 10–12% of India’s total greenhouse gas emissions, making it one of the largest industrial contributors to climate change. The traditional way of making steel depends heavily on coking coal—a high-carbon fuel that powers blast furnaces. India relies so much on coking coal that it imports a significant portion, mostly from Australia, even though it has domestic iron ore reserves.

Source: Statista

With India’s steel production expected to rise to meet the needs of a growing economy, emissions from the sector could increase even more unless there’s a shift to cleaner methods. The Green Steel Mission aims to tackle this by promoting technologies like hydrogen-based steelmaking and renewable energy.

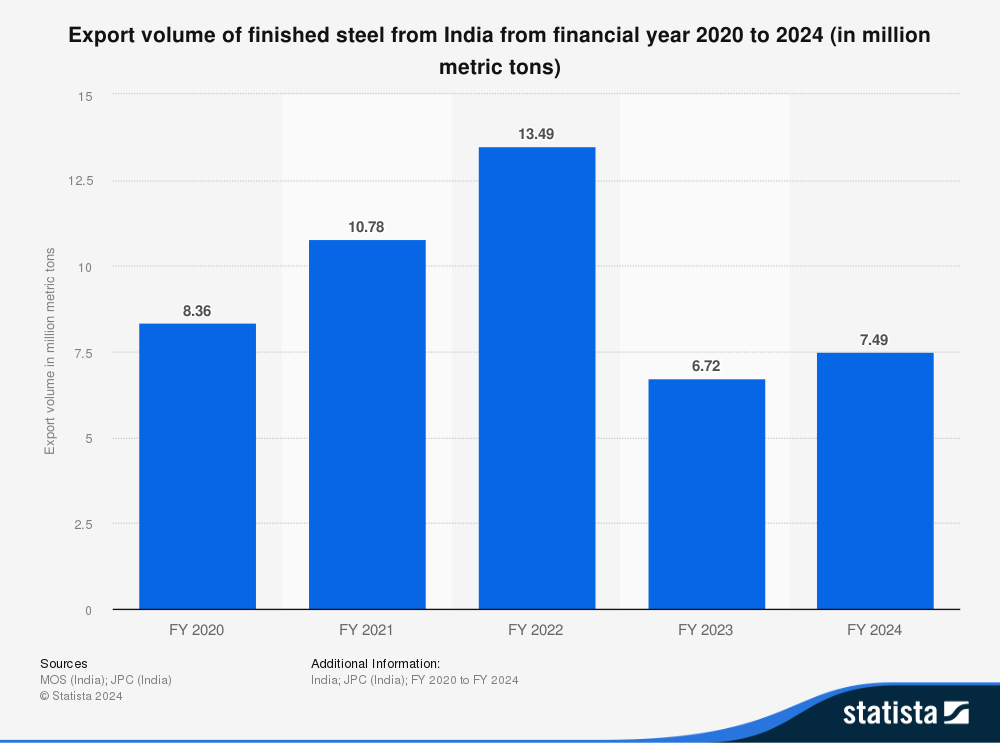

This initiative didn’t come out of nowhere—it’s driven by both challenges and opportunities. One major factor is the European Union’s Carbon Border Adjustment Mechanism (CBAM). This policy adds tariffs on imports based on their carbon footprint, effectively penalizing industries like steel that produce high emissions. Indian steelmakers, who exported around 6 million tonnes of steel to the EU in FY23, now risk losing market access or facing steep penalties unless they adopt low-carbon production methods. This international pressure is a key reason why the government is pushing for green steel now.

Source: Statista

The EU’s Carbon Border Adjustment Mechanism (CBAM), set to take full effect by 2026, poses a serious challenge for Indian steelmakers. Without green steel, companies risk facing heavy financial penalties, which could make their exports too expensive for the EU market—one of their most profitable destinations.

India has committed to achieving net-zero emissions by 2070, a goal announced at COP26. Reaching this target will require major decarbonization in industries like steel, which are among the largest emitters.

The Green Steel Mission will come with high costs for Indian steelmakers, especially smaller producers who might struggle to afford the expensive upgrades or new plants needed to meet the standards. However, it also opens up opportunities for larger players like Tata Steel and JSW Steel. These companies could gain a competitive advantage in export markets such as the EU and tap into growing domestic demand fueled by government mandates for green steel procurement.

By reducing reliance on imported coking coal, the mission also encourages the use of green hydrogen and renewable energy, driving demand for cleaner technologies. Companies that fail to adapt may find themselves losing market share as sustainability becomes a key priority worldwide.

Tidbits

-

NPCI extended the 30% UPI cap deadline to December 2026 and removed WhatsApp Pay’s user cap, enabling it to serve 500 million users. This comes as UPI transactions surged 32% in 2024, with PhonePe and Google Pay dominating market shares.

-

Authum and Mahi Madhusudan Kela acquired a 72.8% stake in Prataap Snacks, maker of Yellow Diamond, through strategic deals. Competing in a fragmented snack market, this move boosts Prataap’s market position and highlights consolidation in affordable FMCG.

-

Blinkit introduced a fleet for bulkier orders and EMI options for purchases above ₹2,999, aiming to boost demand for high-ticket items and expand its consumer base.

-This edition of the newsletter was written by Kashish and Krishna

Thank you for reading. Do share this with your friends and make them as smart as you are ![]() Join the discussion on today’s edition here.

Join the discussion on today’s edition here.