Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Why are tariffs such a big deal?

- Energy all over the world

Why are tariffs such a big deal?

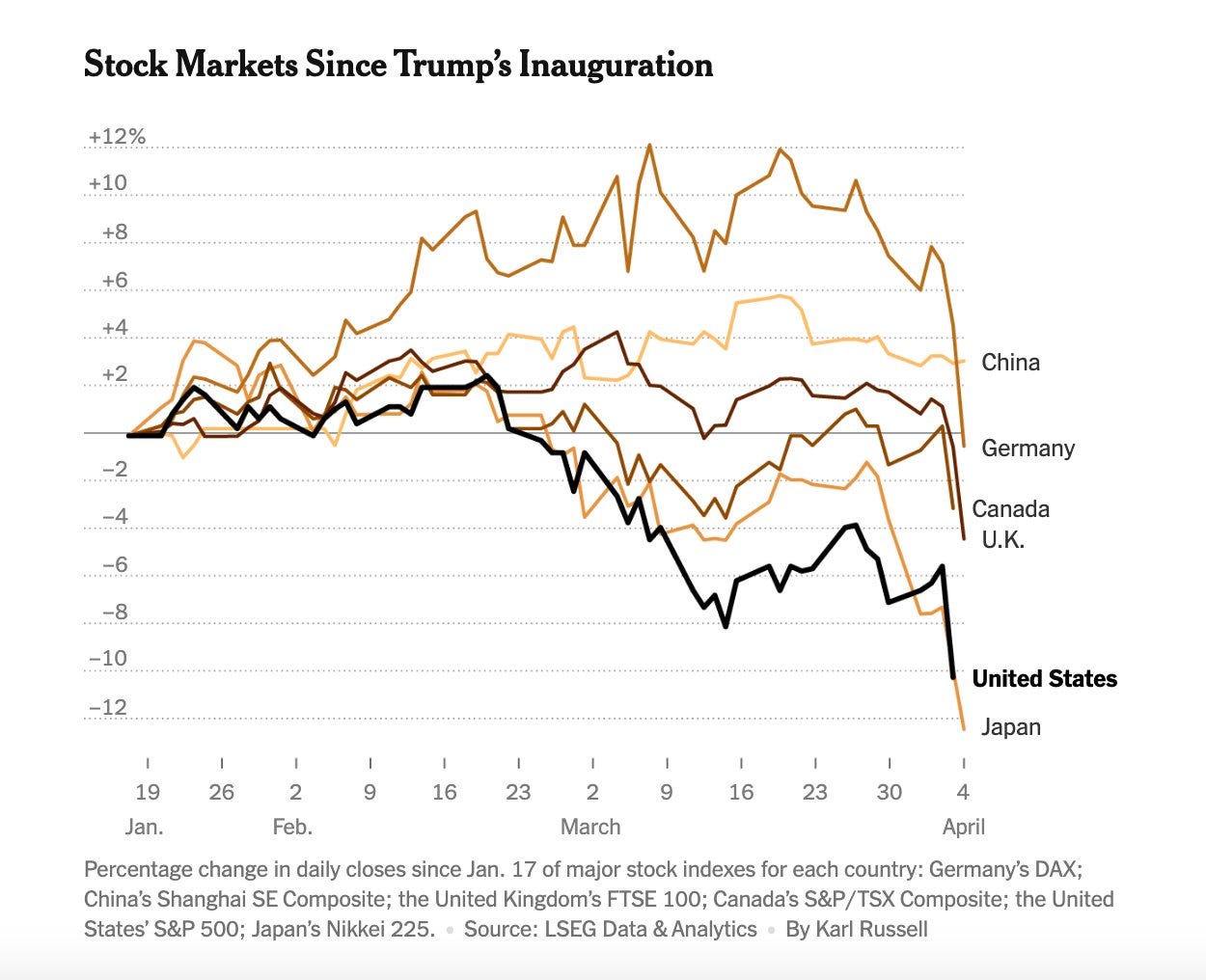

So you’ve seen the world lose their collective minds over the Trump tariffs. Everyone seems to consider this the financial apocalypse. The stock markets are deep in the red, and a range of businesses are making cryptic statements about how they need to “restructure their supply chains.”

Through all this, there’s a good chance that you don’t actually know why this is such a big deal. You’ve probably heard all the basic explainers already — about how tariffs are essentially import taxes — without a real sense of why a few tax hikes can cause the world to lose its collective mind.

We get it. This isn’t something you’re expected to know. People don’t spend their days thinking about supply chains. It’s really easy to underestimate how critical global value chains are, how widely they spread, or how fragile they can be in the face of a crisis. But make no mistake, they’re the basis of the plentiful lives we live. They’re the reason you even have the device you’re reading this on, even.

To help you understand why, though, we’ll need to take you into the mundane, boring exchanges at the heart of the global economy. If you stick with us, though, we promise you’ll learn a little more about why it’s so tragic that these are all suddenly in jeopardy.

Global supply chains are a miracle of mankind

Modern commerce exists because of global value chains.

Most modern industrial products are like giant lego installations. They’re made by putting together a huge array of pieces, most of which are made by other people. As the economist Leonard Reed noted almost seventy years ago, there isn’t a single person alive who knows how to make a single lead pencil from scratch. Pencil-making is a collaborative exercise between millions of people. Some of them chop the wood, some of them dig for clay, some of them mine raw graphite, and so on. None of these people can see more than the smallest sliver of the complete supply chain. And yet, by coming together, they make millions of pencils every day.

What’s true of pencils is a million times as true for the more advanced products we take for granted: from car batteries to mobile phones.

There are places in the world that have world-beating expertise in making single, specific parts of those giant lego installations. Their products, by themselves, could seem mundane. For instance, you may run an entire business around making one very specific spring, which only goes into making the accelerometers that are used in iPhones.

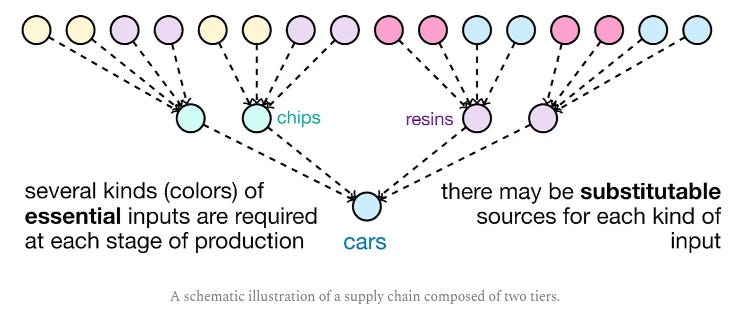

We aren’t exaggerating at all, by the way. Consider this: Toyota, for instance, sources 400,000 different products to make its cars. Boeing sources 6 million different components for its airplanes. Anything they do depends on layers and layers of suppliers. If this is hard to wrap your head around, here’s an illustration of a simple supply chain. This should tell you how quickly the number of suppliers can multiply:

This extreme specificity brings huge advantages. You can spend all your time and energy thinking of how to perfect one specific spring, making it more cheaply and efficiently than anyone else. Different suppliers do the same thing for their own components. Because of all the effort of all those suppliers, taken together, making extremely complicated products becomes cheaper and quicker as a whole . That is why you can get an entire phone — a computer, communications device, camera, music system, and a dozen other things rolled into one — for just a few thousand Rupees.

But here’s the catch: this only works because of the incredible scale at which these value chains operate. Making accelerometer springs for phones sold in Southern Karnataka, where we live, isn’t really a viable business idea. But if you can do so for a big chunk of every phone sold in the world, suddenly, you have a million-dollar business plan. When you hear headlines about India trying to ‘establish itself as part of global value chains ’, this is what they’re talking about — creating excellent, hyper-specialised businesses that can become small parts of mammoth supply chains.

This is why the scale and efficiency of global supply chains are two sides of the same coin. Neither makes sense without the other.

These supply chains are incredibly fragile

When you zoom into any part of one of those global supply chains, you’ll realise how incredibly fragile they are. If any one node of a supply chain goes under, that hurts everyone that it supplies products to. Which, in turn, hurts the next entity in the chain. And so on.

The results can be dramatic . If one supplier in a smartphone supply chain faces problems sourcing a single 5 cent capacitor, for instance, that could block entire shipments of $1000 phones.

We saw hints of this in the COVID-19 pandemic.

When people across the world began working from home, there was a huge surge in the demand for computers all over the world. Chip manufacturers started routing their production to this segment, while car manufacturers temporarily stopped placing orders for them. A few months later, though, when they resumed production, there were no chips available .

Now, chips aren’t too big a part of cars: they run things like power steerings, sensors and infotainment systems. They’re no more than 5-10% of a car’s cost. But you can’t make cars without chips. And so, as chips became hard to come by, global automobile production slumped by 26%. The price of cars swung wildly for years, only easing late last year.

This is why simple intuitions don’t work if you’re thinking about world trade. Supply chains are complex and inter-connected. Tiny disruptions quickly cascade into huge problems. Just as work-from-home policies made cars unaffordable for years, when something as huge as world-wide tariffs comes into play, you should expect chaos to ensue.

America, as the world’s largest consumer market, is where the final products in many of the world’s value chains land up. Trump is trying to leverage that market. The case for Trump’s tariffs is that a lot of businesses will move their manufacturing operations to the United States lock-stock-and-barrel, creating millions of new jobs. On a surface level, this might even make sense to you.

But once you understand how global business actually works, it no longer makes sense. You can’t just force “Apple” or “Nike” to move to America. Those plans only work if their entire ecosystems move with them.

The truth is that we aren’t talking about single businesses at all — we’re talking about huge chains of businesses, stretching across thousands of entities, criss-crossing through dozens of countries. There are entire cities in parts of Asia (like Zhengzhou — China’s ‘iPhone city’) full of businesses that make different parts of a single product. For these tariffs to succeed, the United States would have to find replacements for every single one of those businesses, for every single product it imports. The existing supply chains were put together over decades of investments. Shifting them all is impossibly complicated to pull off, and even in a best case scenario, will take years.

What happens before that? Higher prices. Supply shortages. Industries going bankrupt. And all sorts of other problems.

The research is unequivocal about this. Modern supply chains were only possible because tariff rates across the world were lower than they had ever been. As tariff rates rise again, all those supply chains will probably break.

But things can get even worse: the problem doesn’t just have to do with the products that America imports. All-American manufacturers, too, are plugged into global supply chains. Suddenly, they have to pay much larger bills for everything they import. Companies have been rushing to import as much as they can before the tariffs kick in — but that isn’t a long term solution.

So, on the one hand, Trump might find it hard to bring other manufacturers into America. On the other hand, it might push America’s existing manufacturers into a crisis. This is why these tariffs are inflationary by design . That is why everyone has been losing their minds.

What do we really mean

Chances are, you still don’t get it. Unless you really come to see how complex supply chains are, this is all horribly unintuitive. So here’s just one example, to give you a sense of how these supply chains actually work — by showing you the insides of just one of them.

In 2023, the United States manufactured ~10.6 million cars. But here’s a secret: the United States doesn’t actually have an automobile industry . North America does. Consider this: most cars are made of ~30,000-40,000 parts. More than ~18,000 suppliers are involved in making a single car. These suppliers are scattered all across Canada, Mexico and the United States.

A whole car is an impossibly complex machine, so let’s just zoom into a single part of a car: its dashboard . Nobody makes entire dashboards. A car dashboard is a huge collection of various materials and technologies. A typical one has 21 parts, with 44 possible variations. Here’s a simplified, hypothetical example of how it might come together:

A dashboard has a structural frame, on which everything else is laid. That frame is made of steel or aluminum. This might be procured from suppliers in Canada. Metal sheets (which have their own supply chain) will be transported from Canada to a stamping facility in Mexico, and moulded into the required shapes.

A different supplier, meanwhile, will put together the electronic modules for the dashboard. They’ll buy a series of different units from their own suppliers — such as screens, circuit boards, sensors, climate control units etc. Many of these components will be sourced all the way from South Korea, with chips coming from Taiwan. A plant in the United States might put these all together. Meanwhile, our very own Tata Technologies might write some of the software that makes it all work.

You’ll also require wiring harnesses to connect all those electronics. These might be put together by a separate Mexican manufacturer, from supplies they’re getting from the United States and Chile.

All of this will be dressed in a plastic shell, and will be fitted with buttons and control knobs. Those parts might be manufactured by different moulding facilities in Canada, all of whom will use specialty polymers they import from companies in the United States. Once moulded, those plastic parts may then be sent to Mexico for painting and coating. If they require particularly refined work for a more premium finish, such as laser etching, they might even be shipped to dedicated suppliers in Asia.

Once all these parts have been put together, they’ll all go to an ‘OEM’ that runs an assembly plant in the United States. They will, in turn, assemble the components together into a dashboard, make sure everything works, and send it onwards to the car company.

At the end of this long, multi-national process, you’ll end up with just a dashboard — just one of the hundreds of parts of a car — and not even the main part, by far. A similar process will be repeated for every single other component. In fact, single components can traverse America’s borders with the United States and Mexico as much as eight times.

Now imagine: suddenly, every time any component moves across borders, it gets slapped by a 25% tax. Think of how prices would balloon at every step. Even if companies want to avoid this, they’ll have to go through a profound period of instability, as they comb through their supply chains and reshore their sourcing to the United States. This will take time, and in the meanwhile, they’ll bleed money.

Of babies and bathwater

And that’s why everyone’s losing their marbles.

Trump may be right in some limited sense — of how America has de-industrialised. In response, however, he has committed one of the most profound acts of throwing the baby out with the bathwater in recent history.

The new tariffs don’t just “hurt trade.” They upend a system built over decades — one where efficiency didn’t come from a single country being great at everything, but from many businesses across a variety of countries being world-class at one thing. The plenty we see around us all comes from the long chains these businesses formed — as though they were running a long industrial relay race. The tariffs disrupt relationships between those thousands of companies that, until now, worked together like pieces in a gigantic, invisible machine.

They’ve introduced uncertainty where there was precision, and friction where there was once flow. We don’t know what comes after this. As all the disruption during COVID showed us, economies don’t work in linear, intuitive ways. When one part of the economy breaks, it can throw seemingly unrelated parts of the economy into complete chaos.

That’s why tariffs trigger panic. Not because they’re conceptually scary, but because they casually threaten a system so vast and interdependent that even small shocks can cascade. Because nobody — not businesses, not economists, not even the governments imposing them — can fully predict what happens when you start messing with supply chains this intricate.

Energy all over the world

We’ve previously talked about the World Energy Outlook from the International Energy Agency (IEA). While that was about energy more broadly, today, we’re going into a specific, but crucial, part of the energy story: electricity . We’re looking through the Global Electricity Review 2025 by Ember Energy.

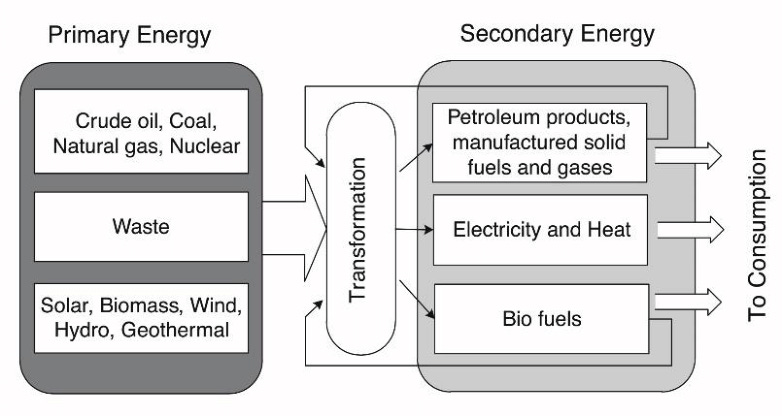

First, though, you should know why energy and electricity are different .

“Energy” is an umbrella term. It’s the ability to do stuff — move cars, heat homes, run factories. It can come from coal, oil, sunlight, wind, or even uranium. These are all primary sources of energy .

Electricity, on the other hand, isn’t a primary source—it’s what we call a secondary source . It’s how we often use energy. We don’t grab electricity straight from nature. Instead, we convert other energy forms, like solar or coal, into electricity, and turn it into electricity for further use.

Take solar energy, for instance. It’s not like you can run your TV directly on sunlight! You must first convert that sunlight into electricity. Similarly, coal can be burned directly, say, in industrial furnaces, but we mostly burn coal in power plants to create electricity. In fact, coal is responsible for about 75% of India’s electricity generation.

This context will come handy later on in the story.

The latest Global Electricity Review talks about everything under the sun about electricity. We’ll first talk about the demand side of the equation—where it’s coming from, which countries are driving it, and a few key trends (both structural and temporal). Then we’ll shift to the supply side —talking about the electricity mix, the scope of growth for renewables, and what not.

Also, on a side note — this story is part of the deeper and more nuanced research we’re doing for an upcoming episode of “The Long Answer”. More on that later.

Well, the demand is demanding

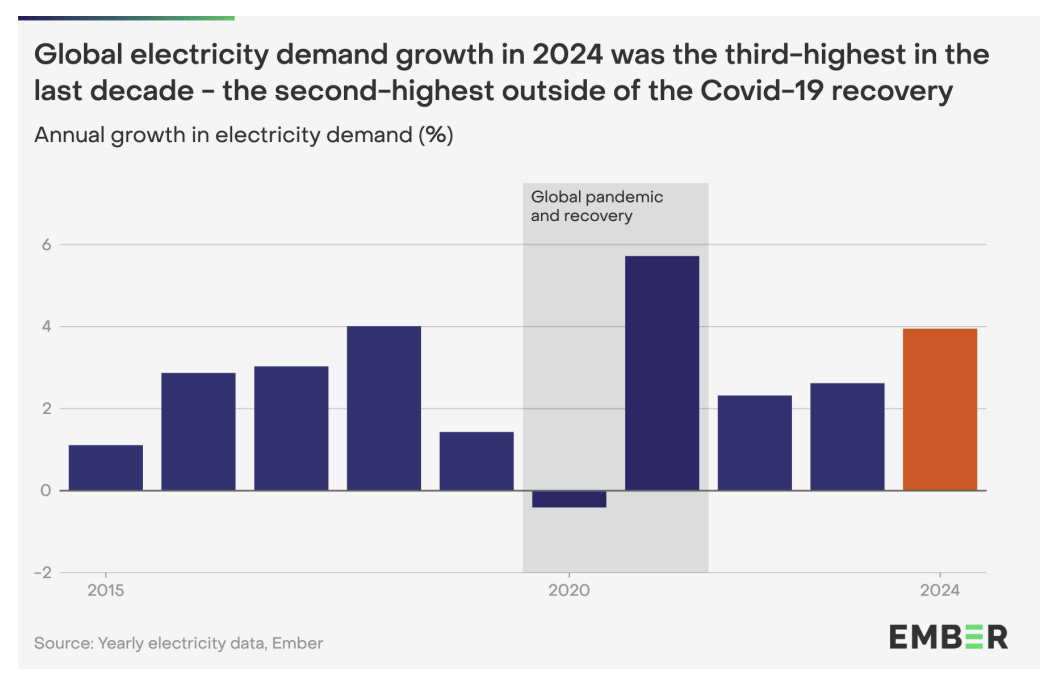

Electricity demand went wild in 2024—jumping up by 4%. That might not sound huge, but get his: it’s actually the third-highest annual increase ever recorded.

China led this charge, with a 6.6% increase in electricity demand — accounting for more than half the global growth. India’s electricity appetite grew by 5% as well, thanks to rapid electrification and rising living standards. Even the US chipped in with 3% growth.

What does this mean? Are people consuming more and spending more, while industries work harder? Well… there’s some truth to that. But there’s more going on here.

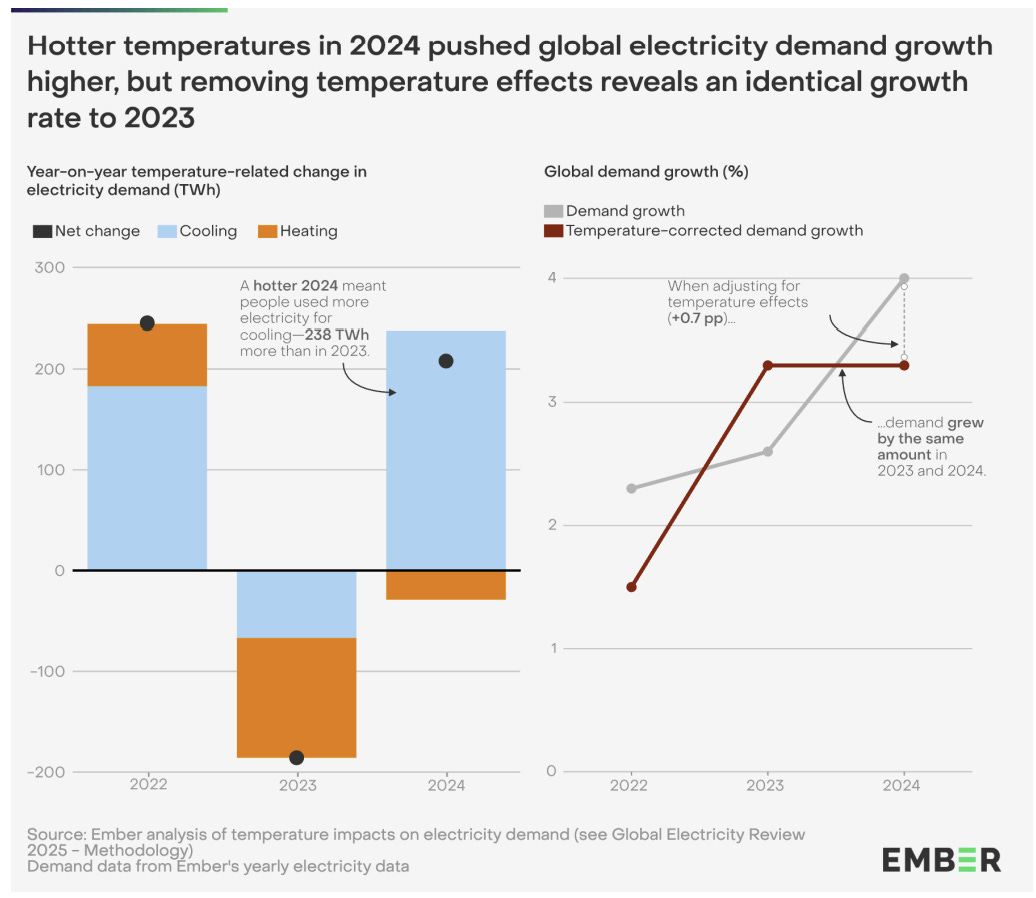

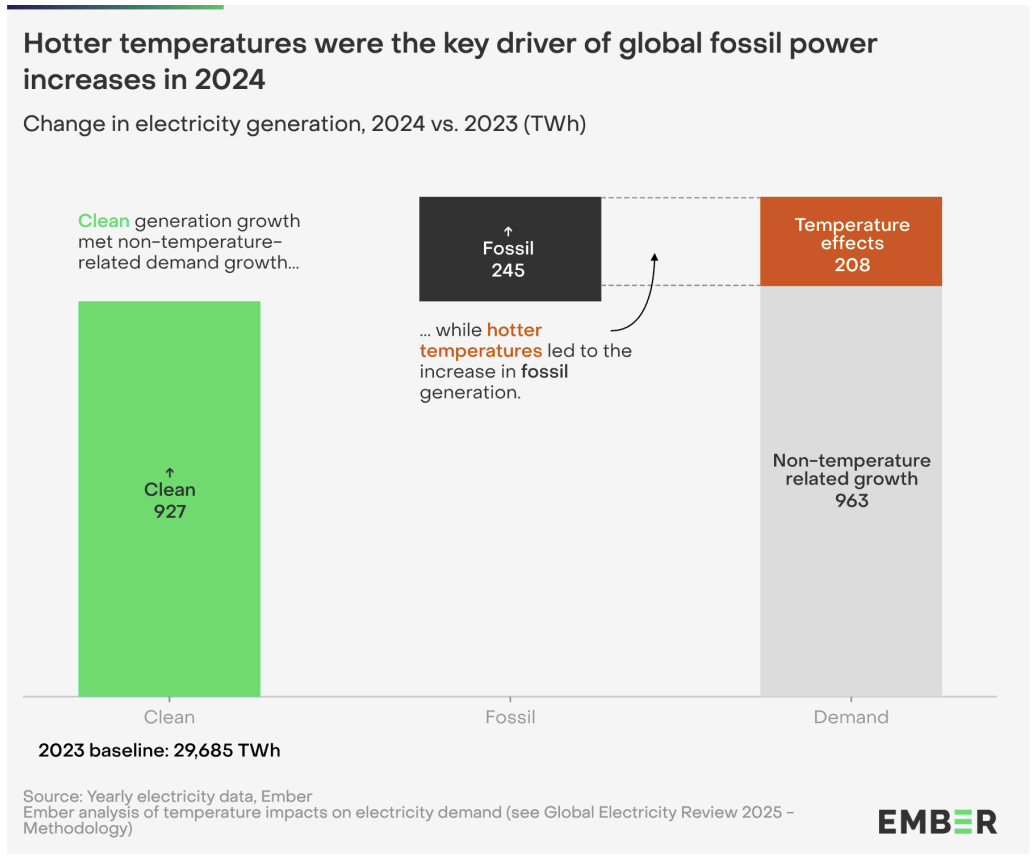

One, last year was hot . Like, record-breaking hot. Heatwaves alone were responsible for almost one-fifth of the total rise in global electricity demand last year. Air conditioners, it turns out, can push up the electricity bills of entire countries. If we remove these temperature effects, the growth in electricity demand in 2024 was actually similar to the previous year.

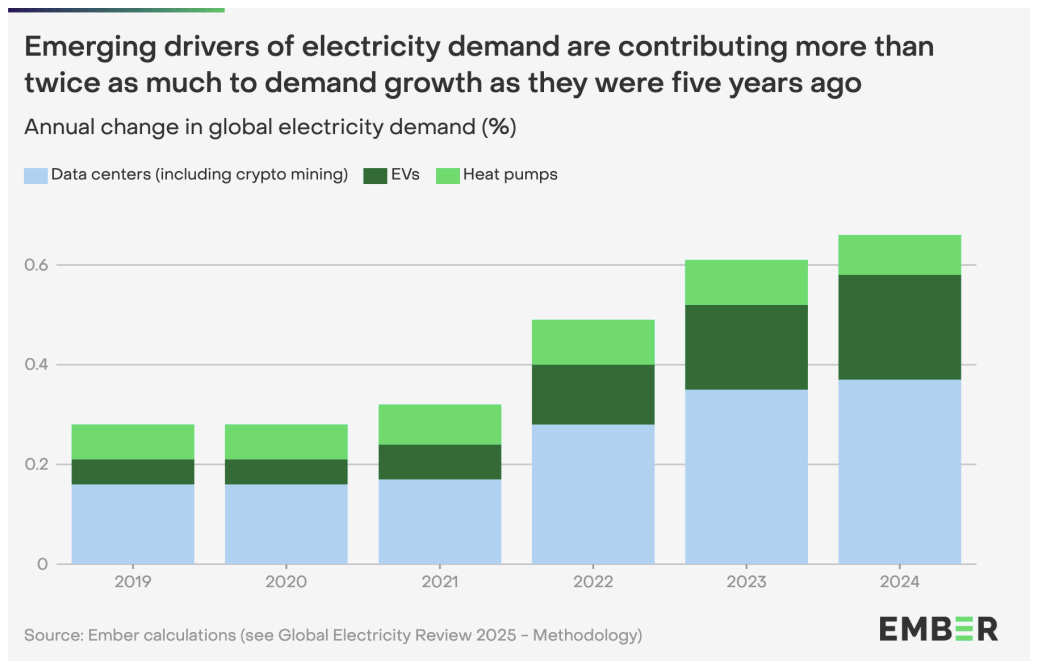

But it’s not just heatwaves that pushed electricity demand up — there are also some permanent changes afoot that are causing a structural shift. A lot of it has to do with electrification and AI .

As we mentioned earlier, electricity is one type of energy. We also use energy in transportation, in the form of crude derivatives like petrol or diesel. But that’s changing. With electric vehicles, we’re seeing a shift — the demand for crude could go down as the transportation system gets electrified. Same with heat pumps. We’ve used diesel pumps to pump water for decades. But now, they’re getting electrified too.

And then comes AI. You need a lot of energy to store and process data to run all those huge LLMs. And let’s not forget crypto mining. These are two brand-new sources of demand for electricity that didn’t even exist until recently — and they probably won’t go away anytime soon.

These factors alone bumped global demand up by 0.7% in 2024—double their impact just five years ago.

How is the Supply keeping up?

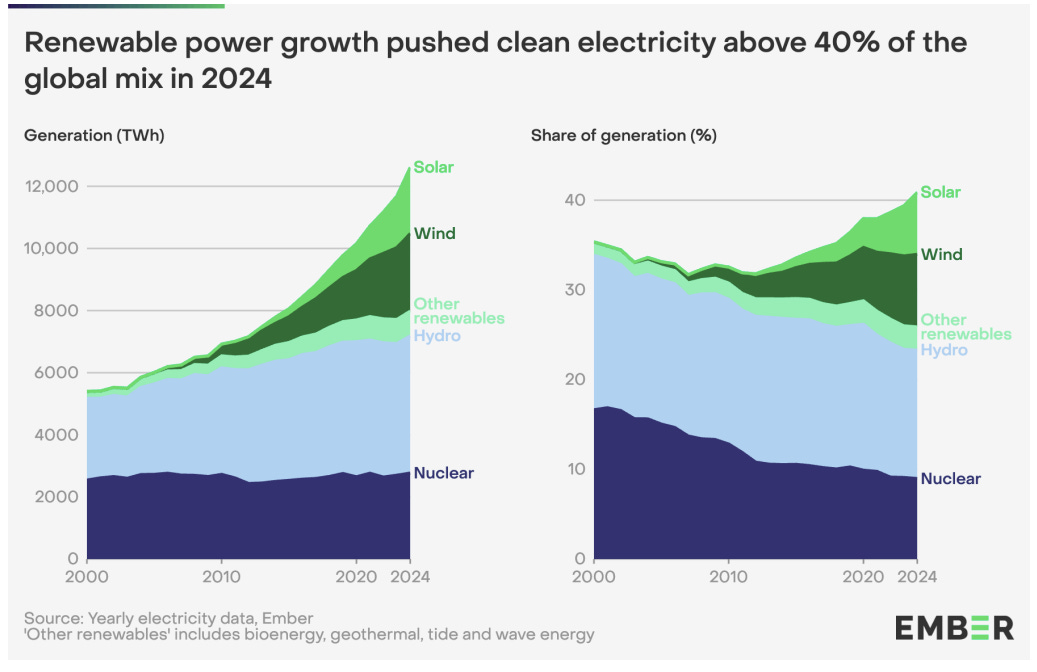

For the longest time, we leaned heavily on carbon-heavy sources like coal for our electricity needs. But here’s the good news: renewable energy is absolutely booming .

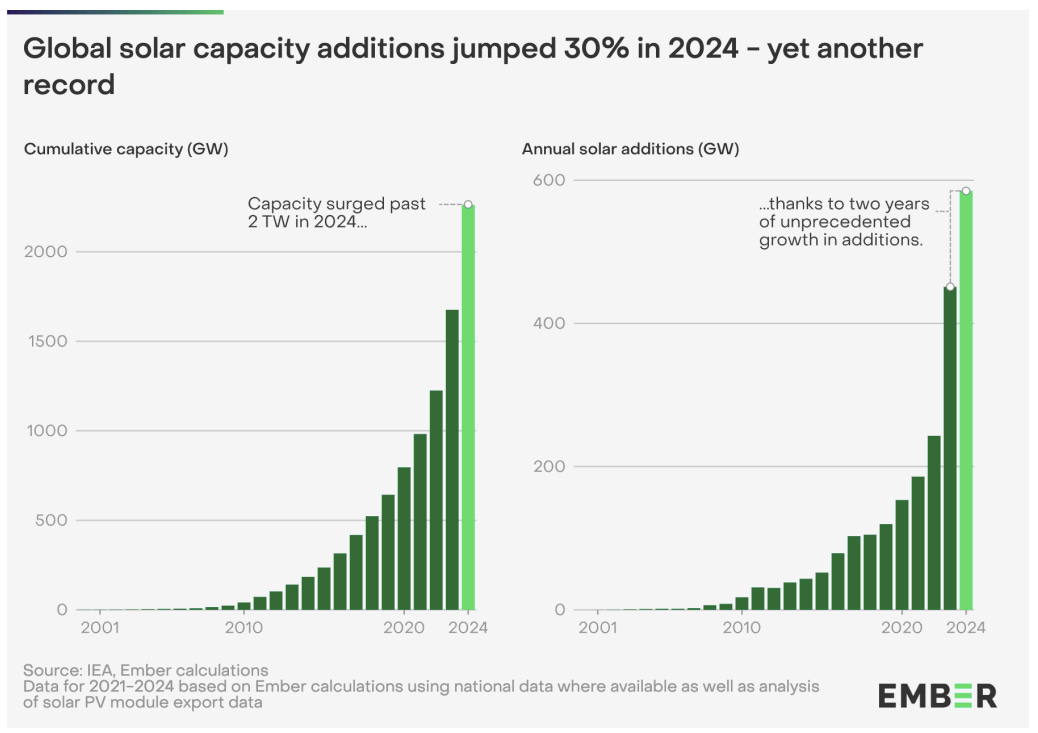

In 2024, for the first time since the 1940s, clean electricity (read: non-carbon sources like solar, wind, hydro, and nuclear) made up more than 40% of global electricity generation. Renewables alone added a record-breaking 858 TWh, smashing the previous high by almost 50%.

And the star of the show? Solar energy (yes, pun intended ![]() ). Solar has doubled globally in just the last three years, and has been the fastest-growing electricity source for 20 years straight. In 2024 alone, it grew by 29%. Fun fact: the world’s now generating enough solar electricity to power all of India.

). Solar has doubled globally in just the last three years, and has been the fastest-growing electricity source for 20 years straight. In 2024 alone, it grew by 29%. Fun fact: the world’s now generating enough solar electricity to power all of India.

This explosion in generation has been powered by insane growth in capacity. The world installed a record 585 gigawatts (GW) of solar capacity last year—30% more than in 2023, and more than double what was added in 2022. For context, we hit 1 terawatt (TW) of global solar capacity in 2022… and then doubled that in just two years. No other power source in history has ever grown this fast.

(A note of caution, though: we rarely make as much solar electricity as the capacity alone indicates. We’ll touch on this some other day.)

One thing that stood out for us was that solar is now so cheap that large markets can emerge in the space of a single year.

Just look at Pakistan. Yes, Pakistan . Amid sky-high electricity prices thanks to expensive thermal power contracts, rooftop solar took off. In 2024, Pakistan imported 17 GW of solar panels — double the amount from the year before — suddenly making it one of the world’s fastest-growing solar markets.

Of course, even with all these solar panels popping up, fossil fuels are still hanging around. Why? Mostly to meet the extra demand from the kind of extreme heat we saw in 2024. In countries hit hardest by heatwaves—coal stepped in to pick up the slack in China and India, while gas generation rose in the US. But if we could keep that aside — if 2024 had the same temperature pattern as 2023, fossil generation would’ve barely budged—up just 0.2%.

Global warming begets global warming.

That said, coal, hydro, and wind still remain big players in the global electricity game.

- Coal still supplies about 34.4% of global electricity. It’s not pretty, but it’s still widely used — especially in countries like China and India — especially when demand spikes.

- Hydropower is the OG clean energy source, contributing 14.3% of the global mix. But its output depends a lot on rainfall. With climate patterns becoming less predictable, so is hydro’s reliability.

- Wind accounts for 8.1% of global electricity. It’s still growing, but a little slower in 2024 because of weaker winds in parts of China and Europe.

Together, these sources show just how diverse—and weather-dependent—our electricity mix still is.

Future Outlook: Clean Power is Winning

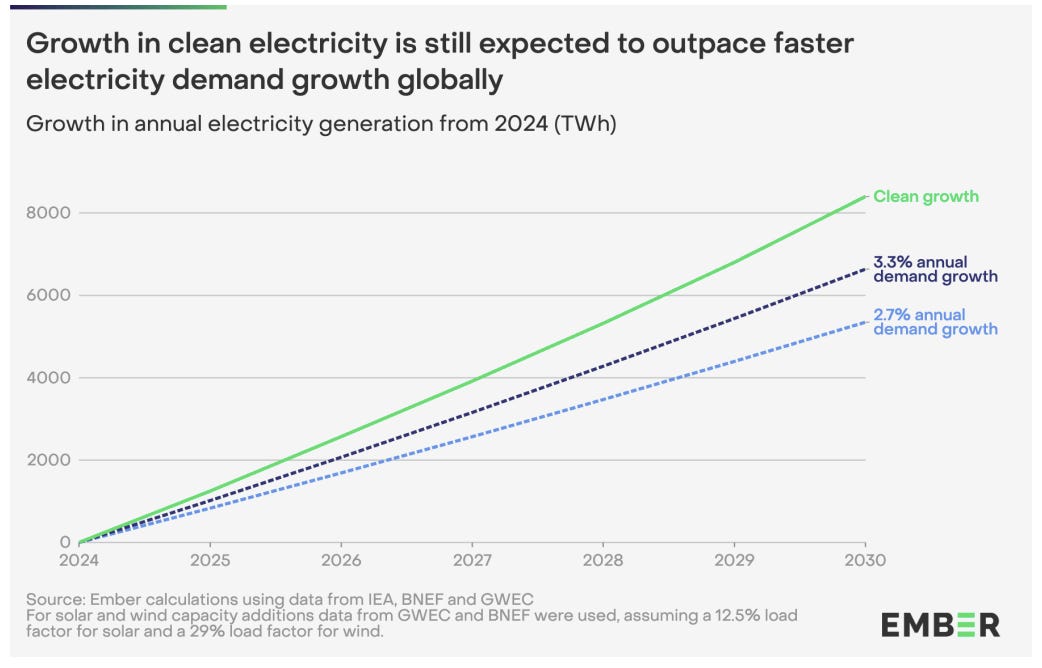

Going ahead, the momentum seems to lie with clean electricity. Even with global demand rising, renewables and clean tech are set to outpace fossil fuels by 2030. Major players like China and India are going all-in on solar and wind. And as we make progress with energy storage solutions, the argument for fossil fuels gets weaker every year.

In fact, even if electricity demand keeps growing at a solid pace, our current rate of renewable installation is fast enough to meet it. That means the clean electricity share—already above 40% for the first time—should keep rising from here.

What does all this mean?

It means the way we power our homes, businesses, and data centers is changing—fast . Clean tech is now leading the charge on both economic growth and energy security. Sure, fossil fuels still sneak in when the weather acts up, but their days of dominance are clearly numbered.

As Phil MacDonald from Ember puts it:

“Cleantech, not fossil fuels, is now the driving force of economic development. The era of fossil growth is coming to an end. ”

Frankly, it’s about time.

Tidbits:

- After a gap of 34 months, the Centre has raised excise duty on both petrol and diesel by ₹2 per litre, effective April 8. This brings the Special Additional Excise Duty to ₹13 per litre on petrol and ₹10 on diesel. Despite the hike, retail prices will remain unchanged as oil marketing companies (OMCs) are expected to absorb the additional burden using existing inventories. In parallel, the price of domestic LPG cylinders has been increased by ₹50 for both PMUY beneficiaries and regular consumers.

- Shriram Finance Ltd., one of India’s largest shadow lenders, has approached the Reserve Bank of India for a primary dealership license, with plans to set up a separate entity for the purpose. The move comes as India’s sovereign bond market continues to expand, with the outstanding amount of federal government bonds reaching ₹112.5 lakh cr.($1.3 trillion) as of April 7, according to RBI data.

- Apple exported iPhones worth ₹1.5 lakh cr. from India in FY25, marking a 76% year-on-year jump and doubling its committed target of ₹74,900 crore under the government’s PLI scheme. The company accounted for 75% of India’s total smartphone exports, which crossed ₹2 lakh cr. in the last financial year. Monthly shipments averaged ₹12,500 crore, with March alone contributing ₹20,000 crore—Apple’s highest monthly figure—followed by ₹18,000 crore in January and ₹17,500 crore in February.

- This edition of the newsletter was written by Pranav and Kashish

Join our book club

Join our book club

We’ve recently started a book club where we meet each week in Bangalore to read and talk about books we find fascinating.

If you’d like to join us, we’d love to have you along! Join in here.

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()

")