Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Cement giants getting even bigger?

- Beer Price War in Telangana

- Reliance vs ONGC: The $1.7B Gas Dispute

Cement giants getting even bigger?

The cement sector’s third-quarter results are out. Today, we’ll look at two of India’s largest cement producers — UltraTech Cement and Adani Cement. Together, these giants account for roughly half of the country’s total cement capacity — with UltraTech touching around 170+ million tonnes per annum (MTPA), while Adani Cement approaches 90 MTPA.

Cement is an interesting sector. For one, it’s absolutely vital for the broader economy. It is the foundational substance for real estate, infrastructure, roads, and nearly every major construction project in the country. When we examine cement’s performance, we’re effectively taking the pulse of infrastructure spending, housing demand, and economic health.

Moreover, the combined dominance of these two companies illustrates the extent of consolidation in the Indian cement industry. This, as we’ll soon see, is a story that we’re still seeing play out.

UltraTech Cement

UltraTech Cement, part of the Aditya Birla Group, is India’s largest cement manufacturer. It’s also among the top five cement players globally (excluding China). The company has a massive footprint across all key markets — North, Central, West, and an expanding presence in the South.

Source: Tijori Finance

As of Q3 FY25, UltraTech’s total cement capacity stands at ~171 MTPA, following two major acquisitions that it completed recently — India Cements and Kesoram Cement. The company aims to cross 200 MTPA by FY27.

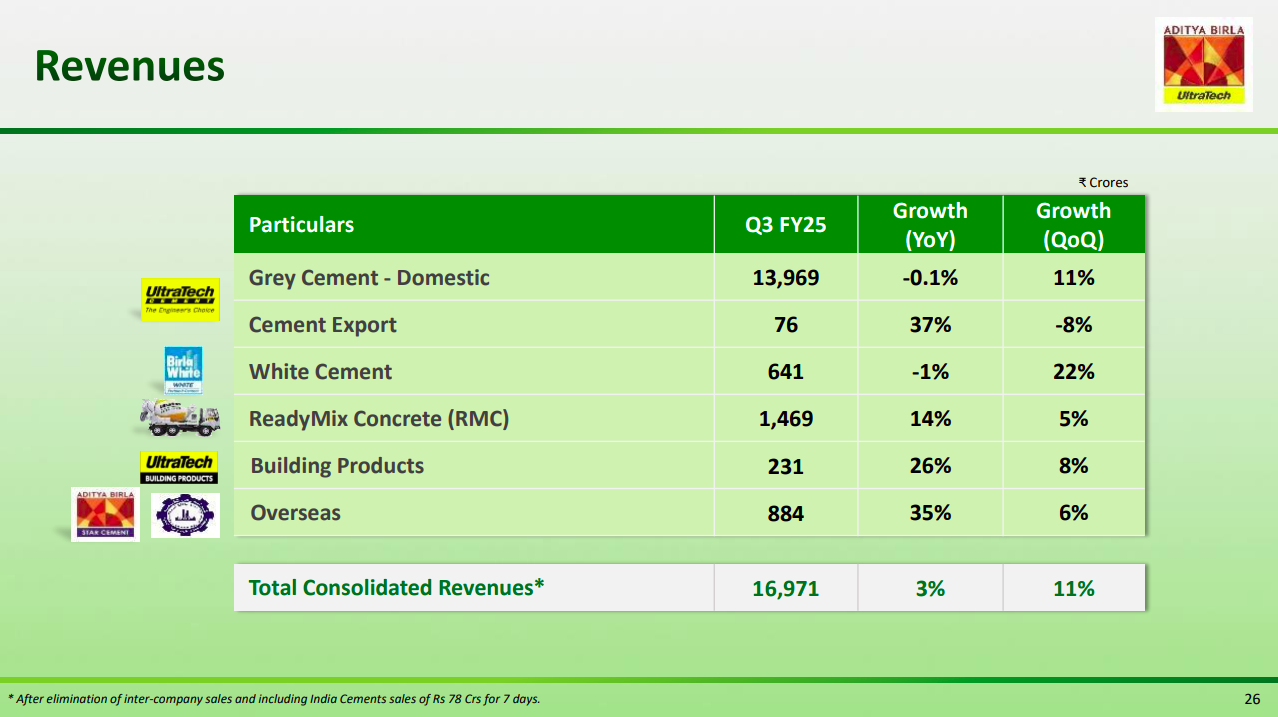

This year, UltraTech Cement brought in about ₹16,971 Cr in consolidated revenue. That’s just a 3% bump from the same period last year, but a healthier 11% jump from the preceding quarter.

Source: UltraTech’s Investor Presentation

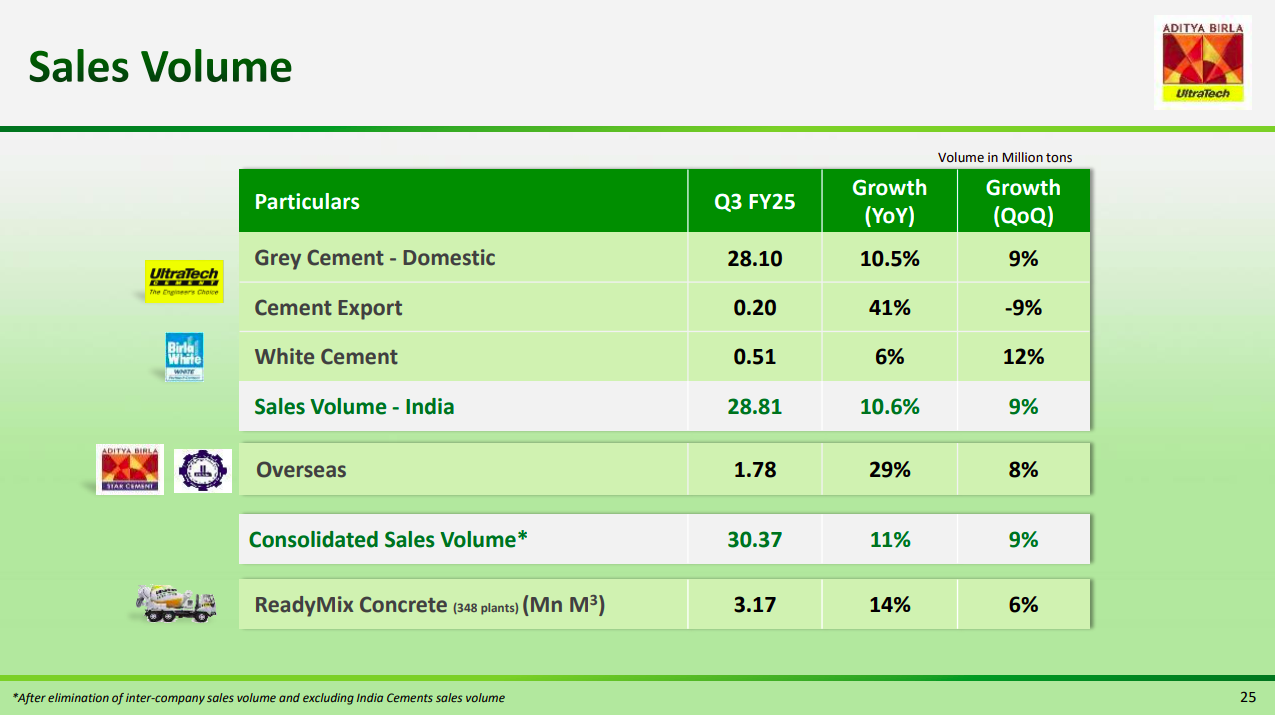

Volumes, meanwhile, climbed roughly 11% year-on-year, outpacing the broader cement industry’s estimated 5% growth.

Source: UltraTech’s Investor Presentation

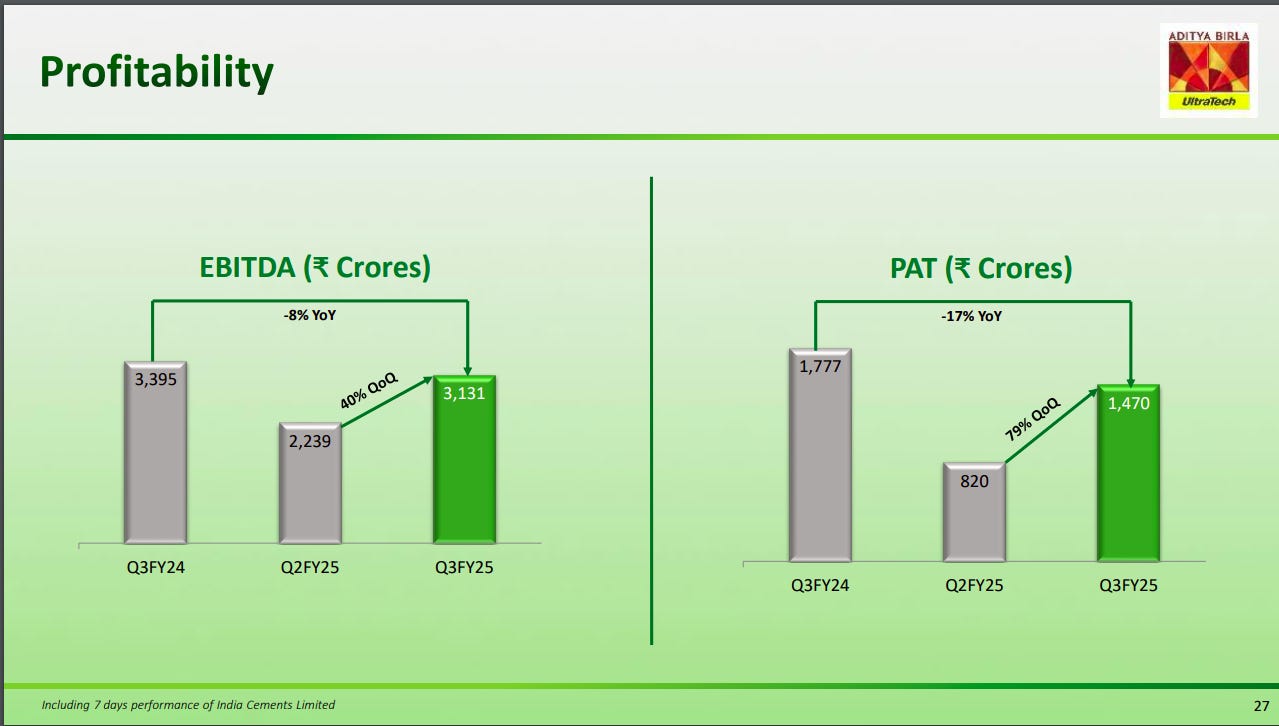

Despite that volume strength, however, the company’s net profit for the quarter actually declined. At ₹1,470 Cr, it was 17% lower than last year’s figure. That said, compared to the previous quarter, profits rose by 79%.

Source: UltraTech’s Investor Presentation

Explaining the revenue-profit divergence

So why this discrepancy between revenue and profit growth?

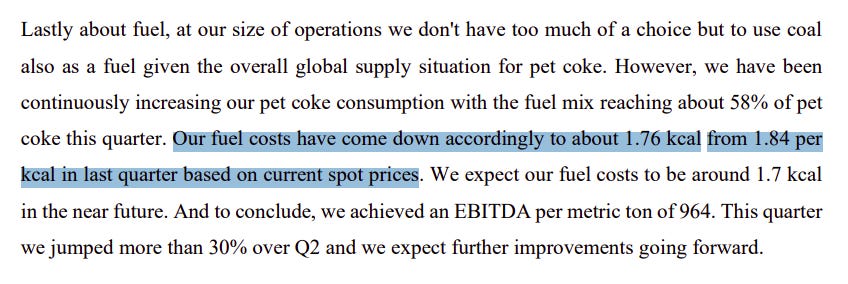

For one, the company saw spikes in the cost of raw materials — specifically, fuel and freight costs. The company spent much of 2024 grappling with expensive pet coke, thermal coal, and diesel. This brought its margins down. As per Chief Financial Officer Atul Daga, however, things started to improve toward the end of the quarter, with the average fuel cost dipping from about ₹1.84 per kcal in the previous quarter to ₹1.76.

Source: UltraTech’s Earnings Concall

The company also tightened its distribution network and shortened lead distances, bringing freight costs down. Even so, these measures couldn’t fully counter the rise in costs. Ultimately, the company’s EBITDA was 8% lower than in Q3 FY24.

A big change this quarter, though, was a distinct pickup in market demand — particularly in December. With more demand, UltraTech could command better prices in the North and West. Daga called it “a lull before the storm ,” explaining that after long months of lukewarm buying, December was when projects finally picked up speed — from rural home-building to infrastructure expansions. So, by his assessment, UltraTech exited the quarter on a stronger footing than it began.

UltraTech big capacity expansion bet

UltraTech believes that India’s cement demand has plenty of runway left. That’s why it has been steadily expanding its footprint — both through new plants and acquisitions. By the end of FY25, UltraTech expects to have roughly 185 million tonnes of capacity, and by FY 27, it aims to cross 210 million tonnes.

Part of that push comes from buying assets, like the 14.45 million tonnes it recently acquired from India Cements. That said, acquisitions like this take time to really fall in place, and it seems like Ultratech Cement is in the middle of that teething process. Those acquired plants haven’t been running at peak efficiency. But Daga claims that once UltraTech’s playbook is implemented, they’ll dial up utilization rates and trim costs. This would take a year or more to fully turn things around.

Kesoram Cement is another piece of the puzzle. UltraTech is waiting on final mine-transfer approvals, after which those plants will join the mix. This will give it a bigger foothold in the South. Ultratech believes that by being closer to Southern customers, it can cut down freight costs.

Why Management believes demand will stay strong

A lot of UltraTech’s optimism rides on the idea that government spending — both central and state — will soon shift into a higher gear. Although the government had cut down on capex for much this year, Daga pointed to signs that key infrastructure projects paused earlier in the fiscal year are restarting and that rural markets are spending more now that the monsoons are done and harvests are bringing in some cash flow.

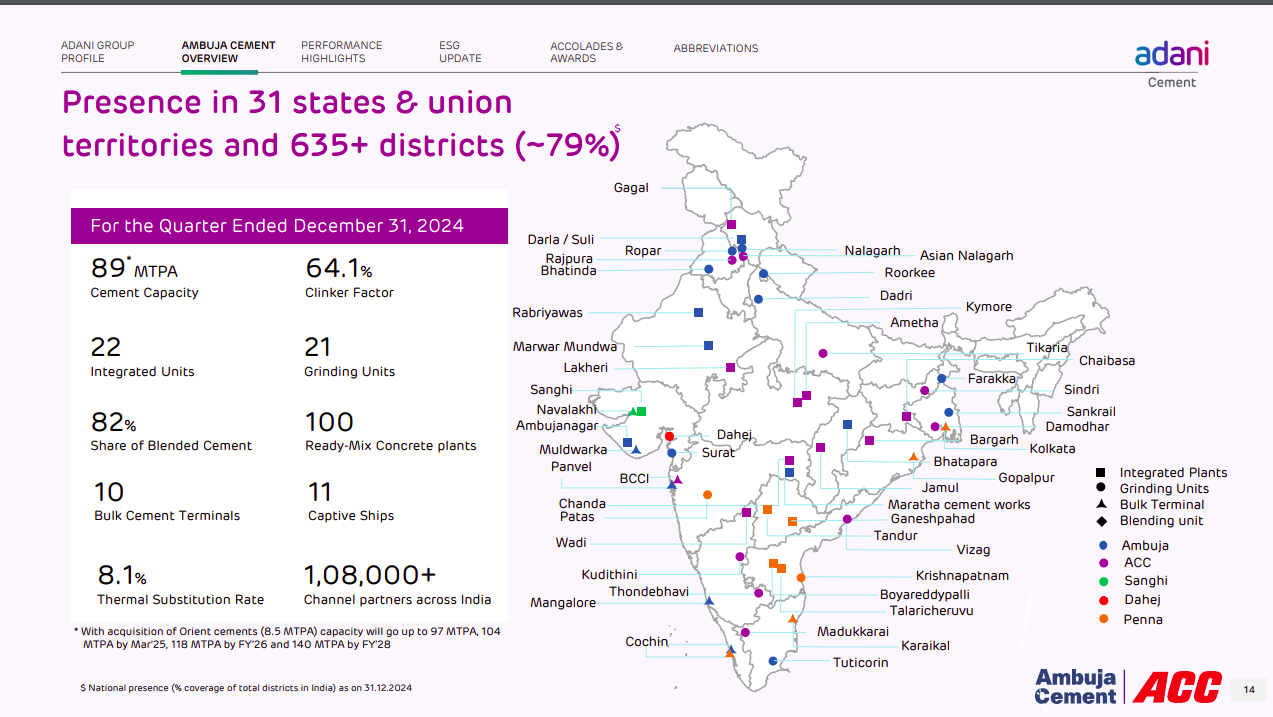

Adani Cement

Adani Cement is essentially the coming together of Ambuja Cements and ACC — two heritage brands once owned by Holcim — as well as newer acquisitions like Penna Cement in the south and Sanghi Industries in Gujarat. Together, these assets place Adani’s total capacity around 90 MTPA.

Source: ACC’s Investor Presentation

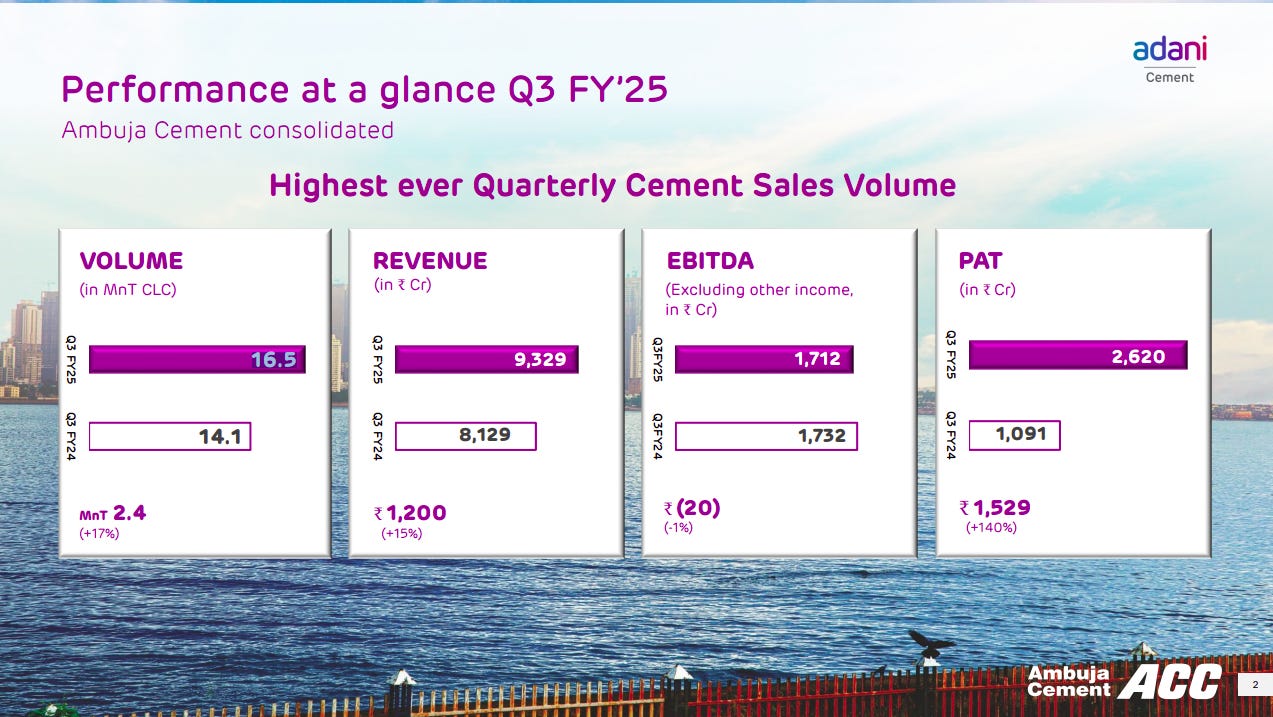

Its revenue this quarter came to around ₹9,329 Cr, marking a 15% jump compared to the same period last year. Sales volumes followed a similar trajectory — climbing 21% year-on-year to 10.7 million tonnes (MT), which is 15% above Q2.

In all, its net profit jumped by a massive 140%, to 2620 cr.

Source: ACC’s Investor Presentation

A big part of the profit jump this quarter came from many government incentives being recognized at once. These payouts, tied to capacity investments and state-level concessions, can arrive unpredictably. They should therefore be seen as a one-time thing — while the company saw a short-term boost in one quarter, the same lump sum might not show up every quarter (or might have already shown up in a previous year), causing its year-on-year numbers to look less dramatic.

Why revenue grew and margins recovered

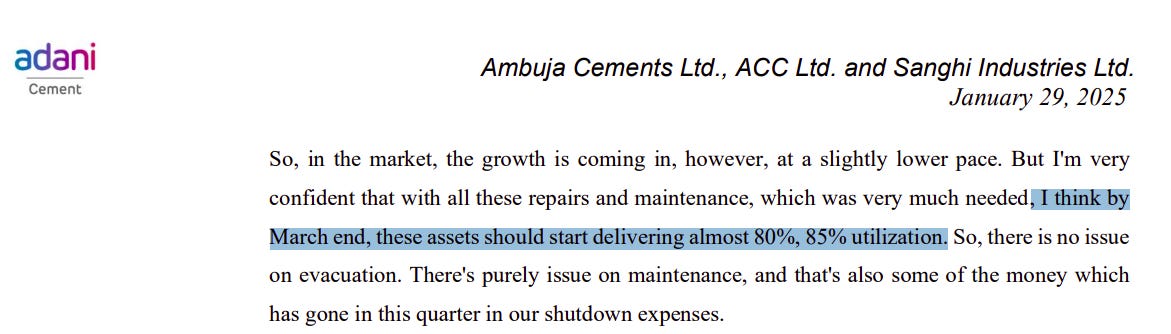

A big slice of the year-on-year and sequential revenue bump came from the company’s higher cement volumes. According to the company, infrastructure projects—especially those that had stalled—picked up steam from December onward. Rural housing demand remained steady, particularly in North and Central India. These factors pushed ACC’s utilization levels higher and helped it weather some of the headwinds it faced earlier in the year.

Southern markets remained softer than in the north, but the company’s overall realization improved slightly quarter-on-quarter.

Why ACC, too, is doubling down on capacity

ACC is in the midst of a capacity expansion that aims to cater to the demand coming in from the rest of the Adani Group — across all its business verticals. The company plans to add or optimize several grinding units to keep pace with the growing cement demand. It is also planning to cut down transportation costs considerably, by bringing its clinker assets closer to their respective grinding plants and connecting its plants through rail and water.

The company is also in the process of integrating newly acquired assets, such as those from Penna and Sanghi. While these plants will eventually improve Adani’s cement business, these integrations carry short-term costs — for plant overhauls, brand alignment, and hiring.

Source: ACC’s Earnings Concall

Why demand might stay strong

Adani Cement believes that demand for cement will soon pick up. Like Ultratech, Adani Cement also believes that government infrastructure spending — despite a subdued first half of 2024 — has shown signs of rebounding. Urban commercial construction has also picked up, aided by new project launches in key cities. The company also suggests that renewed focus on affordable housing, as well as steady rural incomes post-harvest, should keep volumes healthy.

The state of the industry

Despite a subdued start to 2024, when volumes increased by a mere 2% year-on-year during the first half, the Indian cement industry seems poised for a robust recovery. This resurgence will be driven by increased government infrastructure spending, a rebound in urban housing demand, and the improving financial health of rural India.

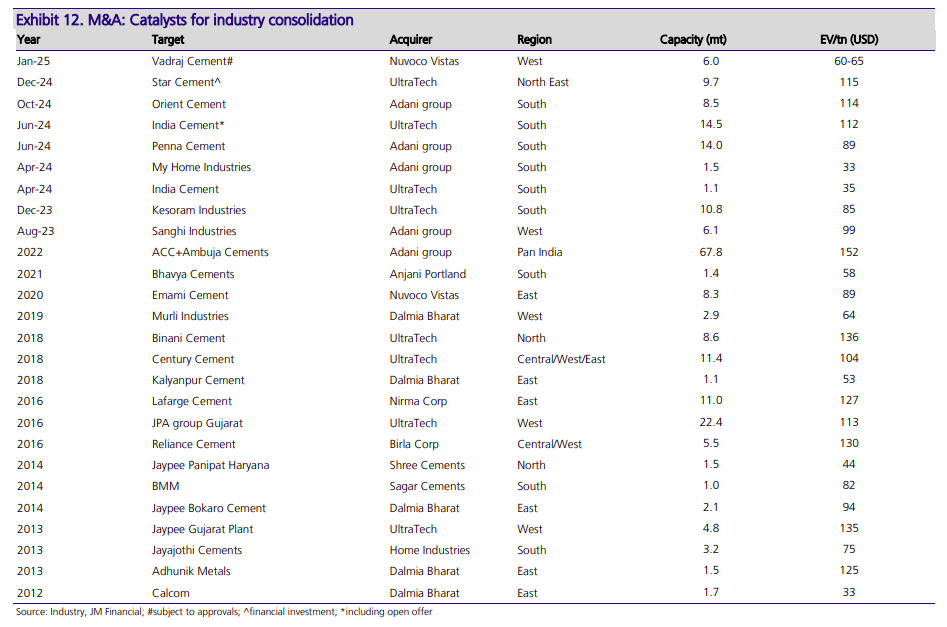

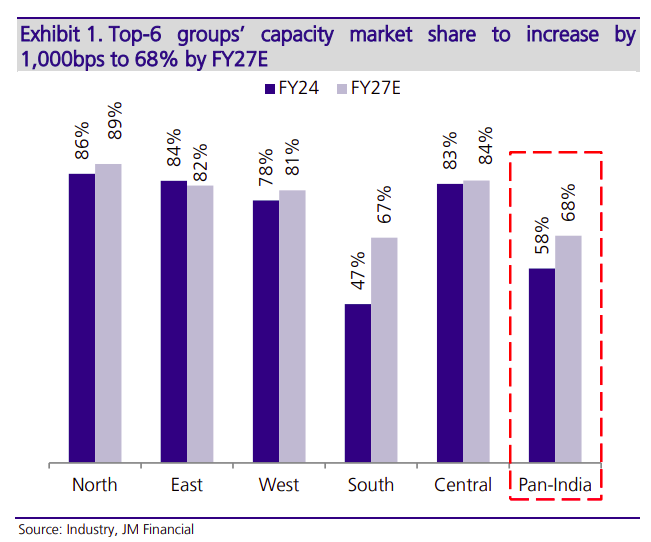

The lull that just went by was a period of consolidation — the latest of many waves over the last decade. Ultratech and Adani Cement have been behind much of this acquisition activity.

Source: JM Financial

Now, the top five or six producers control a majority share of the industry.

Source: JM Financial

This consolidation won’t just streamline operations, but also bolster pricing power among the leading firms. The few players that remain may potentially see improved profit margins. With demand picking up and industry giants firmly entrenched, the cement sector is entering a phase where scale, efficiency, and strategic positioning will define the next leg of growth.

Beer Price War in Telangana

Telangana is one of India’s largest beer-consuming states. Recently, it increased beer prices by 15% after a long, ugly, and very public confrontation with United Breweries Limited (UBL), which supplies the state with Kingfisher and Heineken beer.

But what’s the whole fuss about? Why is Kingfisher fighting a state government? And why is the state government setting beer prices in the first place? That’s what we’ll talk about in our second story today.

Why Telangana Controls Beer Prices

Before getting into the details, let’s understand how the Alcohol industry in Telangana works and how it’s different from other states.

See, Telangana exerts strict control over alcohol prices. Ordinary people can’t enter the business of distributing alcohol. Instead, there’s a government entity — Telangana State Beverages Corporation Ltd (TSBCL) — which has a monopoly on the wholesale of beer and ‘IMFL’, or Indian Made Foreign Liquor, in the state.

Now, since the government controls all sales in the state, it also sets the prices. For this, it fixes a Maximum Retail Price (MRP) for alcoholic beverages. This price is binding. If manufacturers don’t like it, their only choice is to not sell in the state.

Here’s how it all works:

-

Breweries/distilleries propose an ‘ex-brewery’ price — which is the cost at which they sell to TSBCL.

-

These pricing suggestions are sent to a three-member ‘Price Fixation Committee’. This committee reviews the price — after considering cost structures, inflation, and pricing in other states. If it finds the proposed prices acceptable, it can approve them.

-

The government then finalizes an MRP — after accounting for excise duties, distributor margins, and retailer margins.

Now, as far as alcohol manufacturers are concerned, TSBCL is the only buyer of their alcohol in the state. This, sort of, makes them a monopoly and gives them tremendous pricing power. The state liquor depots they run are the only places where a manufacturer can make a sale. It’s then TSBCL, and not manufacturers, that sell alcohol onwards to retail outlets.

And the overall idea behind this model is to make alcohol prices predictable for consumers. But if you think about it, that’s odd, right? Why does a government care about what people pay to get intoxicated? And also, why would they care so much that they have built up an entire liquor distribution system?

Well, that’s where the entire issue lies. One could argue that the state is trying to prevent ‘profiteering’, and wants to keep alcohol affordable for those who choose to drink it. Because, after all, if it becomes too expensive to drink legally, people might turn to all sorts of alternatives — including illegal liquor — which could hurt their health terribly.

But there could also be something more interesting happening here. The Telangana government relies heavily on taxes from alcohol sales. In fact, Telangana earns ₹36,000-₹40,000 crore annually from liquor sales and monthly license fees collected from liquor dealers. This makes it one of the largest sources of the state’s revenue.

And for that, the state sells 45-55 lakh cases of beer monthly — even more than the hard liquor it sells. For this revenue to keep coming in, you obviously need more alcohol sales. Keeping liquor cheap does exactly that.

The troubles of United Breweries

The problem with Telangana’s complicated alcohol pricing system, though, is that it comes with significant downsides for manufacturers. And that’s precisely what we’ve seen play out over the last month. For beer companies like UBL (which owns Kingfisher and Heineken), the Telangana pricing model creates a serious profitability crisis.

Now, Telangana is really big for UBL. The state contributes 18% of its volumes and 15% of its revenue. But despite this, doing business in the state has become increasingly difficult for the company.

The state hadn’t revised the cap on beer prices since 2019-20. Meanwhile:

-

Raw material inflation (that is, the prices of things like barley, glass bottles, logistics, etc.) has surged in the last five years.

-

Telangana’s ex-brewery price has been among the lowest in India. As a result, UBL earned just ₹300 per case in Telangana, compared to ₹500 per case in its northern neighbor, Maharashtra.

On top of all this, the state government has often lagged in paying its dues to alcohol companies. For instance, the state government owed more than ₹3,600 crore to beverage companies in unpaid dues, including ₹658 crore to UBL as of January 2025. This added to the already strained commercials of selling alcohol in the state.

So, manufacturers faced squeezed margins, unpaid dues, and no price revision. In essence, their earnings were lowered artificially — at least when compared to other states — and on top of that, they weren’t paid that lower amount as well.

And so, in January, UBL took a drastic step — it halted beer supplies entirely to TSBCL.

This was a big deal. When a big company like UBL, which controls about 70% of Telangana’s beer market, refuses to supply a popular beer — in a State that sells huge volumes of beer every month — the Government came under pressure. After all, while the government might broadly want to keep alcohol consumption under control, it also has to ensure that manufacturers stay interested in selling in Telangana. If companies start walking away from the state or reduce their supplies, that could create liquor shortages. Not only would that upset consumers; but it could also lead to a massive loss in revenues.

So, recently, after a lot of back-and-forth, the Telangana Government gave in and hiked the prices of beer by 15%. This was still not as much as the United Breweries was asking for. After all, their costs have gone up significantly over the last half a decade. Even after the 15% hike, margins in Telangana still remain lower than in Maharashtra, Karnataka, or even UP. They had asked for a ~33% hike. But with that said, 15% was still the biggest single jump in beer prices the state of Telangana had seen in a really long time.

Where do we go now?

So, while United Breweries may have gotten some temporary relief from this 15% hike, it’s only a short-term solution. The involved parties also call it an “interim” arrangement. However, the state’s deeper problems still remain.

Telangana’s rigid price controls and state monopoly over alcohol distribution may provide predictable revenue, but the core issue lies in the government’s dual role as both regulator and trader.

As a regulator, its incentive is to control alcohol consumption and curb illegal liquor sales.

But as the sole buyer and distributor of alcohol, it is also incentivized to prioritize revenue, supply, and price stability.

These competing objectives inevitably lead to confusion and distorted decision-making, which is exactly what we’re seeing now.

This results in delayed price revisions, payment backlogs, and strained relations with suppliers like United Breweries.

So, in summary, while the government may have temporarily avoided a crisis unless it rethinks its broader approach, these situations will keep recurring—which, of course, isn’t good for any of the involved parties.

Reliance vs ONGC: The $1.7B Gas Dispute

Last week, the Delhi High Court set aside an arbitration award by a Singapore-based tribunal, which protected Reliance Industries from a $1.7 billion claim by the Indian government. That’s roughly ₹1.5 lakh crore, by the way. At the heart of the dispute was an odd claim — that Reliance was pumping out ONGC’s gas from its own gas fields in the Krishna-Godavari Basin.

But how could this ever happen? And why was a tribunal in Singapore hearing a dispute between India’s largest company and the Indian government, over Indian gas fields?

Well, that’s a story that spans many decades. Let’s dive in.

The twin gas fields

The roots of this conflict go all the way back to 2000.

Back then, Reliance and its partner Niko Resources were awarded a block, called the ‘KG-D6 block’. Right next door lay two other blocks, which were operated by ONGC. There was an interesting fact, however, that nobody fully knew at the time: beneath the ground, Reliance’s block was connected to those of ONGC. So, in 2009, when Reliance began extracting gas from its own block, it also began sucking in gas from ONGC’s blocks, as though by a straw. ONGC, meanwhile, hadn’t developed its own blocks, so it didn’t catch on to what was happening.

That changed in 2013 when ONGC noticed something was amiss. Its internal studies showed a connection between its blocks to those of Reliance. It approached the Directorate General of Hydrocarbons — India’s oil regulator — alleging that Reliance was siphoning off its gas. This was a serious charge. ONGC alleged that Reliance had, in effect, stolen gas that didn’t belong to it.

Instead of taking Reliance head-on, however, ONGC pulled the government into the dispute. It essentially asked the Government to step in and protect its rights. The government brought in a US-based expert — DeGolyer & MacNaughton (D&M) — to figure out what actually happened. D&M confirmed ONGC’s worst fears. Between 2009 and 2015, about 11 billion cubic meters of gas had migrated from ONGC’s blocks to Reliance’s area. Reliance had already produced and sold about 9 billion cubic meters of this gas. The value of this gas? Approximately $1.5 billion .

What’s more, Reliance appeared to know that their block was connected with that of ONGC since 2003.

But there was a twist. The expert committee that the government set up for this dispute held that Reliance didn’t owe ONGC anything. It hadn’t actively tried to steal ONGC’s gas. That said, it did take gas it didn’t have a right over. Under Indian law, all underground hydrocarbons belong to the government. Contractors are only permitted to the gas within the limits of their block. So, it wasn’t ONGC that Reliance had to compensate — it was the Indian Government!

Based on this finding, in 2016, the government demanded $1.7 billion from Reliance.

The current dispute

But here’s the thing: if the dispute was just between ONGC and Reliance, normal Indian law would apply.

That changed when the government stepped in. When it came to gas extraction, Reliance had a very specific contract with the government. And that contract said that if the two were to ever fight, the dispute would have to be settled through arbitration.

And so, Reliance and Niko asked for international arbitration — which would not be held in India, but in Singapore. In 2018, the arbitration tribunal sided with Reliance, by a 2-1 majority. It found that Reliance had a clear right to take gas from its block. How that gas got there was none of its concern. There was nothing in their agreement that stopped Reliance from taking gas that ‘migrated’ from elsewhere into its block, as long as it wasn’t stepping outside its boundary to extract it. And so, it didn’t owe the government anything.

The government challenged this award. In May 2023, however, a single judge of the Delhi High Court refused to interfere with the tribunal’s award. The tribunal had taken a fair view, the High Court noted, and anything it said should be binding unless it was blatantly perverse.

The government, however, appealed against this decision, to a two-judge bench of the High Court. Last week, that bench reversed this position. The judges emphasized that natural gas is a “vital national resource belonging to the Union of India as a trustee, in the public interest of the people.” In essence, the government holds gas on behalf of the Indian people, and no matter what the contracts say, private companies can’t simply take it for their own benefit.

What comes next?

For now, the old $1.7 billion claim is back on Reliance’s head. The company, however, has indicated it will appeal to the Supreme Court. Meanwhile, ONGC finally began production from its blocks in January 2024, though much of that gas may have already been drained.

The implications, however, extend beyond this specific case. The dispute has exposed big gaps in India’s regulatory framework for managing shared reservoirs. After all, underground natural resources don’t respect the boundaries we draw on top of the land. Under the neat parcels that the government puts up for auction, the reality is messy. Globally, such situations are typically handled through “unitization” agreements: where connected reservoirs are developed together, and entities share benefits proportionally. With this experience, India too might start planning things differently.

Tidbits

- SAIL is investing $800 million in a new rail mill despite no confirmed purchase commitment from its biggest customer, Indian Railways. The company’s existing rail production at Bhilai and forged wheels at Durgapur have catered to railway demand, but Indian Railways has remained non-committal about future procurement.

- Aurobindo Pharma’s China facility, which began operations in November 2024, will start supplying to Europe by April 2025, with U.S. approvals pending. Despite these expansions, Q3 FY25 saw a 10% YoY decline in net profit to ₹846 crore, while revenue rose to ₹7,979 crore from ₹7,352 crore in the previous year.

- NHPC plans to invest ₹84,000 crore to develop 20 GW of pumped storage capacity, with a total capex of ₹1.2 Lakh Cr., primarily through joint ventures where NHPC will hold a 70% stake in most projects. The company has 20 PSP projects in various stages, including five in Andhra Pradesh under a JV with APGENCO.

- This edition of the newsletter was written by Krishna, Anurag and Pranav

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]() Join the discussion on today’s edition here.

Join the discussion on today’s edition here.