Centrum broking has recently shared an interesting report on the Auto Finance NBFCs space covering the following companies ; M&M Finance, Shriram Finance, Cholamandalam Finance and Sundaram Finance. Here are some key highlights:

Auto finance NBFCs - Key Highlights:

Auto finance NBFCs reported AUM growth in the range of 13-38% over the last 12 months driven by strong auto demand and business diversification.

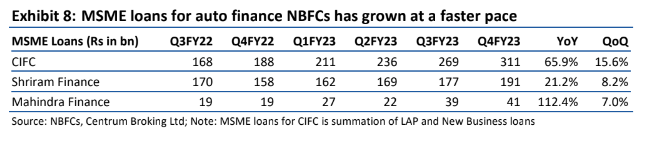

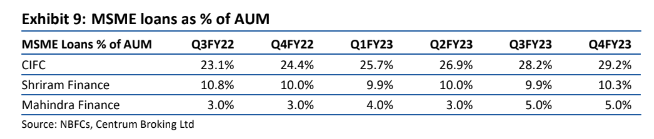

MSME is the new growth engine.

Improving Asset quality due to improving collection efficiency.

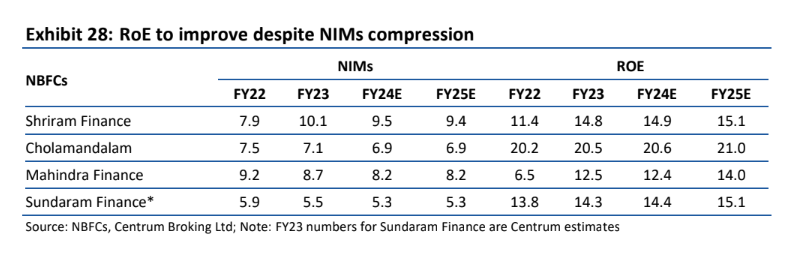

Lower Net Interest margins due to prolonged rate hikes but higher RoE due to stronger growth.

The liability profile for NBFCs are diversified and there are no ALM mismatches across tenures.

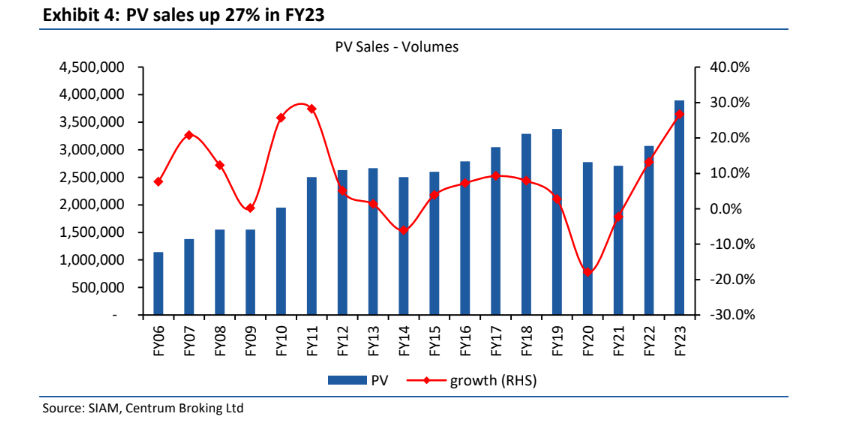

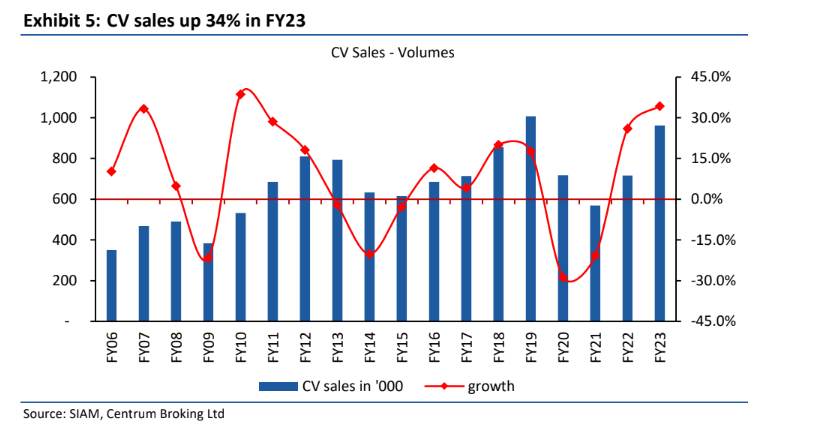

1. Passive Vehicle and Commercial Vehicle sales - Back to moderate growth after a stellar year?

-

In FY23, CV sales grew at 34% while PV grew at 27% annually. According to industry estimates, PV volumes are expected to grow in the range of 5-7% in FY24 due to high base, waning pent up demand and increase in total cost of ownership.

-

However, price hikes should support low double digit revenue growth. CV sales are expected to grow 9-11% in FY24.

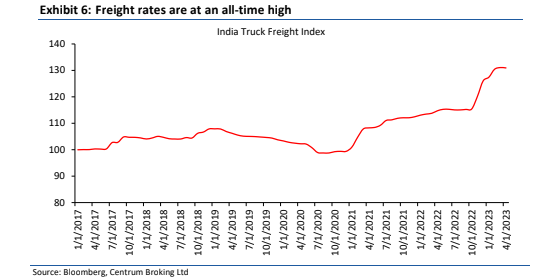

- Transporter freight rates are at all-time high indicating strong cash flow generation for fleet owners. An average of freight rates between Delhi and 81 other cities in India can be seen in the below chart.

2. MSME – The new growth avenue?

With nearly 7 crore MSMEs with an estimated credit demand of 106 trillion, Only 20% is addressed through formal channels.

Even if some part of the credit is captured by NBFCs, the scope for growth is tremendous. This would also ensure diversification in AUM and reduction in cyclicality .

Share of NBFCs and private sector banks have increased in MSME loan origination.According to CIBIL Transunion, disbursements in PSBs, Private sector banks and NBFCs grew at 21%, 25% and 34%, respectively.

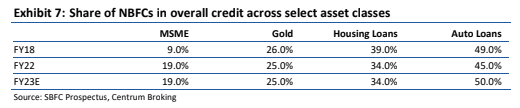

Share of NBFCs in MSME credit has increased from 9% in FY18 to 19% in FY22 due to their focus on customer service, faster turnaround time and geographic reach.

-

Formalization of MSMEs has led banks to capture more data from GST portals, alternate data sources and is enabling better underwriting, credit processing and quick loan disbursals. Also, tie-up with Fintechs for lead generation and use of alternate data for credit appraisals has led to uptick in small ticket size loans.

-

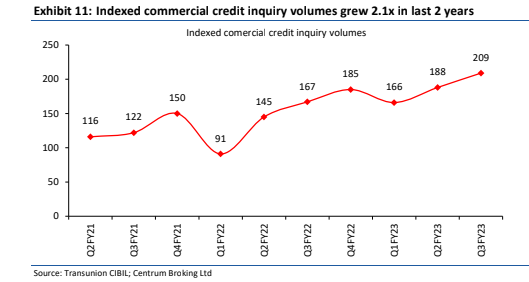

As per CIBIL Transunion Report, demand for MSME loans has grown 1.7 times the demand seen two years ago (as on 2QFY23). NBFCs saw credit demand crossing 2x for the same period.

Commercial Credit inquiry is on the rise

- Recovery in economic and business activities led to demand for commercial lending. Commercial credit inquiry volumes saw 1.8x growth in last two years with NBFC growth at 2.1x over the same period.

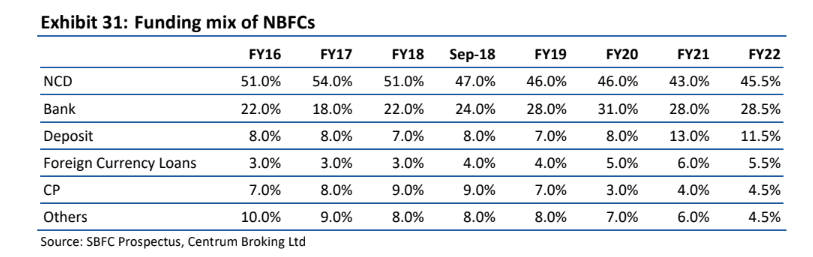

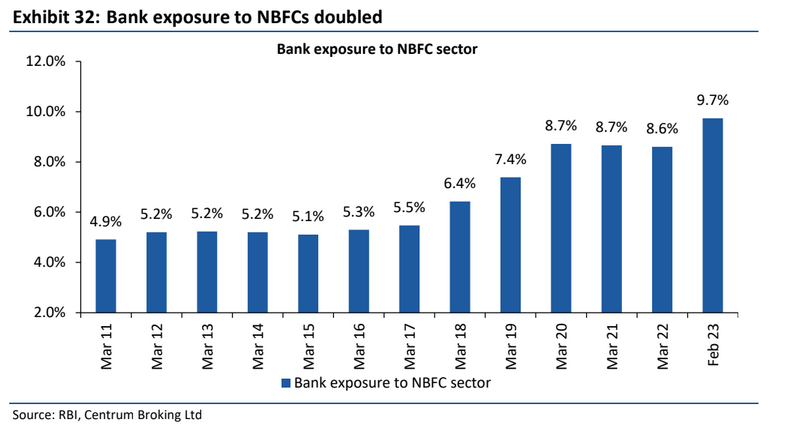

Liability profile diversified after IL&FS crisis

- NBFCs diversified borrowings mix after IL&FS crisis. Share of NCDs and Commercial Paper declined in funding mix while the mix from the other sources increased.

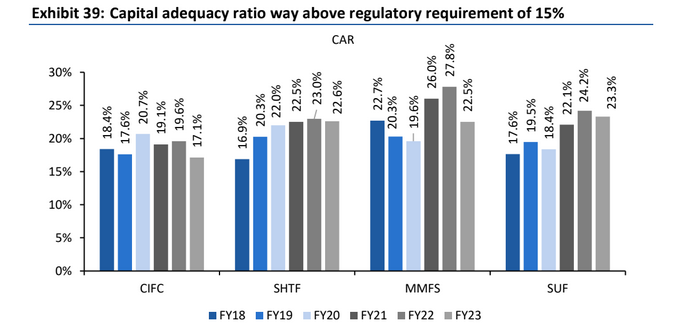

- Funding from debt MFs declined from 19% in July 2018 to 8.5% now. This was offset by an increase in bank exposure to NBFC sector, which is up from 6.4% in Mar 18 to 9.7% in Feb 23. Post Covid, banks have increased funding towards NBFCs as their balance sheets strengthened with strong capital adequacy ratios and high provision coverage ratio.

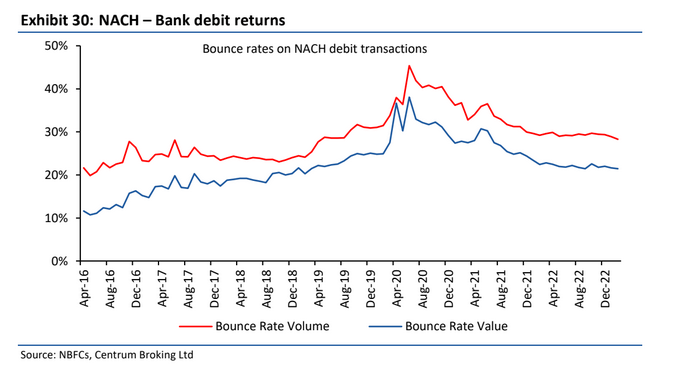

3.Asset quality continues to improve

- On a system level, banks have witnessed improvement in decline rates in NACH transactions, which suggests an overall improvement in collection efficiency and better asset quality environment.

Biggest risk in the coming year

El-Nino impact on farm cash flows

El Nino generally impacts the asset quality of rural focused NBFCs as GNPA and credit costs rise.

Even though, The reservoir levels at an all India level are 28% above the 10-year average. However,Eastern India may be the pain point due to the deficit monsoon last year.

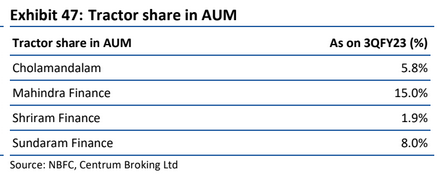

Few more Interesting charts

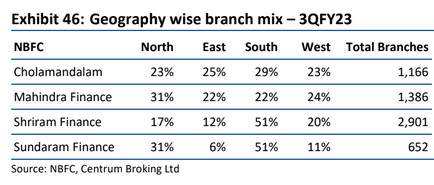

Tractor share in AUM

Geography mix

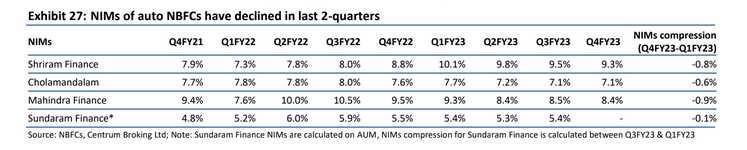

4. Lower NIMs due to prolonged rate hikes but higher RoE due to stronger growth

Capital raised during Covid period strengthened Balance Sheets

- Cost of Funds for auto NBFCs increased after a longer than expected cycle of repo rate hikes. Repo rate increased by 250 bps over the last one year to 6.5%. NBFCs increased lending rates by 25-200 bps in FY23, while CoF increased by 30-100bps. Also, the interest rate hike is on fresh disbursements, while the old book is at a fixed rate suggesting near term NIMs Compression.

- Auto loans are fixed rate loans and rate transmission will be visible as the old book gets replaced with fresh disbursements. However, given the impact on demand, NBFCs may favor growth as Return on Equity (RoEs) is likely to remain stable.