I am evaluating whether I should consolidate all my Mutual Funds on COIN or MF Utility. I have an account with both now.

MF Utility: MF Utility activated my CAN and Online Login. However, it seems I need to complete a physical form before I can initiate a SIP on their site. I find that extremely discouraging. I thought it is completely online but it’s not. Plus, the interface is not great. The only things I like is that it’s absolutely free and it is recognized by almost all AMCs, AMFI & SEBI. Very legit I think. There is no issue with any fractional units, you can buy & sell in decimals (fractional units).

COIN: Everything was set up online, no paper forms. Can buy/set up SIP online without any paper forms. Charges are INR 50 a month plus demote charges of INR 300 a year plus every time you redeem, there is a charge. The biggest problem seems to be that you can’t redeem Fractional units. If you have 220.76 units in a folio, you may forever be stuck with the .76 units. Is there a solution to that?

Direct AMC: How about I continue to invest directly on the AMC websites. Now that I have a CAN from MFU, if I die or something; my heir only needs that one CAN to access/redeem everything; even though I don’t invest through MFU. Is my interpretation correct?

When you are investing through COIN, the units allotted to you are in demat form which is a more secure form of holding your securities. You can can add anyone as a nominee to your demat account, then that person would be the legal heir to all the securities in your demat account.

With respect to your query on fractional units, you can redeem fractional units on COIN too. Every scheme has minimum redemption quantity so if you hold units which are less than the specified quantity then you might have to buy some more and then redeem all the units. But, most of the schemes specify a minimum redemption quantity of 0.001, thus it should not be a problem.

However, if you are facing any problem while redeeming fractional units then you can drop an email to [email protected] and we will investigate the issue.

Awesome! Thanks for clarifying and that was super quick

Could you also confirm if opening a Joint Demat account with Wife is legal easier for her to manage compared to adding her as a nominee, in the event of my demise. I don’t mind opening a new Demat account it’s just INR 300 a year or so.

Also, can I delete/deregister from MF Utility’s Common Account Number as I don’t care for them really.

I would say you should go ahead with opening MFU CAN number and then just set-up their payEZZ facility. That is easiest. You can always nominate one person and that should be applicable across all AMCs. There are no transaction charges. As far as demat is concerned, you don’t need demat account for mutual funds, because AMCs don’t really allot paper based units. So my take is go with MFU. I am using the same facility, its easy and simple. However, one caveat here is that most of AMCs have joined MFU but not all. You can check list of participants from the website. One prominent exclusion is Mirae Asset.

Just curious, if you had are already invested (done transaction) with direct with AMCs then KYC is done and your bank account is also linked then MFU should have enabled paperless application for you.

I prefer MFU compared to myCAMS or direct AMC website since it is an aggregator and enables multiple transactions (like shopping cart) across AMCs. Best of all, payment is delinked from transaction. You can pay by NEFT/RTGS or Payezz (NACH mandate).

Agreed interface is not great but then it is transaction platform, I expect some analytics would come up in future.

I liked the idea of coin and the features it provides. 50₹ per month is also acceptable for me. But my worry is that, if zerodha decides to increase this fee in one morning, I’ll be forced to pay it till fund’s lock in period. For zerodha it is just a matter of big long a post saying operational cost blah blah… Without getting written confirmation saying that 50₹ will maintain till life long for my account, I am scared to commit to coin. I’ll go with mfu for now.

Point me to a company which has as you say in WRITING said they are gonna keep their subscription fee fixed. What nonsense is this. Dude, inflation affects everyone including companies, that’s the reality. Why don’t you ask the govt in WRITING to fix fuel prices?

You know MFU is handled by mutual fund companies themselves. Right? They don’t offer demat or trading account. How do you think they will force us to pay fee in middle of subscription? Zerodha will charge fee to trading account and as soon as we withdraw, money will adjust with negative balance in trading account. MFU just act as intermediates between bank and mutual fund companies. Probably they will introduce account opening fee. But for monthly charges, chances are very slim. And since they are not holding the fund, we will not be forced to pay for continuing existing subscription.

Life insurance. Just because you asked me to point something. They says this is premium we need to pay for life time. They give in writing. I pay, plan continues. Simple as that. I don’t think in middle of subscription they will just double the premium.

1) What is MF Utility?

MF Utility (MFU) is an innovative “Shared Services” initiative by the Mutual Fund industry under the aegis of Association of Mutual Funds in India (AMFI), which acts as a “Transaction Aggregation Portal” through which a Mutual Fund customer is enabled to transact in multiple schemes across Mutual Funds using a single form/payment.

2) How does it work?

It provides browser based access to Mutual Fund customers, with connectivity to Registrars and Transfer Agents (RTA), Banks, Asset Management Companies (AMC), Payment Gateways (PG) and KYC Registration Agencies (KRAs) and enables online transaction submission in multiple schemes across Mutual Funds through a single form/payment.

3) Who operates and owns MF Utility?

MF Utility (MFU) is operated by MF Utilities India Pvt Ltd (MFUI) which is equally owned by the Participating AMCs.

Doesn’t mean they can’t pay you to go on various forums and promote them right. They wouldn’t be the first ones to do this!

What you specifically said was “What you should really be shocked to know, is that Coin gets both” don’t point me to a generic article. When are you are alleging something you should have hard proof, otherwise you sound like a kook.

Fantastic! The kiska baap ka paisa business model and why not, has worked fantastically for hundreds of other startups.

One word, Sahara!

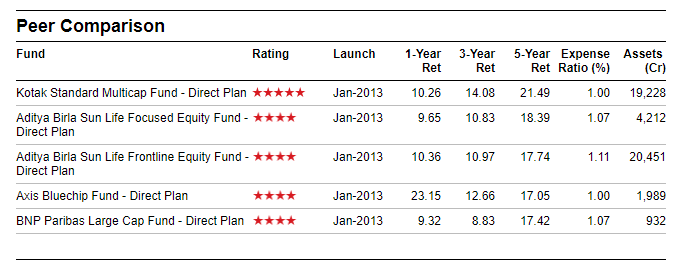

what Kotak fund and dude, just because a platform lists a fund doesn’t mean investors go buy the fund. Do you think they are really that stupid? Assuming that they did invest, pretty sure the fund has handsomely rewarded them compared to an index fund. Still not sure why you bought this fund up.

Considering the fact the MF AMCs are so pure-hearted and ethical how can you beyond a reasonable doubt say that they aren’t? Afterall how can they continue to survive on VC money? They must make money somehow and this seems like an easy start.

No idea how this makes a difference to me as an investor.

And for writing, I am not expecting a legal document to sign and send to me. Some assurety is enough in web page that says something like, current subscription fee will continue for existing mf subscriptions, any revision in fee will only applicable for newly subscribed funds. I do not think my wish is not reasonable

Yes, you did. You said"Shocked to know" I know I don’t have a PHD English lit but, that sure as hell sounds like putting someone down or written with an intent to defame. You didn’t say. Kuvera is free but you would “Shocked to know” they make money in marketing fees from the AMC’s.

Comparing Kuvera’s VC funded model to that of Google and Facebook’s initial days is like comparing Meryl Streep to Poonam Pandey, not the same. If you would have listed some Fintech’s, that would have been a whole new conversation. Let me give you examples, Betterment, Wealthfront and even India’s own smallcase, all have raised money and all have some revenue models.

You said financial crimes are possible but Kuvera won’t do it. How can you be sure?

Sir, costs matter and so do returns. Now I have no idea what you insinuated when you bought up Kotak fund.

Insinuation 1 - Kotak paid Zerodha money to promote. Here’s the result

Insinuation 2- Zerodha doesn’t give a shit about investor interests and they are promoting an inferior fund

Insinuation 3- Index funds have performed better than Kotak with low costs. No matter what, I see that it hasn’t made a difference.

Ahem,

In India, we don’t have fiduciary duty laws. What’s the difference between Coin listing some funds and Kuvera recommending some funds? If they don’t perform, it’s not like investors have recourse in either of the scenarios.

I am because, I’ve seen guys like you here, Reddit and Quora blatantly painting other platforms in a bad light while openly being promotional. What are you guys messiahs for investors in India.

No I don’t. You know why? it is for this exact reason. People are smart and they’ll figure out shit for themsleves. They don’t need salesmen in this day and age.

I am because you are. If you do it on your FB profile or twitter handle, then that’s different. But when you do it on a moderated forum like this then, criticism is fair game.

Disclosure: I use Zerodha for both stocks and MFs and I don’t mind paying 50 bucks.

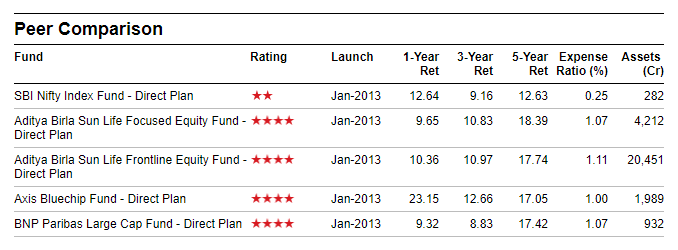

Nope, you said “they recommend low-cost index funds because they actually want to protect investors from having to pay high costs.” Which is why I posted the screenshot of their recommendations. Obviously, I am an expert to judge their choices, but I have been around in the markets for a long time enough to say “recommendations don’t matter” unless there is a fiduciary duty clause. If an advisor is giving advice then he should be held responsible. Currently, they might as well say, Oops, my bad.

My problem is with “Oh Kuvera is awesome, Coin is bad” blatant promotion. That is PLAIN WRONG.