Was reading this circular that NSE has just put out

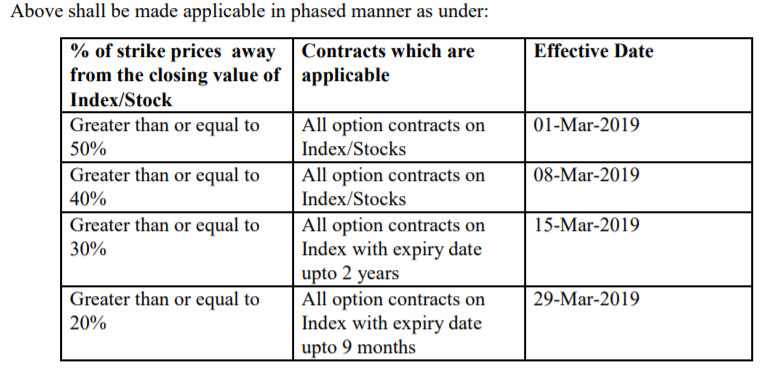

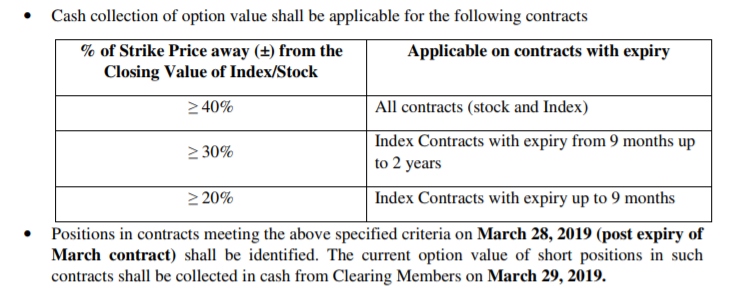

The current value of ITM/OTM options contracts shall be collected by Clearing Corporation in Cash for all net short positions as per parameters specified in table below

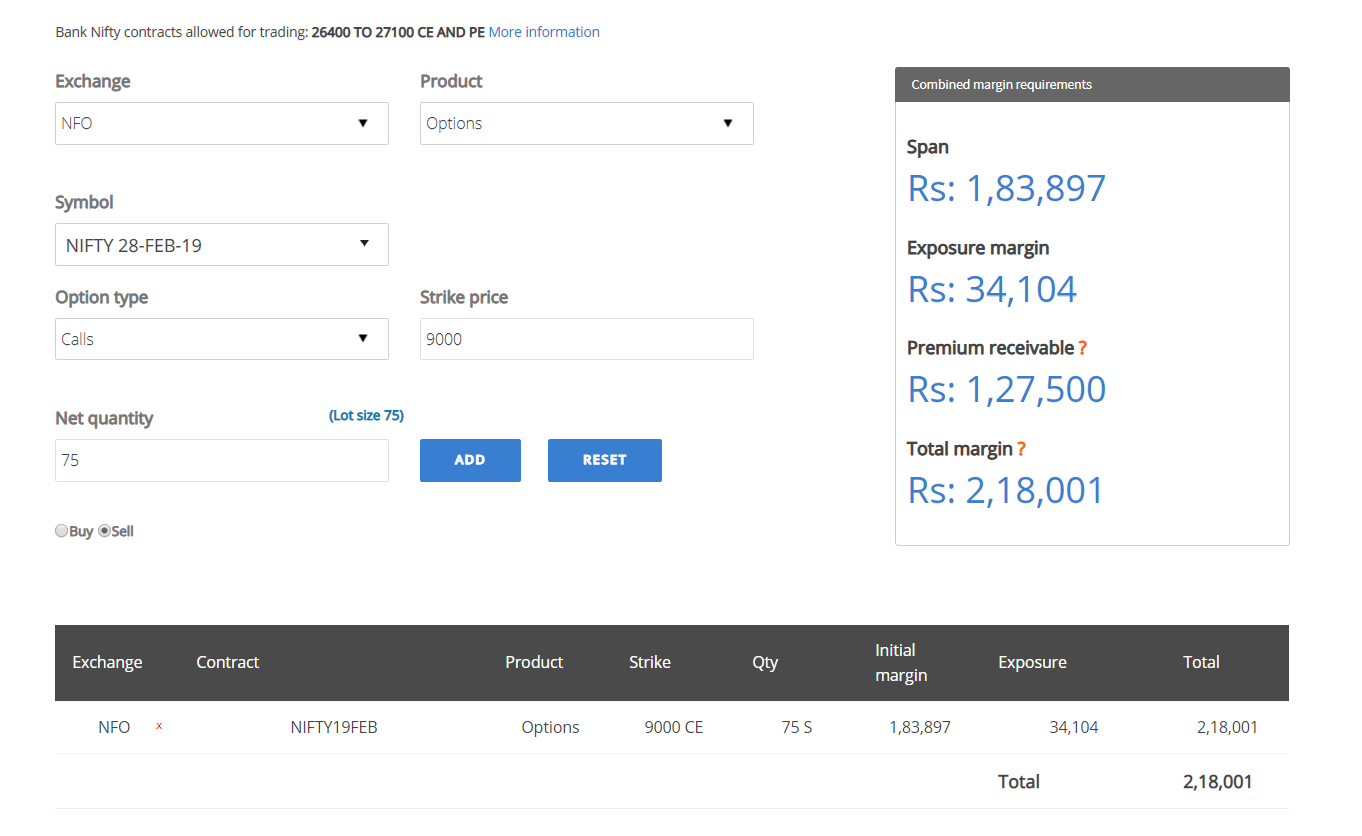

When you short options, the premium received gets credited to the trading account. Let me take an example of 1 lot short 9000 calls of Nifty (I am taking a deep ITM option as this is what the circular is trying to address to).

Even though the margin required is 2.18lks to take the position, once you take the position, the premium of Rs 1.27 lks gets credited to you. So the net margin blocked is only around 90k. To take the above position, you could bring the entire Rs 2.18lks as collateral margin (pledging stocks that you hold) and then the Rs 1.27lks would get credited to you as cash.

But going forward for strikes which are either below or above the current market price by 20%, the premium component of the margin cannot be funded by collateral. So in the above example, Rs 90k could be used from collateral margin and the remaining Rs 1.27lks has to be funded by cash.

How does it affect F&O traders?

It doesn’t in any way. Almost everyone trades only on strikes which are within 20% of the current market price. Even if someone trades outside the 20% strike range, it is usually OTM options which have very small premium component to it. So if that premium was asked to be brought in cash for the seller, it wouldn’t make any difference. For example Nifty 12500 Feb calls are trading at 0.5 or just Rs 40 in premium.

Why put this up if it doesn’t make any difference?

My guess: All of us would have read the breaking story in Jan on the huge build up in OI on June Nifty 5000 calls, 50% below the current market price. Very questionable the intent of people who are trading them. If someone is putting up so much premium, why not just take a future position and rollover till June? Liquidity, impact cost, etc would all be cheaper. This had a feeling of being a structured kind of deal being executed on the exchange platform - especially in the longer dated index options. There have been similar instances on certain strikes of stocks as well. With this new rule, the margin required to trade such deep ITM strikes would double or more and make taking such trades extremely expensive in terms of margin requirements.

Nifty 5000 calls has intrinsic value of around 6000 points. That means, to buy 1 lot of Nifty 5000 June calls, you’d need around 6000 points x 75 = around Rs 5lks to buy just 1lot. Instead you can put up 1 lk and buy futures and have exact same P&L. So if someone is buying 5000 calls, you’d know something is wrong.

There are many ways in which this can be misused, one example below on how this be used for funding kind of deals.

Assume Person A is a financier and Person B is someone in need of money. Person B can put a small margin and short 5000 calls and 15000 puts on the long dated options (say 2020). Person A buys these options. For every 1 lot, 10000 points or Rs 7.5lks. Person B could use his stock holding as collateral to get into these trades. So if person B has Rs 5lks worth of stocks, he can pledge them with his broker and take both these short positions with around Rs 2.5lks. Once he shorts it, he receives premium worth Rs 7.5lks to his account. He can do anything with this. It becomes an extremely easy way to send money from one account to another. Person A could be a financier, or Person A could be having his account managed by an advisor who find this unique way to send money to someone else without person A realizing what is happening and thinking this as a genuine trade.

What if the financier is a FPI (Foreign institution) and person receiving the premium is a local entity. This becomes like a conduit for FPI’s to lend money in India which they are not allowed to otherwise.

Thanks for the explanation. But it may not be right to say that traders only sell premiums 20% above or below when we can clearly see that is not the case. Definitely not a good news for the option sellers. Margins were recently increased and we can see it’s impact on returns. Now this move we can’t do much about it and have to look explore better options.