Over the past few years, retail investors in India have gained access to direct bond investing through platforms like GoldenPi, Wint Wealth, and Grip Invest. These platforms fall under SEBI’s regulated Online Bond Platform Provider (OBPP) framework, meaning they follow strict compliance norms for investor protection.

But here’s the truth:

![]() They are not the same product in disguise.

They are not the same product in disguise.

![]() Each platform targets a different type of investor.

Each platform targets a different type of investor.

Let’s break them down.

![]() Personal note: I’ve been actively investing and monitoring multiple bond platforms around 2 years, tracking returns, defaults, liquidity, and overall user experience. This review is based on both hands-on experience and market understanding.

Personal note: I’ve been actively investing and monitoring multiple bond platforms around 2 years, tracking returns, defaults, liquidity, and overall user experience. This review is based on both hands-on experience and market understanding.

GoldenPi Review — Best for Variety & Flexibility

GoldenPi Review — Best for Variety & Flexibility

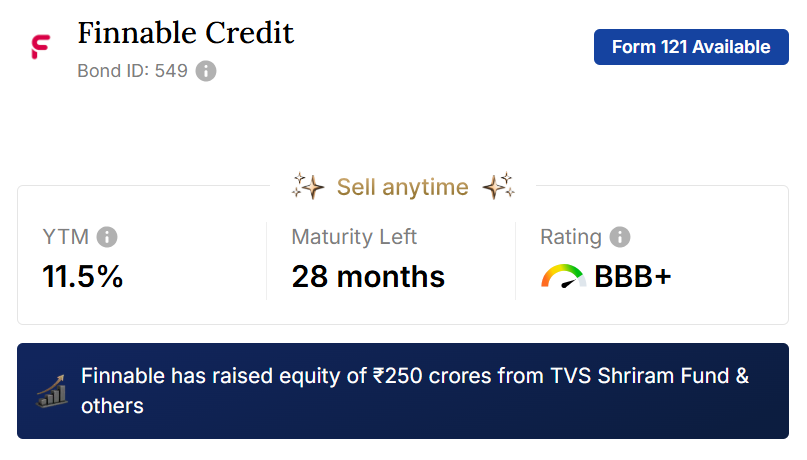

GoldenPi is one of the largest bond marketplaces in India with a massive inventory.

What I Observed

What I Observed

- Massive bond inventory (corporate bonds, SDLs, G-Secs, tax-free bonds)

- Wide range of yields (from safe to high-yield/risky)

- Minimum investment: ~₹10,000

- Account creation: Asks for your your existing Demat account number OR helps you open one

- Support quality: Good. Got prompt replies to my email queries.

What I Like

What I Like

- Huge selection — best in India

- Unmatched variety — you can actually build a diversified bond portfolio

- Better control over risk vs return

- Access to instruments not easily available elsewhere

Cons

Cons

- Can be overwhelming for beginners

- Requires understanding of credit risk

- Some bonds are high-risk/high-yield

![]() Verdict:

Verdict:

GoldenPi is like a stock exchange for bonds — powerful, but you need to know what you’re doing. It is for serious investors. If you know what you’re doing, it’s the most powerful platform in India right now.

Wint Wealth Review — Best for Beginners & Safety

Wint Wealth Review — Best for Beginners & Safety

Wint Wealth takes the opposite approach: curation over choice.

What I Observed

- Curated list of ~50–75 bonds

- Only Senior secured bonds

- Returns typically ~8–11%

- Minimum investment can be as low as ₹1,000–₹10,000

- You will get additional 0.25% return if you invest using within first 7 days.

- Account creation: Creates a new Demat account.

- Support quality: Good.

-

- They provide WhatsApp + Email support.

-

- Email: Got prompt replies to my email queries.

-

- WhatsApp : Response times on WhatsApp chat support was slow at times.

What I Like

- Beginner-friendly UI & explanations**

- Lower risk due to pre-screened bonds

- Predictable returns (FD alternative)

- Educational content is strong

Cons

- Limited bond selection

- Less flexibility in choosing risk/returns

- You don’t get access to the full bond market

- Slightly lower return potential compared to DIY platforms

![]() Verdict:

Verdict:

Wint Wealth feels like a “fixed deposit replacement with better returns”.

Grip Invest Review — Best for Alternative Fixed Income

Grip Invest Review — Best for Alternative Fixed Income

Grip Invest is slightly different — it started with lease financing & alternative assets before adding bonds.

What I Observed

- Offers:

- Corporate bonds

- Lease-backed investments

- Investment memos and detailed documentation

- Account creation: Usually uses your existing Demat (depends on product)

- Support Quality: Got prompt replies to my email queries

What I like

- Unique investment options beyond bonds

- Higher return opportunities

- Good documentation & transparency

Cons

- Some products carry higher risk

- Not purely a bond platform

- Past user concerns around defaults in certain assets (community feedback)

![]() Verdict:

Verdict:

Grip Invest is suitable if you want to experiment beyond traditional bonds, but it’s not my first choice for core fixed-income allocation.

Which One is the Best?

Which One is the Best?

Let’s be clear — there is no single “best” platform. It depends on your investing style:

Choose GoldenPi if:

Choose GoldenPi if:

- You want maximum options

- You understand credit risk & YTM

- You want to build a custom bond portfolio

Choose Wint Wealth if:

Choose Wint Wealth if:

- You are a beginner

- You want FD-like simplicity

- You prefer curated, safer options

Choose Grip Invest if:

Choose Grip Invest if:

- You want diversification beyond bonds

- You’re okay with slightly higher risk

- You want exposure to alternative fixed income

Final Verdict (Straight Answer)

Final Verdict (Straight Answer)

- Best Overall (Advanced Users): GoldenPi

- Best for Beginners: Wint Wealth

- Best for Diversification: Grip Invest

![]() If I had to recommend ONE for most people:

If I had to recommend ONE for most people:

![]() Start with Wint Wealth, then move to GoldenPi once you understand bonds better.

Start with Wint Wealth, then move to GoldenPi once you understand bonds better.

Important Reality Check

Important Reality Check

No matter which platform you choose:

- Bonds are not risk-free

- Higher yield = higher risk

- Always check:

- Credit rating

- Issuer financials

Closing Thought

Closing Thought

After 2 years of real investing experience:

- Bonds are one of the most underrated asset classes in India

- They sit perfectly between:

- Safety (FDs)

- Growth (stocks)

![]() If used properly, bonds can:

If used properly, bonds can:

- Stabilize your portfolio

- Generate steady income

- Improve risk-adjusted returns

Disclaimer:

This article is for informational purposes only and not investment advice.