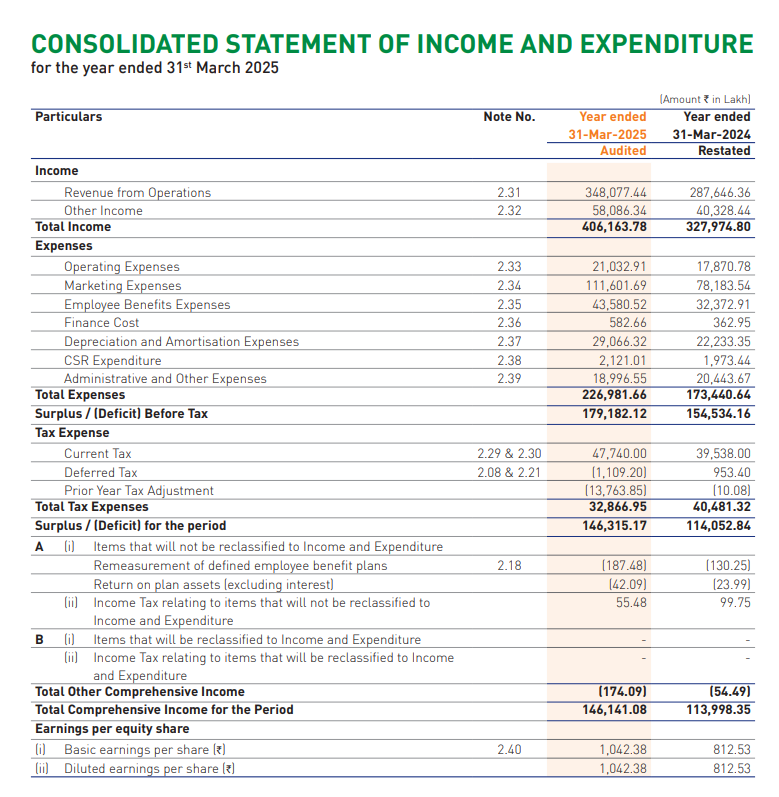

NPCI made ~₹1,500 crores in profits on ₹4,000 crores of revenue in 2024–25, with EBITDA margins above 50%. And they did this while spending just ₹210 crores on tech and another ₹290 crores in depreciation.

In other words, it costs just ₹500 crores to run the switch layer for UPI, IMPS, and NACH, which is basically the entire country’s payments infrastructure.

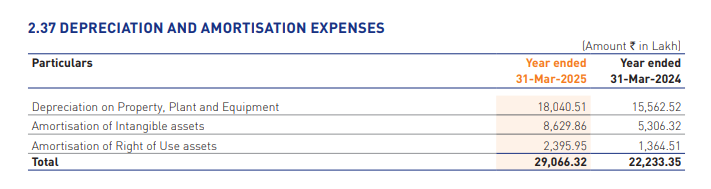

Depreciation on property, plant, and equipment was for about 180 crores and the rest was amortisation of software & asset use rights. I am assuming all of this contributed towards the cost of running the systems. Since outside these expenses, there are just admin, employee and marketing costs left.

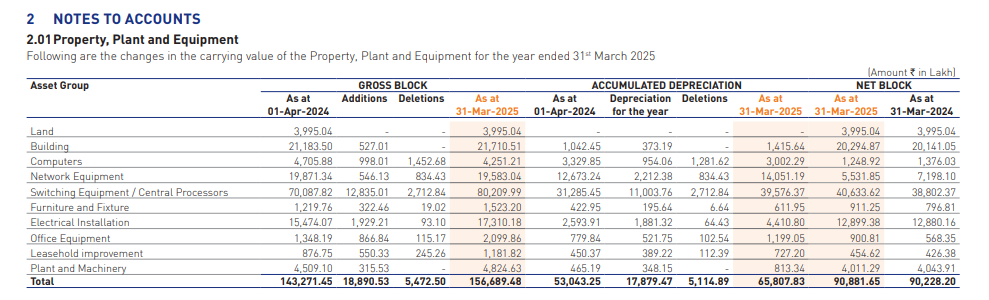

Also, here is a snapshot of the property, plant, and equipment. Out of the asset block of 1560 crores, 2/3rds is directly network equipment and switching equipment - used for payment infra. I am assuming the rest is ancillary to the equipment as well.

You can go through the complete financials here. Looks like free UPI forever is possible if all payment stakeholders have infrastructure as efficient as NPCI.

true, but also consider they’re the monopoly in this space. It’s less about efficiency and more about monopolisation of the retail payments system that allows them to, by policy design, be PAT (here, surplus) positive. Another network/entity like a NUE will considerably slash switching fee, etc making the payments system even more competitive in terms of pricing, innovation, etc. Nonetheless, NPCI has been at the helm of innovation and most importantly implementation of innovative payments system that we don’t see elsewhere in the world

i saw articles from many reputable websites last year, they mentioned that a bank has to bear around ₹1 cost per upi transaction and right now npci is bearing this cost and giving it as a subsidy to banks.

NPCI does not bear cost of bank. However govt does provide budgetary support to ensure zero MDR on UPI and to incetivise merchants. Last year support was for around 1500 cr

Kindly explain where the profits have come. UPI & NEFT are free; only IMPS transactions have a fee. Does that fee support both and still end up making a profit?

i was talking about this data. Acc to chat-gpt , india does around 6.5Million upi transactions in a day, so per day cost cost for npci for this 650million transaction as 40paisa per transaction = 26crores per day

so for a year of 365 days, total transaction cost for upi, npci has to bear around 9500Cr

These are free to end users not for partner banks.

NPCI does charge a fee to partner banks to register as ell as to transact.

Also, NPCI manages lot many things apart from what you mentioned like Rupay card network and Bharat Bill payment systems too, which generates revenue.

NEFT is run by RBI, not NPCI. Outside of the switching fee for various payment products [list below], NPCI also makes money from interest income from the deposits banks have to maintain for the UPI limits they have access to on a bank-wide level.

ok. But what’s the benefit to a bank when every transaction has a cost? And if I am not wrong, for every bank inflow must be equal or almost equal to outflow? The net is zero income, but loads of expenses with no indirect benefit either.

payments council of india says they need at least Rs 10,000 crore each year to sustain and further develop UPI at an ecosystem level, including banks and fintechs.

not really a speculation. I work with fintechs and that’s roughly what the cost comes down to. For larger fintechs, it can further go down to 10-20p. That said, can check for what the breakup looks like PSP-related costs, infra costs, development, switching fee, etc.

benefit? That is precisely the function of a bank to enable transactions

Bank build branches, builds ATM, provides cheque clearance, provides electric transaction facilities etc. Every one of these function has a cost and bank has to bear it.

These are enabler function which allows bank to operate and then earn money from various other functions (like lending, fees etc.)

In simple words, if bank doesn’t allow electric transfer, then people will be forced to issue cheques. Clearing a cheque has much larger cost to bank then what it pays for electric transaction OR worst, people start withdrawing cash for transaction (which has still higher cost)

And as other pointed out, bank are not completely happy with doing this for free and are pushing govt for some charges on UPI. But so far govt is not budging.

Here’s a news article that I came across on the “cost per UPI transaction”.

COST PER TRANSACTION

Industry experts estimate that banks now incur costs of 3-4 basis points per UPI transaction, including NPCI switching fees and technology service provider commissions. This represents a dramatic reduction from the 3-5 basis points per transaction that technology service providers charged in 2020, now dropping below 1 basis point.

With 213 billion transactions processed in FY2025, NPCI’s Rs 500 crore technology spend translates to approximately Rs 0.23 per transaction, an extraordinarily low cost for maintaining real-time payment infrastructure

Correct me if I’m wrong, i don’t think the math is right in the above calculation. It should be ₹0.023 paise, not ₹0.23 paise per transaction.

213 billion transactions equals 21,300 crore

So, if the total cost incurred by NPCI in relation to payments infrastructure (ignoring the costs incurred by banks) is ₹500 crore, the actual cost per transaction comes to (500/21300) = ₹0.023

The technology spends are not only for UPI. They also include services like IMPS, NACH, and Fastag. The costs attributable to UPI at NPCI’s end to support the UPI switch infra would be much lower. However, banks and UPI apps have their own costs too. Hopefully, if everyone is as efficient then the cost per transaction will actually be just a few paise.