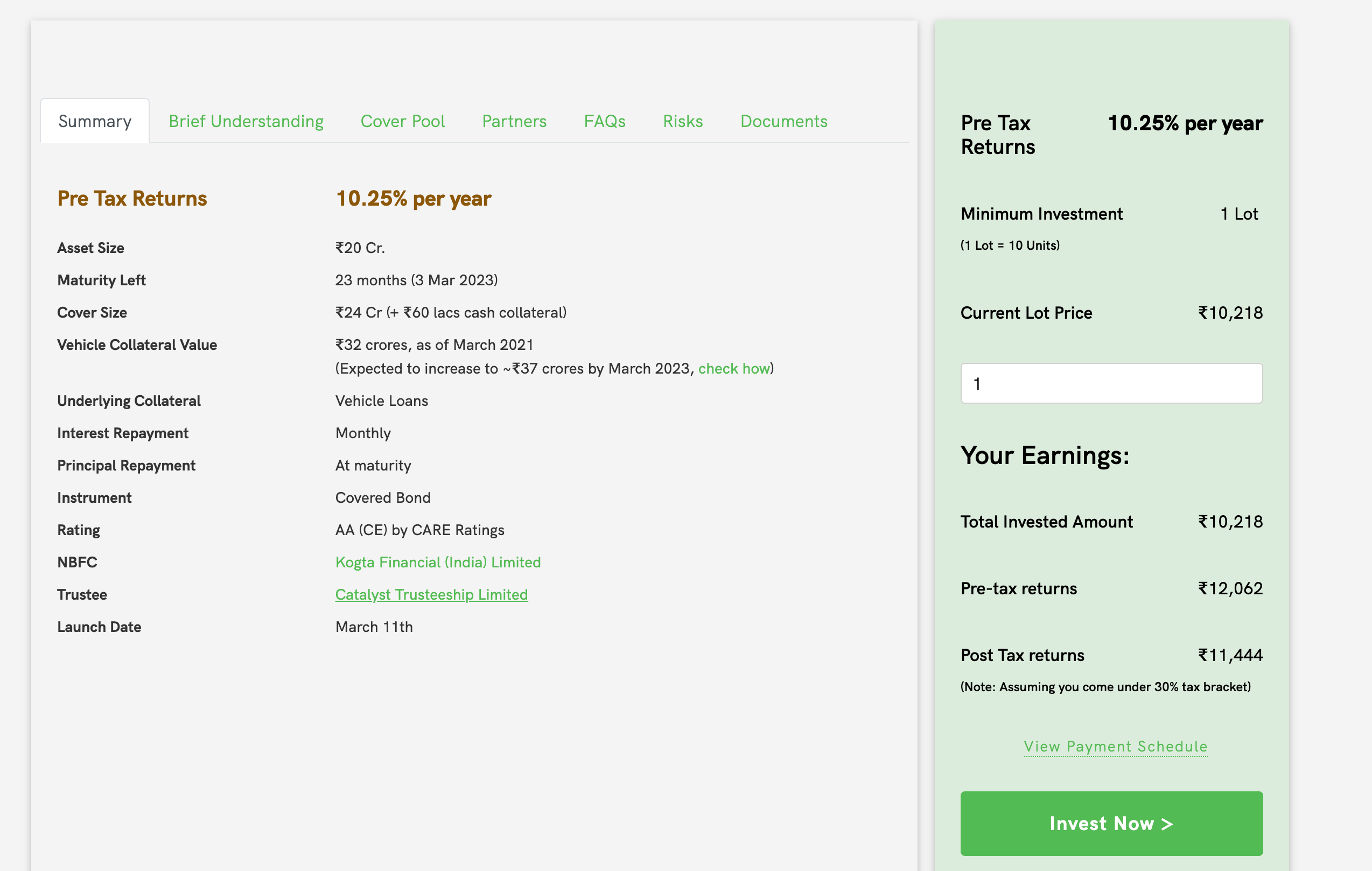

In covered bond the investor has dual recourse. Firstly on the issuer of the bond and Secondly on the underlying pool of assets.

The issuer is obligated to pay the interest and principal. In case the issuer has defaulted/gone bankrupt, the underlying pool of loans is used to repay the interest and principal.

Further, the issuer is also obligated to maintain the quality of the cover pool. For example, lets say a loan in the underlying has become NPA the issuer is obligated to top up the pool with a performing loan.

Covered Bond as a product came into India in early 2019 in which a mutual fund was an investor and incidentally the issuer was Kogta Finance itself (the same NBFC whose covered bond is live on WintWealth). Subsequently close to 5000 Cr worth of covered bonds have been placed in the market mostly with institutional investors and ultra HNIs.

Wint Wealth was started around six months back to democratise such products and enable retail investors to also access them. This is our third transaction. There hasn’t been any default in covered bonds till date.

7 to 8.5% ROI is offered in new vehicle financing segment which is typically offered by PSU and Private Banks (this segment goes upto ~12%). Also these rates are majorly offered in Urban areas.

In the case of Wint Wheels live asset, the NBFC Kogta Finance offers mostly used commercial vehicle loans. The rates in this segment is ~17% and above ROI. These customers are mostly from Tier2/Tier 3 geographies where banking penetration would be comparitively lower and the customers are catered to by NBFC sector.

The performance of this segment(especially LCV segment) has been good since these are commercial vehicles taken for income generation purposes.

@anshulgupta

Can we assume that an investor’s money is 100% secured in case of covered bonds and all of his Principal amount would be returned in case of things going wrong ?

this would be everyone’s question…is the principal safe? here the risk seems to be high as you are fully dependent on one bond vs debt mutual fund which has several securities. also, its difficult to understand the legal fine print as it gets too technical.

Hi,

Thanks for your query.

This is not a risk free product and definitely not a replacement for Fixed Deposits. The product is subject to credit and liquidity risks as detailed on the website. In case the NBFC defaults and there are significant losses in the underlying collateral pool, there may be a shortfall in principal and/or interest repayments.

Happy to get on a call to explain the risks in more detail.

You are right. We also recommend the investors to diversify their exposure across Wint deals (we are trying to bring one asset per month on our platform) and to not allocate significant portion of portfolio in just one asset. In future we do plan to bring pooled products as well where in a single deal investors would be able to diversify their exposures across assets.

Happy to get on a call to discuss the technicalities of the product covering risks and how the same are mitigated.

@anshulgupta I was following Wint Wealth after reading this post and finally invested some money in Wint Bricks May 21. After making the investment, I got the bonds and I was really surprised at way Wint Wealth is masking information from investors.

Something which really annoyed me:

Wint Wealth website says Maturity for these bonds as 25-Nov-22

But the actual NCD indicates maturity as 25-Nov-29 with call option to company at 25-Nov-22

Nowhere I could find this on Wint website before making investment. Basically you are selling investor a 8.5 years bond claiming it to be 1.5 years product.

What happens if company determines not to exercise call option. Both my principal and interest gets locked up for 8.5 years?

Don’t you think investor should know these details beforehand???

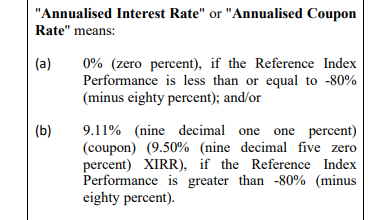

Nowhere on Wint website could I find actual interest rate for product. Website keeps harping 9.5% XIRR. But what is actual intrest rate on bond?

Again original product documentation clearly mentions it as 9.11%

For a company which is backed by zerodha and @nithin , these are some real shady practices to use.

Their website says, interest will be paid on maturity - does this mean you need to wait until 25.11.29 or 25.11.2022 to get the interest.

Is this normal, I thought in any NCD (normal ones - not these type) there are different types of interest payments.

Also like to know if possible the following for my info

who the trustee are who is holding the securities on behalf of investors. Are these properties registered in the trustee name.

Do they tell you when the properties were valued and date of valuation and who the valuators are. They have mentioned an amount of 100 crores? It means nothing. It is like saying financials are audited without auditors name and date and audit report

3 Do they give you a break up of the security they they hold once you have invested.

What is the role of Wint Wealth - are they brokers and walk out after the deal - do they have any skin in the game.

There seems to be some misunderstanding. I will try to clear both the queries below:

Tenor of the bond:

The issuer is suppose to make the payment at the end of eighteen months only. If the issuer fails to pay at the end of eighteen months it results into a credit event and the collections from the pool will be utilized to make the repayments. Amongst other things (like right to appoint nominee director etc), consequence of this will be that coupon rate would increase to 13.5% for the investors.

The last rupee from the entire set of pool is expected to come by eight years, however we only need to recover 20Cr of principal along with interest which is expected to recover by ~50 months ( the difference is because the pool amount is much higher than bond amount and pool has lot of interest cashflows which also would be used to repay the investors in this scenario). Further trustee will also try to find a buyer (some other NBFC, bank etc) for the underlying pool in which case investors may not even have to wait till ~50 months and may get the repayments in just few months.

These consequences are mentioned in the documents and also on the website (relevant portion from website pasted below for easy reference).

The legal final tenor of the bond is mentioned as 2029 because that when the last rupee from the pool is suppose to come, but issuer is suppose to pay after 18 months only failing which above consequences get initiated.

The returns on the bonds are 9.50% as mentioned in the documents and also mentioned on the website. (9.11% figure is monthly coupon equivalent returns for 9.50% XIRR).

Website also clearly mentions that 9.50% are XIRR returns (please refer below)

@anshulgupta : Thanks for the Info , i have few other questions as well

1 After the Bonds comes to the Demat account , can we sell in open market these bonds before maturity?

2. Can we buy the same bond from open market and are these bonds covered bonds from open market as well? or Bonds are only covered when bought via Wint wealth.

3. Also do we have to do anything (like accepting the call etc on maturity 25.11.2022) or Maturity amount will directly be credited in the bank (no actions required by investor)?

Anshul, thanks for calling and discussing the issue, While I understand your explanation, I believe disclosures could have been better to avoid confusion.

Appreciate you clearing the air.

Thanks for the queries, please find below reverts:

Yes the bonds can be sold in market. However the liquidity of the bonds is very low, so please do invest with the intention to hold till maturity.

These are bonds structured by Wint Wealth so may not be available in the market (unless some existing investor is looking to sell their bonds in secondary markets)

Maturity amount would be directly credited in the bank accounts of the investors. There is no action required on part of investors.