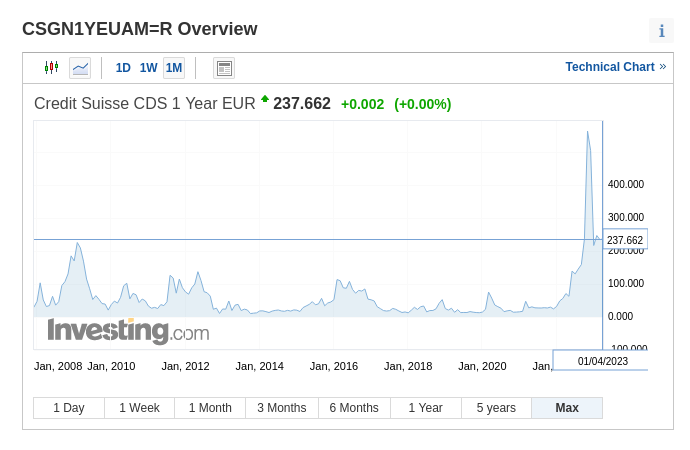

Credit Default Swaps on Credit Suisse broke even the infamous 2008 levels [see image]

You may have heard about CDS, bond defaults, and the Credit Suisse episode recently. Here’s a simple breakdown @mohitmehra & I drafted of how these swaps work,

Suppose a company sold a $100 bond with a 10-year maturity. The bond buyer faces credit risk if the company goes bankrupt. They can buy a CDS to transfer the risk to another investor. The CDS buyer agrees to pay if the company defaults.

Credit Suisse bond holders had to pay 2.7 cents per dollar for buying swaps to insure their investment a year. If there’s no default, the CDS seller pockets this neat premium. But if there’s a default, the CDS seller pays $100 plus coupons.

Swaps are infamous for the 2008 financial crisis - banks all over the world bought CDS protection from AIG. In 2008, AIG was not able to make good on that promise of payment without a Govt bailout. As a result, until the bailout was announced, every one of those banks lost that protection. The lack of liquid cash or liquidity failed these companies.

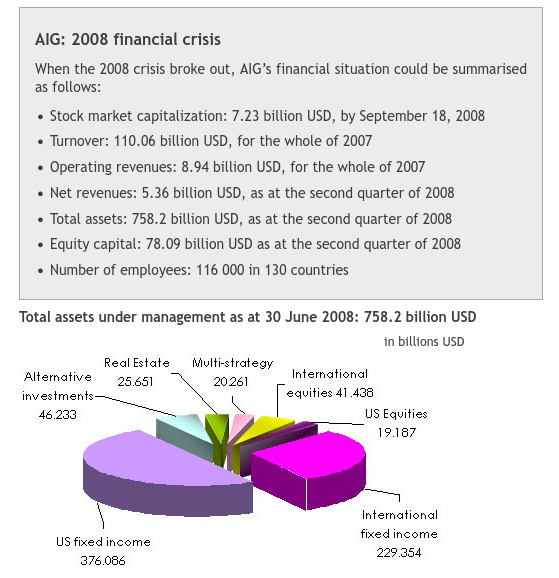

AIG was a global company with about $1 trillion in assets prior to 2008. But during the financial crisis of 2008, AIG lost $99.2 billion. The company’s Credit Default Swaps caused the collapse. It ended up costing AIG $30 billion. Finally, Federal Reserve had to bail out AIG.

There wasnt anything interesting about the assets. AIG had written credit default swaps on over $500 billion in assets. But it was the $78 billion in credit default swaps on multi-sector collateralized debt obligations—a security backed by debt payments from residential and commercial mortgages, home equity loans, and more—that proved most troublesome. AIG’s problems were exacerbated by the fact that these were one-way bets. AIG didn’t have any offsetting positions that would make money if its swaps in this sector lost money.

They mentioned credit market deterioration and charges related to restructuring activities contributed to the loss - mostly arising from the financial crisis and CDS defaults. Specifically, about $7 billion was attributed to restructuring costs; $26 billion to market disruption items including a steep decline in commercial mortgage backed securities; $25 billion in accounting costs; and $7 billion in amortization and credit charges for govermment credit facilities.