Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Cult.fit’s IPO promises to lift heavier weights, but can it?

- How AI is eating the web that feeds it

Cult.fit’s IPO promises to lift heavier weights, but can it?

For most of its life, Cult.fit has worn a convenient label of being “fitness-tech”. It’s an app with lots of data about customers and even an AI that decides where to open the next gym apparently. Maybe “omni-channel fitness platform” is a better description?

But labels aren’t all that useful in understanding nuances of running and understanding a business.

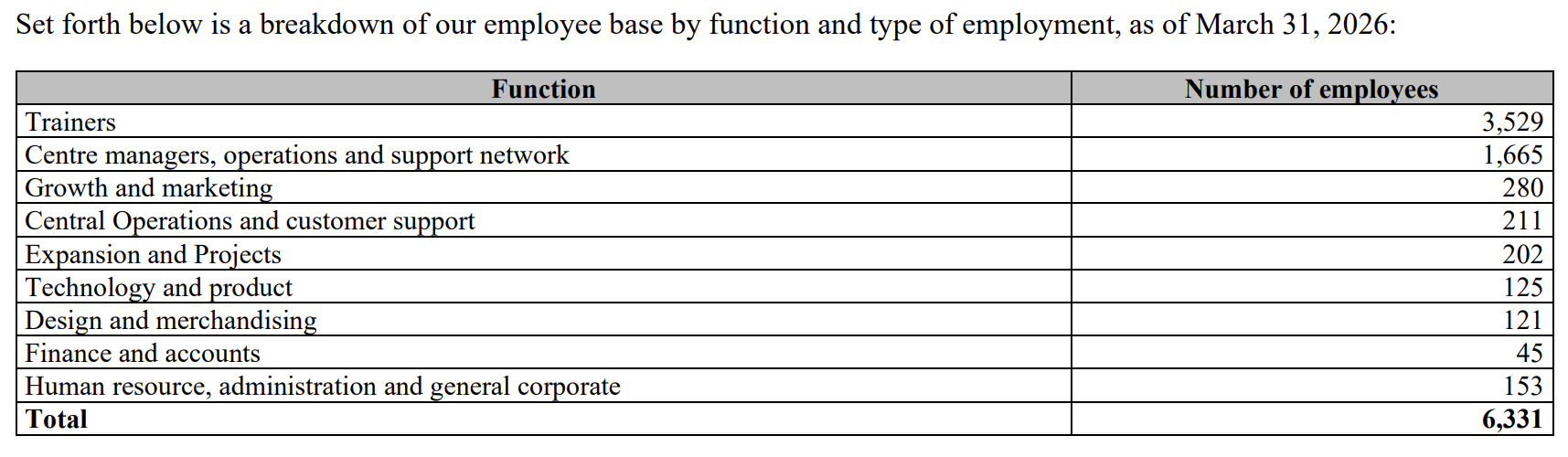

So, here’s a number that cuts through this one. As of March 2026, Cult.fit employed 6,331 people. Of them, 3,529 were trainers and another 1,665 ran its centres. The number working in technology and product was just 125.

That ratio is the company. Cult.fit is clearly a gyms business with some software bolted on with a physical operation of leases, trainers, floor space and treadmills. It makes Cult.fit a more interesting company to understand because a brick-and-mortar business has brick-and-mortar economics: rent, utilisation, footfall, whether people actually show up. The app layer, meanwhile, affects all these things in weird but intuitive ways.

So instead of asking whether the IPO is cheap or dear, let’s do something more useful. Let’s understand the business from the floor up, and ask the questions that decide whether it works.

Two businesses, and one of them does the work

Cult.fit is really two companies under one brand.

The first is fitness services subscription with gym access, group classes, personal training, sports, at-home workouts, sold mostly through CultPass memberships. In FY26, this brought in about ₹1,198 crore, or roughly 70% of revenue.

The second is products like activewear, footwear, treadmills, massagers, accessories, sold through its own stores, its app, or e-commerce marketplaces. That was about ₹523 crore.

Obviously, services is the more predictable business: members pay upfront, come back (ideally), and can be upsold over time. The product side is closer to a retail operation stitched onto a fitness brand.

This IPO is primarily a bet on the services engine. The company might have you believe that you are buying the whole “integrated ecosystem,” but the ecosystem as a whole still has much left to prove. We’ll get back to this eventually.

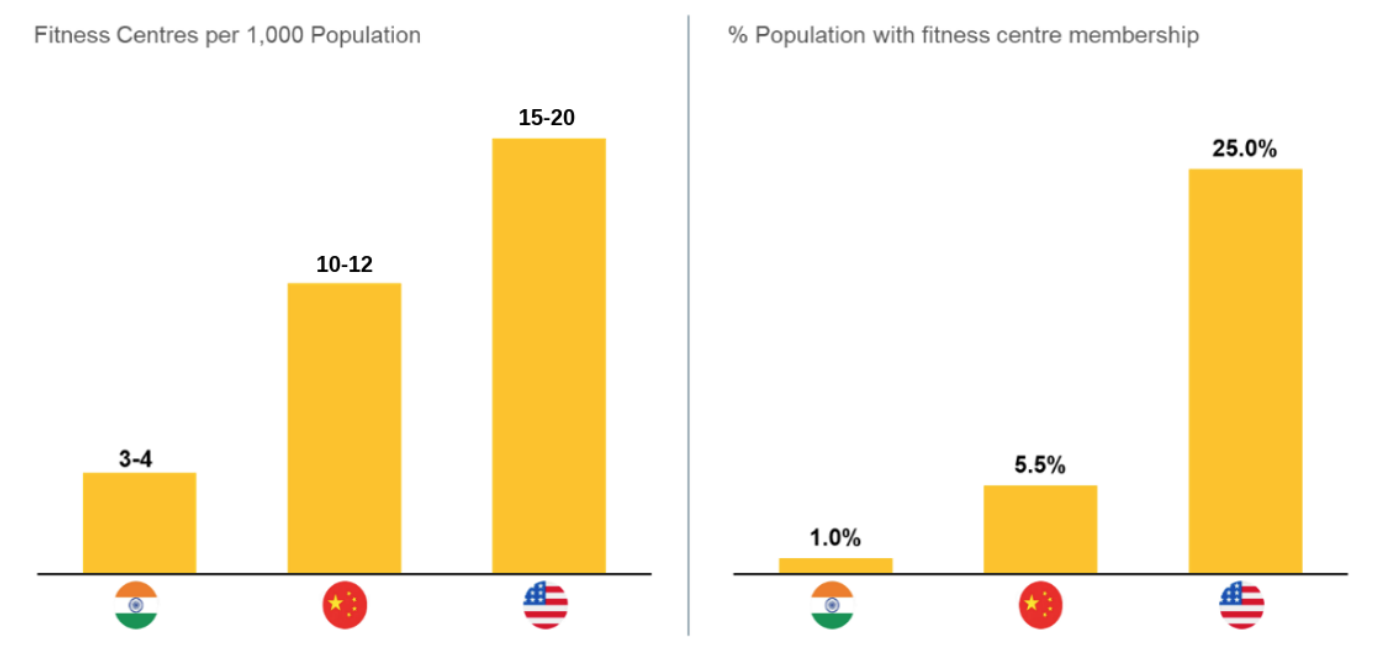

The setting, at least, is promising. India’s organised fitness market, which includes branded gyms rather than neighbourhood setups, is estimated at only about 12% of the fitness-services market, and expected to reach 17-19% by 2030. Fitness-centre membership runs to roughly 1% of the population.

What remains to be answered is whether Cult.fit can gain the most from the potential that exists. More existentially, does India even go down this trajectory in the first place?

Repeat business

Every gym membership is a small bet against human nature. People sign up in January full of intent, only for disappointment to set in a few months later, and the treadmills empty out by April.

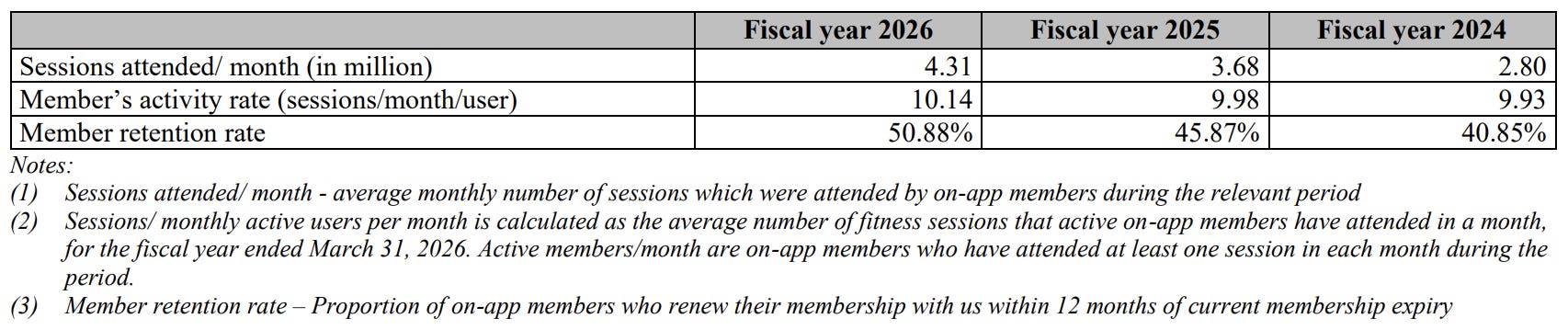

So an important number in this business is whether members renew. It’s easier to get the existing, already-fit customers to stay, than actually finding new people who want to get fit. And these renewals are what makes a subscription model viable.

Here, Cult.fit has an improving story. Its retention rate climbed from ~41% in FY24 to ~51% in FY26. That’s progress, but hard to describe in absolute terms of it being good or bad. We can read it the other way too, roughly half its members don’t renew. It might be better than a typical local gym, but a long way from the stickiness of a software subscription.

What makes the improvement believable is where it’s coming from. Marketing spend, which is what a business would burn to keep replacing the members it loses, has fallen sharply from ~20% of revenue in FY24 to 10% in FY26. Over the same stretch, ~39% of new paid members came in through referrals. That’s an encouraging signal that the brand needs less paid ads to build a reputation.

Personal training also points the same way. It grew 73% in a single year, to ₹122 crore, and is now a tenth of services revenue. That’s a company deepening its grip on existing customers, rather than endlessly chasing new ones.

But it’s far more difficult to say this is evidence of large-scale habit formation. Cult.fit doesn’t disclose what share of paid members are active in a given month, or how a batch of members who joined in 2024 behaves two or three years on. Those are the numbers that would settle stickiness.

Asset-light, but blame-heavy

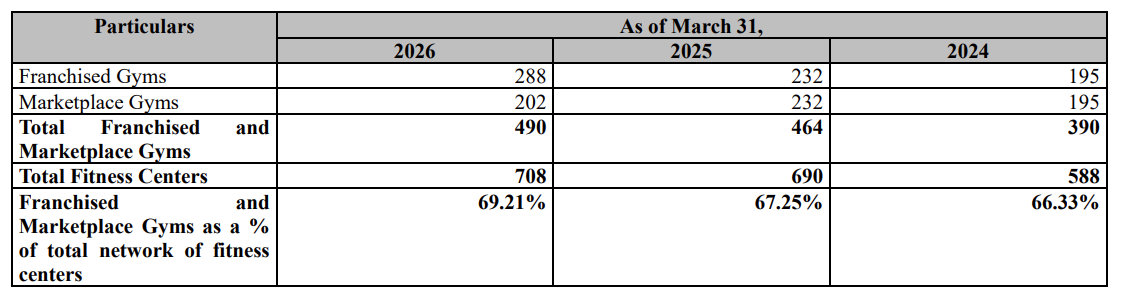

Now, Cult runs its gyms in three different ways.

Of its 708 centres, only about 218 are gyms. Cult pays to build and fills payroll itself, carrying the full cost but keeping the most control and the biggest share of the money.

The other 490 centres (nearly 69%) come in two lighter forms. The first is a franchise centre, which is built with a partner’s capital but run by Cult under its own brand, systems and trainers, with the two sides splitting the revenue. Then, there’s the lighter marketplace gym, which Cult neither builds nor staffs. But this gym is simply plugged into the CultPass app so members can walk in, with Cult paying the operator for each member it sends over. In FY26, over three-quarters of new centres came through these two asset-light routes.

From a cost standpoint, the appeal of building more asset-light gyms sounds obvious, but so is the trade-off. The further it moves towards being asset-light, the more of every rupee it has to hand a partner, and the less say it keeps over what actually happens on the floor. Across its franchise and marketplace centres together, 64% of the revenue goes to their actual owners to services Cult members. Being asset-light isn’t free.

But beyond actual cash, Cult also makes a sacrifice on brand control. See, when a member walks into a grubby, overcrowded, badly-staffed gym, they don’t blame the franchise partner. They blame Cult.fit. The more Cult leans on partners to grow, the harder its audits and app-based monitoring have to work to keep the experience consistent across hundreds of locations it doesn’t fully own.

A national company that lives in four cities

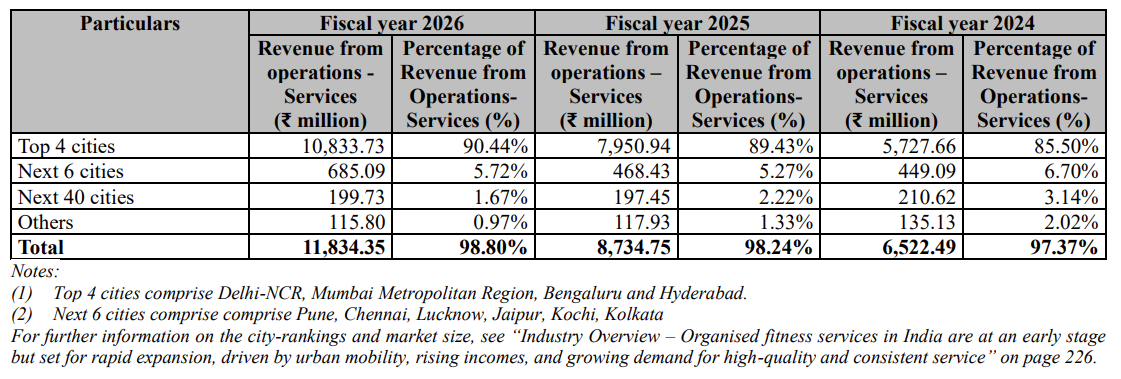

Cult.fit calls itself India’s largest fitness brand, and by centre count, it is — more than four times the size of the next player.

But “national” needs an asterisk . Just four cities brought it ~90% of its fitness-centre revenue, and that concentration has only risen, not fallen, from 85.5% two years earlier. Bengaluru alone runs 247 centres and occupies over 30% share of the city’s gym market. It’s a company dominant in a handful of metros and thin almost everywhere else. Nationally, its share of the fitness-services market is just 4-6%.

Those four cities are only about 40-42% of India’s fitness-services market but the other 58-60% sits in cities where Cult barely earns anything today.

Cult wants to expand across the top 100 cities, led by two formats: Cult Elite, its hybrid gym-plus-classes format, and Cult Neo, a leaner, value-focused gym aimed squarely at the price-conscious mass market that makes up the bulk of Indian fitness demand. On paper, Neo is the right weapon for smaller cities.

But that’s exactly the bet that’s unproven. The economics that work in high dense cities with higher incomes and people willing to pay for a premium format may not survive the trip to a Tier-2 city with lower willingness to pay and thinner trainer supply. Whether the model travels is the difference between Cult.fit being a very good metro business and a genuinely national one.

The products puzzle

Now, we come to the other business.

The product pitch is seductive for a fitness brand with a million members. Effectively, Cult has access to tons of workout data that should be able to sell their customers shoes and apparel more cheaply and cleverly than a direct-to-consumer (D2C) label. And, to a degree, that’s happening, with product sales growing 60% in FY26.

But look closer and the “ecosystem “ gets blurry. The products segment still loses money . Only about a quarter of product sales come through Cult’s own stores and apps, while ~39% run through third-party marketplaces. Only ~32% of product revenue comes from people who were fitness members, showing that the cross-sell flywheel story is not as strong. Meanwhile, the number of distinct products it stocks has doubled.

All of this changes the economics of the overall business. On one hand, you have a subscription platform. But that has mixed with the messy working capital cycles that consumer retail demands. Apparel and footwear are brutally competitive categories where incumbents like Decathlon, Nike and Adidas roam.

The money question

Lastly, we get down to the bottom line.

Cult.fit’s adjusted EBITDA in FY26 finally turned positive at ₹145 crore — less than 10% of revenue. That reads like a turning point, but a good chunk of that figure is one-off gains and accounting add-backs, not money earned from running gyms. Minus those, the real operating margin is wafer-thin. And once every cost is counted, Cult.fit still lost ₹252 crore for the year.

With cash-flow, Cult.fit had both a milestone and a catch. For the first time, after years of burning it, Cult.fit’s day-to-day operations actually generated positive cash of ~₹94 crore in FY26. But it then spent more than that building new gyms and paying rent on the old ones. That shows up on the balance sheet with nearly ₹900 crore of lease commitments.

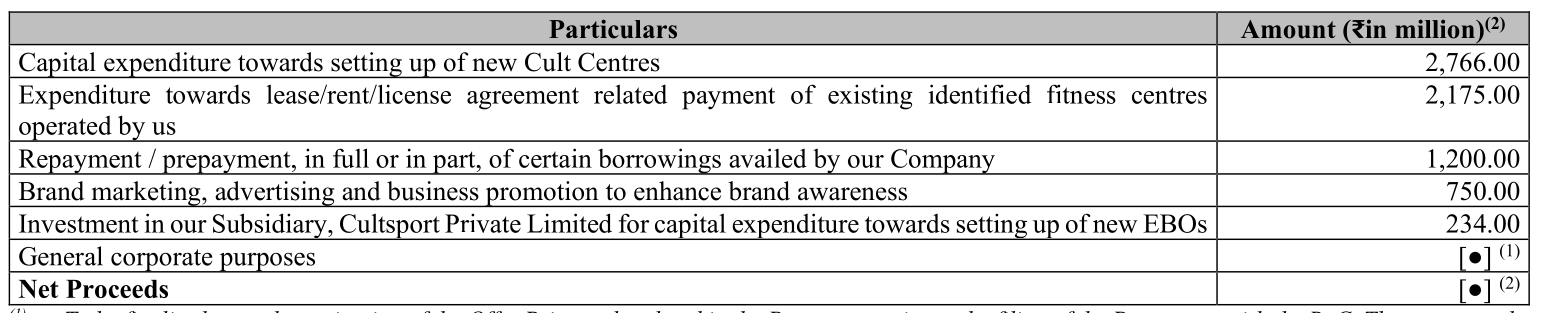

Which brings us to the IPO. Cult is raising ₹950 crore in fresh capital. Existing investors are also selling a large block of shares in a parallel “offer for sale”, from which the company itself keeps nothing.

The single largest use of the raise will be building more physical gyms. The second largest is paying rent on gyms it already runs. And the loans it wants to clear were themselves taken out to open gyms. Put those three together and roughly two-thirds of the fresh capital — about ₹614 crore — is going into physical floor space, its rent, and the debt raised to build it.

What’s also worth noting is that the company hasn’t yet picked the locations for its new gyms or signed final deals with vendors. So these are estimates to be deployed over three years to 2030, not shovel-ready projects.

What you’re actually deciding

Cult.fit is a real business that has gotten meaningfully better by growing fast, churning less, spending less to win customers, finally throwing off operating cash. None of that is hype. The services engine, in its core cities, is a good business.

But the leap the IPO asks you to make is that it will go from a strong metro fitness operator to a more national player, which also manages to make money selling physical products.

The answer to that lies behind a lot of tough questions. Does the model work outside four cities? How fast do centres become profitable at standalone level? Does the product business make profit, or just add to the revenue? Does adjusted EBITDA ever turn into real cash after the rent is paid?

A growing fitness market may not necessarily answer those, either. A rising tide floats new gyms, new D2C brands and the trainer down the road just as easily as it floats Cult.fit.

How AI is eating the web that feeds it

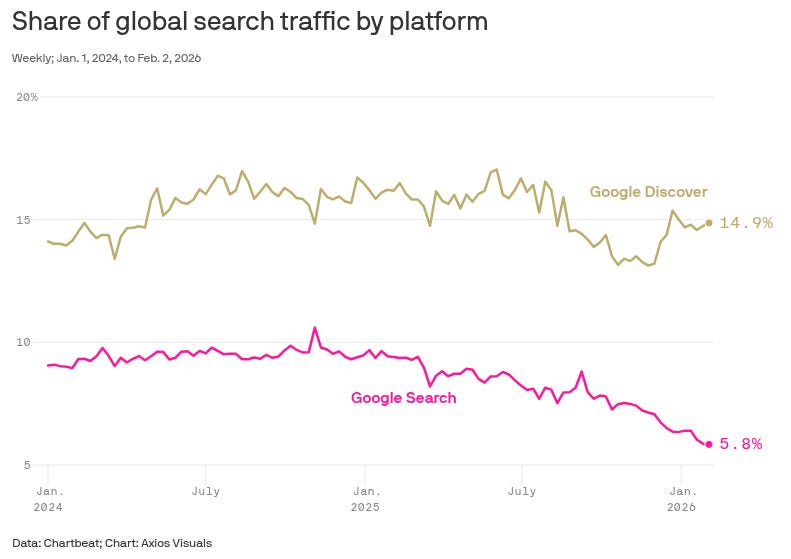

As per Axios, between 2023 and 2025, Google Search referral traffic to small publishers, which get between 1,000 and 10,000 daily pageviews, fell by 60% , while medium publishers lost 47%. Even the large ones, with over 1 lakh daily views, saw a 22% drop. At the same time, traffic from AI chatbots still accounts for less than 1% of all publisher page-views.

Everywhere you look, websites themselves are generating less traffic. Even when a chatGPT or Gemini throws up an answer to your query, you’re not likely to click on the link that was the source of truth for what the LLM spewed out.

A new paper by Harvard economist Alex Chan looks exactly into this problem and formalizes it in a mathematical model. It doesn’t assume bad actors, nor does it need misinformation, irrational users, or even hallucinatory AI answers. All it looks at is how AI has changed the viability of the contract under which content on the old web used to work.

The bargain that built the web

So, what did the old internet look like?

The open web, which was built on shared standards like HTML and HTTP, where anyone can publish, has always run on a basic bargain. Publishers produce content, and search engines and social platforms send users to that content.

Those visits do two things. First, they generate revenue through ads, subscriptions, affiliate links, and so on. Second, they generate information about the value and trustworthiness of the publisher . When a user clicks, returns, subscribes, bookmarks, shares, or links to a page, they’re leaving behind signals about its quality. Future users and search engines use those signals to find good sources.

These are the two pillars of the open web’s economic loop. And AI answer systems are pulling both of them away from publishers at the same time.

When you ask Claude a question, the AI reads publisher content, synthesises an answer, and serves it to you at the AI interface. You got your answer, but most likely, the publisher lost a visit because you didn’t check the source.

Now, multiply that across billions of queries a day. A Pew Research study found that when Google’s AI overviews appear at the top of search results, just 1% of users click on the cited links. Without AI overviews, 15% of users click the organic links below. With them, that drops to 8%. The AI answer is absorbing the attention that used to flow to the sources.

Catch-22

On one front, assuming that AI’s answer is always correct (which it isn’t), one could say that with AI answers, the user has been served their immediate needs much faster. They don’t have to do tons of searching anymore.

But Chan’s paper argues that this view misunderstands the true impact of LLM-generated content. The AI answer is consuming costly human information without paying at all for its reproduction.

If AI scrapes the work of, say, a finance newspaper for free, what incentive does that leave the owners and employees of that newspaper to publish? Their work involves a lot of scarce inputs: reporting, testing, judgment, verification, observation, real fieldwork, and so on. All of that has value, and therefore a high cost compared to other forms of content.

Any such human information, be it a deeply reported investigative story, a maintained technical database, or even a niche expert forum, does more than merely generate immediate traffic. It also creates durable assets, like backlinks, search authority and reputation. All of these assets are attention which can potentially be turned into more revenue.

But these assets also have their own shelf-life. After all, subscribers can churn, links often go stale, and bookmarks gather dust. If the content isn’t refreshed and reproduced, these assets eventually wither with no viable replacement.

Chan formalises all of this into what he calls the “open-web reproduction number” , or R-web . The mathematical construction of R-web is extremely complicated even for us to grasp fully, but in simple terms, it is determined broadly by three factors:

- The traffic share that actually reaches publishers (T)

- The strength of its existing body of content on the web (N) — this itself is determined independently of T, by factors such as how much revenue per visit a publisher can make, the behavior of users in the old web, and attention built through assets

- The rate at which old content turns stale (S).

Expressed in simple math terms, R-web checks for one condition: “T x N > S”.

If this condition holds, the system sustains itself; meaning, each generation of costly content generates enough attention, which in turn can result in more monetization, and therefore a higher ability to fund new content. However, if it doesn’t, that feedback loop basically ceases to exist, the knowledge base contracts, and eventually, it collapses.

This condition can fail across individual publishers, but on average, it would still hold true as a way of how the open-web works. But as per the paper, AI puts this entire equation in an existential crisis, with failure being the default mode.

AI lowers the T variable, since publishers get much less visits. T is also hurt by what Chan calls “genuine-source visibility “, which refers to how well search engines surface real, original sources amid a rising tide of synthetic content. We’ll come to this as well.

The extent of monetisation a publisher can resort to is the product of these two forces. You don’t need full AI diversion to collapse the system. Even a moderate level of answer diversion, combined with polluted search results, can do the job. Even if N is high in the short-term, the fall in T alone is substantial. Over the long-term, N also falls because of lower T.

Slop begets slop

While AI collapses the demand for high-value sources, it also floods the supply side with cheap AI-generated content.

An Ahrefs study of 9 lakh newly-created web pages in April 2025 found that roughly three-quarters contained detectable AI-generated content. Automated traffic via bots now exceeds human traffic on the web .

Chan calls this the “abundance paradox “. The web can get bigger in raw page count while getting thinner in actual knowledge. More pages and URLs, but fewer facts, and less valuable writing or journalism. And each of those pages increasingly refer back to other AI-generated pages.

This also degrades the search systems that everyone (including AI models) relies on. After all, the original insight behind the PageRank algorithm that defined Google Search was that hyperlinks are decentralised quality signals.

When a real person reads something and links to it, that link encodes information about trust. People rely on Bloomberg or Reuters because they’ve established themselves as authoritative finance news outlets, and therefore get backlinked and bookmarked often. But when cheap synthetic pages flood the web with their own link structures, those signals get diluted. If synthetic pages dominate the web’s link graph, and they reference each other more, the PageRank mass on genuine pages converges to zero .

Then, Google’s ranking of pages becomes a measure of who can produce the most content cheaply, not who has the best information. And since AI models are trained on web content and rely on retrieval systems to stay current, this degradation feeds back into AI quality itself. That is what the peak of the wave of AI slop looks like*.*

When we zoom out from each step in this chain, we get to a self-reinforcing spiral.

It starts with AI answers diverting traffic from publishers, as a result of which publishers earn less revenue and produce less costly content. With less fresh content, search engines have fewer genuine signals to work with and search quality deteriorates. Users notice that search results are getting worse and shift further toward AI answers. That raises AI diversion further, which removes more visits and links, which degrades search quality more, until publishers get no monetizable traffic to themselves.

This sounds like a fully-abstract concern, but the signs of this spiral manifesting itself, even if partly, are already here. Media executives surveyed by the Reuters Institute in early 2026 expect search engine traffic to fall by 43% within three years. Many publishers now plan to reduce investment in traditional SEO. Publishers are already adapting by filing lawsuits, negotiating licensing deals, and blocking AI crawlers.

The fix

Chan’s paper also provides solutions to this problem.

First, if an AI answer satisfies a query that would have driven a publisher visit, someone needs to pay the publisher what that visit was worth. Chan calls this a “visitor-replacement royalty “. If the AI diverts 40% of a publisher’s monetisable traffic, and the publisher would have earned ₹100 per visit, the royalty is ₹40 per diverted query.

Secondly, even if you pay publishers, you still need to distinguish costly human information from cheap AI imitations. If an AI platform pays for “quality”, but can’t tell the difference between a meticulously fact-checked original piece and AI slop, that effectively creates a subsidy for slop content that AI platforms eventually gravitate toward to reduce costs.

As per Chan, the audit system needs to be informative enough to overcome the cost advantage of imitation. One example of an attempt at building such an audit system is Pangram, the AI writing detector. Another is Google’s SynthID, which watermarks AI-generated content.

Third, compensation shouldn’t be allocated by clicks alone. There are some “keystone topics “ which incur the highest fixed costs, but often the lowest direct click monetisation. That could be a research paper (like this one), local news, niche technical databases, or even public-interest investigations. Few people read them, but those who do, reference them as their source of truth in blogs (like we are right now). These are the topics whose loss would do the most damage to the web.

Finally, Chan proposes a market clearinghouse where AI platforms, publishers, auditors, and even regulators can measure displaced visits, verify provenance, run audits, and settle payments.

Conclusion

The market is already groping toward partial solutions. OpenAI has signed licensing deals with roughly 20 publisher groups covering over 160 outlets. The UK’s Competition and Markets Authority also imposed regulations in June 2026 requiring Google to give publishers opt-out controls over AI search features.

But licensing deals with a handful of large publishers could create a two-tier web where major outlets get paid, while the long tail of local, niche, and independent sources keep losing traffic with no compensation. It raises questions about the very nature of text as a medium of expression, a far cry from an era where self-hosted blogs had become so commonplace.

A magazine like The New York Times has enough capital to survive. But a lot of smaller sources, or even academic journals, which are far smaller, but collectively make the web worth searching cannot keep going without the market design adequately reflecting what AI is doing to the web.

Tibits

1. Government waives import duty on battery and display manufacturing inputs

The government has exempted customs duty on 85 capital goods used in lithium-ion cell manufacturing and key inputs for display assemblies and wireless charging modules until March 2029. The move aims to lower manufacturing costs and boost domestic electronics and battery production.

Source: The Indian Express

2. TCS posts strong Q1 as AI business crosses $2.6 billion run rate

TCS reported a 4.7% rise in Q1 net profit to ₹13,420 crore and a 14% increase in revenue to ₹72,275 crore. The company secured $9.5 billion in new orders, while its annualised AI revenue run rate crossed $2.6 billion, reflecting growing enterprise spending on AI-led transformation.

Source: The Hindu BusinessLine

3. Dr. Reddy’s halts semaglutide supplies over quality concerns

Dr. Reddy’s has temporarily halted commercial supplies of its generic semaglutide after detecting a quality issue linked to the drug’s active ingredient. The company said there is no impact on patient safety, but fresh supplies are expected to resume only by late October or early November.

Source: The Hindu

- This edition of the newsletter was written by Kashish & Manie.

Points & Figures by Zerodha

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s retail lending landscape has transformed, using credit bureau data to reveal why lenders are moving away from unsecured loans and betting increasingly on collateral-backed credit.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

The Chatter by Zerodha

Our team at Markets spends a lot of time reading earnings call transcripts and listening to management interviews. Along the way, we come across plenty of interesting insights that are worth sharing.

That’s what The Chatter is for.

It’s a weekly newsletter where we dig through what India’s biggest companies are saying and bring you the most interesting insights into businesses, industries, and the wider economy.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops so that you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()