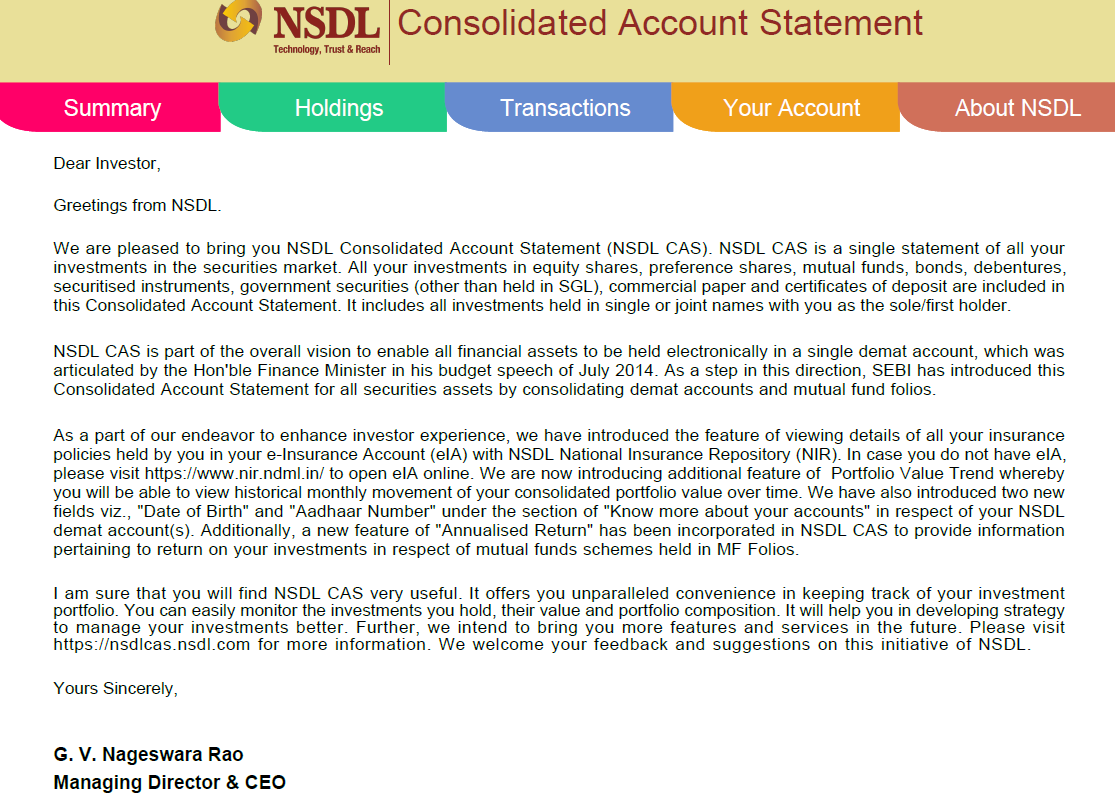

A good friend of mine recently received a 10-page ‘Consolidated Account Statement’ (CAS), from NSDL via email. For those of you who are not familiar with CAS, check this FAQs.

My friend was not sure how to read and make sense of this report, so he asked if I could help me read through his statement and help him understand the details better. So we sat together and dug into the report.

As expected, the CAS contained all the details of the transactions he had done in the securities market over the last financial year. This included transactions across stocks, bonds, government securities, corporate bonds, and mutual funds. The report was quite straightforward to understand. Just when I was about to close it, the section under his mutual fund investment caught my attention.

Unfortunately, this friend of mine still continues to invest in Regular Mutual Funds via his agent, despite me giving him all the gyan! Anyway, that’s another story for another day ![]()

The CAS report very promptly reports the commissions his agent earns by all the investments my friend makes every month, and the commissions were not small! To set the context my friend makes an investment of Rs.40,000/- every month split across 6 different mutual funds.

With his permission, I’m posting screenshots of certain sections of his CAS statements, hopefully, this should convince you why direct is a much better option than regular!

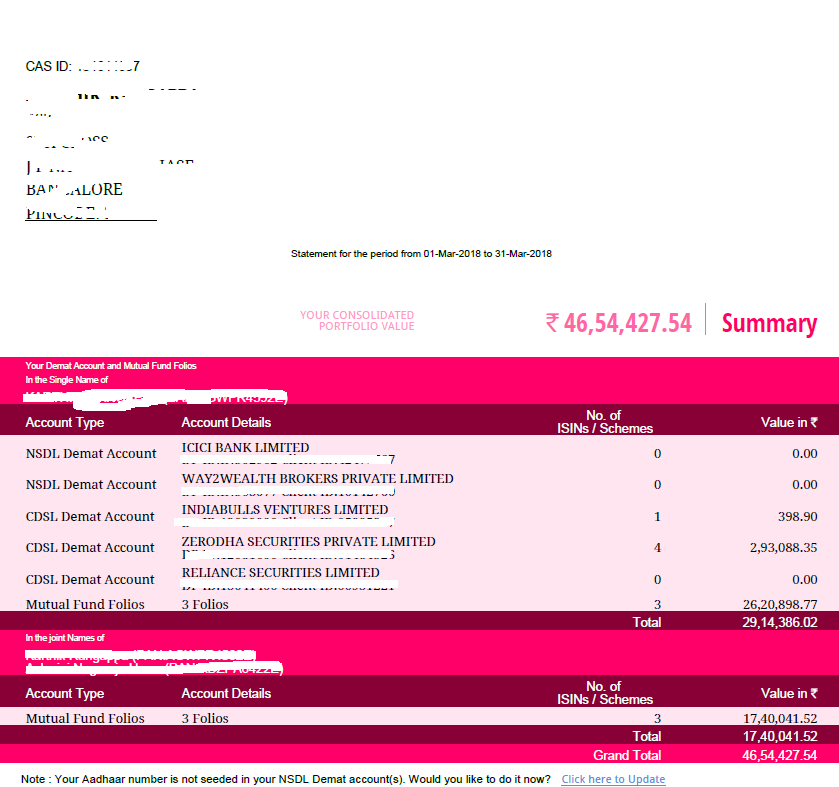

This is the intro page (should also give you a perspective of what a CAS statement is)

This is the snapshot of all DEMAT accounts held against your PAN and all MF folios you hold. DEMAT accounts and MF Folios are separated with single holder and joint holders. This also gives you a quick view of consolidated portfolio value -

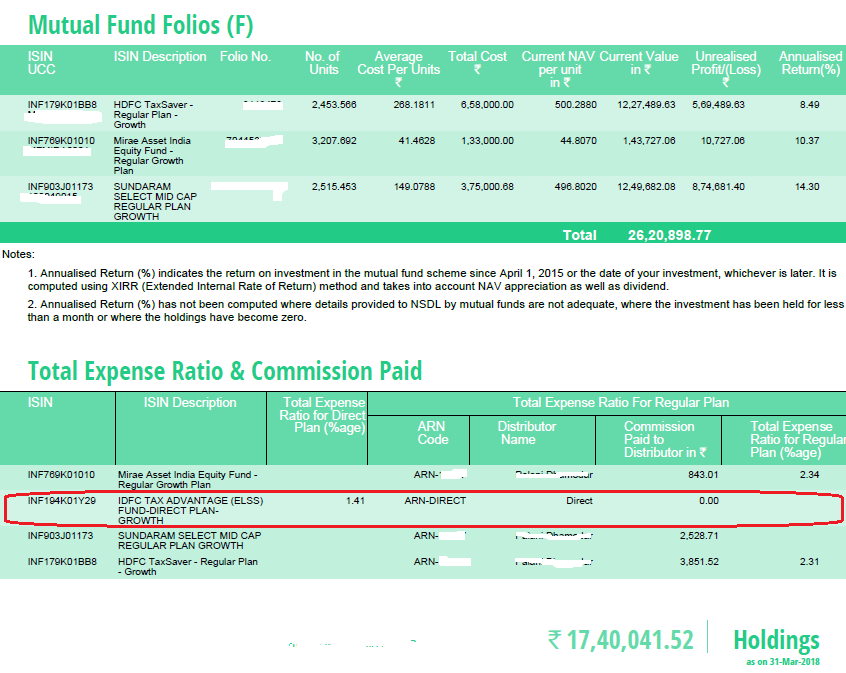

I’ll skip some of the other sections in this report and moving directly to the MF section.

In this section, the CAS report details the funds you have invested in and the respective commissions you paid the agent (agent is identified by his name and his ARN number).

Notice, there is one direct MF, which I’ve highlighted, see the commisions paid ![]()

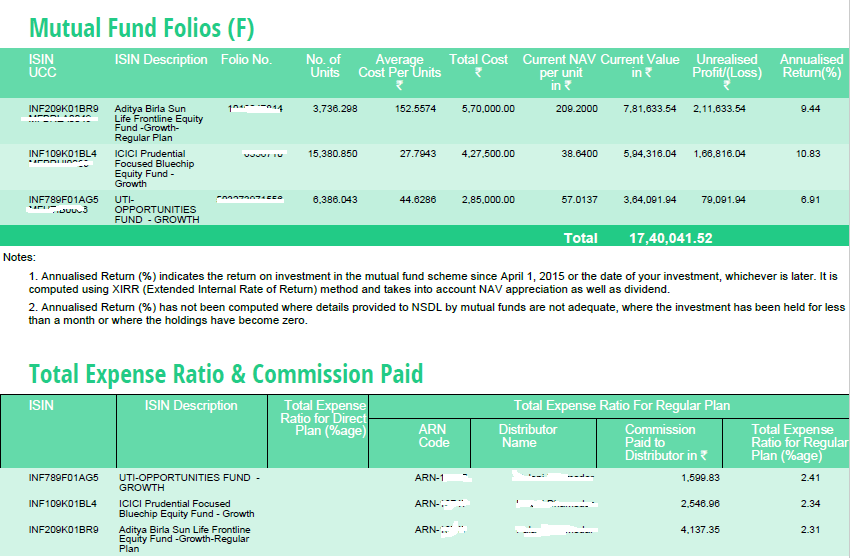

Here are more commission paid details -

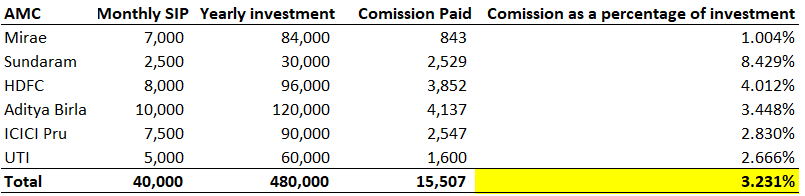

I’ve consolidated his yearly SIP investment and commissions paid information in the table below -

So this guy has essentially paid a whopping Rs.15,507/- as commission over a total yearly investment of Rs.480,000/-. This is 3.231%, which I think is quite massive.

I know the pro regular MF folks will jump at this and suggest that I should not consider the yearly investment but rather the total accumulated value in the fund. But this is exactly my problem ![]()

Why should I consider the accumulated wealth? When pay commissions for the investment made in the past? MF investment is for the long term, it implies there should be no any meddling with the MF portfolio, so why pay commissions perpetually to the agent for nothing? What subsequent role is the agent playing here?

Your comments are welcome!