Bank Fixed Deposits have traditionally been one of the most popular investment tools as it is considered to be safe & secure and earn guaranteed returns. But with the steadily falling interest rates since 2012, investors are slowly turning their attention to Debt Mutual funds. Both Bank FDs and Debt mutual funds are investments in the fixed income space for short / long term goals. Banks offer compound interest rate for fixed deposits based on the term or duration chosen. Debt fund returns, to a great extent, depends on the overall interest rate movement. Let’s take a closer look at how each of these investment instruments work and how best to decide which is right for you:

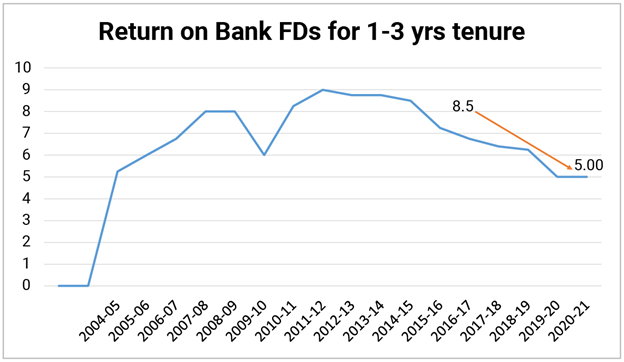

Figure 1: Steadily declining interest rates on Bank FDs since 2012

Source: TABLE 67: STRUCTURE OF INTEREST RATES

- RBI as on Sept 05, 2020

How do Bank FDs work?

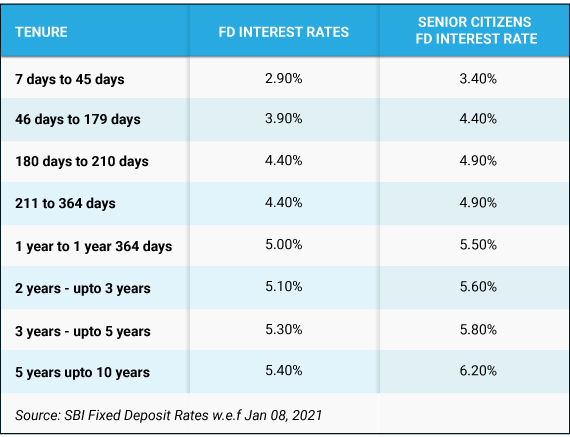

Bank fixed deposit (FD) or term deposit is a type of savings, where you agree to lock the amount and not withdraw or access your money for a fixed period (say 7 days to 10 years). In exchange, you earn returns in the form of interest on a cumulative basis throughout the period which gets added to the principal amount invested.

There are several types of fixed deposit instruments such as Tax-saving fixed deposits, Senior Citizen’s Fixed deposit, Cumulative and Non-Cumulative Fixed Deposits.

How does a debt fund work?

A debt fund is an actively managed mutual fund that pools money from investors and puts it in fixed income instruments such as government and corporate bonds, non-convertible debenture (NCD), government security (G-sec), treasury bills (T-Bill), commercial papers (CP), certificates of deposit (CD) and money market instruments. There are sixteen categories of debt mutual funds defined by SEBI. The yields investors receive from debt funds is based on the interest income. The yield-to-maturity on these funds which means the speculative total return anticipated until maturity, depends on the yield of the underlying securities which in turn is a function of the maturity (duration) and credit quality of these securities.

The returns earned from debt fund are inversely proportional to the interest rates prevailing in the economy. If the interest rates are rising in the economy, debt fund portfolio might give you lesser returns, due to the falling price of bond and vice-versa when interest rates are falling.

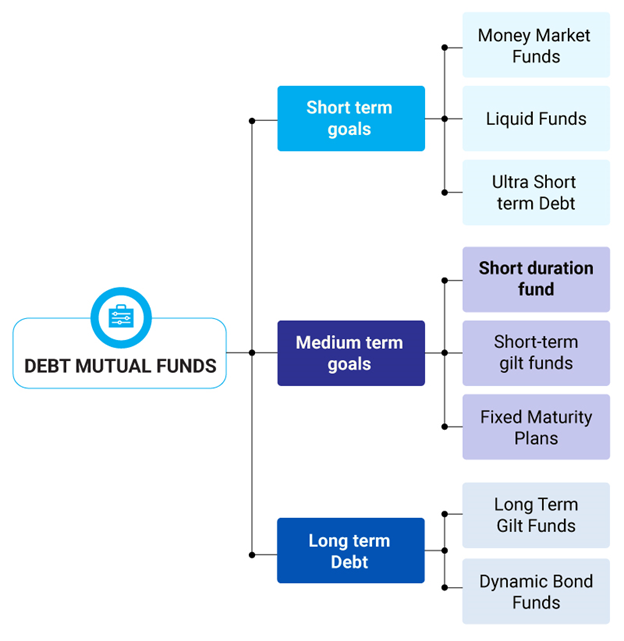

For very short tenures, say up to 3-6 months, one can consider investing into liquid or ultra-short term funds. However, every investor should consider the credit risk that varies as per the instrument chosen.

For relatively longer tenures, one can decide to invest into long-duration funds and 10-year gilt funds, depending on risk appetite.

Type of Debt Funds as per goals

The risk-reward trade-off

In a fixed deposit, the interest rate is fixed for the tenure of the deposit. In a debt fund, however, returns could change depending on the movement of interest rates. If interest rates go up, yields of instruments in your portfolio will go down, leading to a fall in net asset values (NAVs) and hence your returns. On the other hand, NAVs will go up if interest rates fall.

If your priority is safety of your capital with least amount of risk, you may consider investing in bank fixed deposits. If you wish to benefit from potentially higher gains at the cost of relatively higher risk, you may consider investing into debt mutual funds suitable in line with your goal and risk-appetite. However, as investors, you should note that your priority for Debt funds is the safety of your capital and tax efficiency instead of chasing after returns.

The safety of debt funds depends on the type of debt funds, the quality of the bonds underlying in the portfolio and the interest rate fluctuations. When opting for debt funds, select mutual funds with underlying AAA-rated bonds in the portfolio. It is safer as compared to lower-rated bonds, where you may lose money if the bond-issuer defaults on principal and interest repayments.

Taxation on Debt Mutual Funds and Fixed Deposits

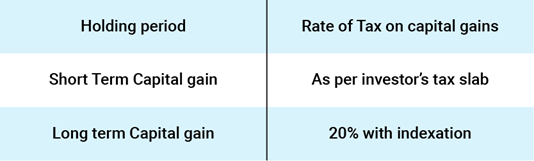

Fixed deposits and debt funds are taxed differently. Interest income from fixed deposits are added to your taxable income and you have to pay income tax according to that income. In the case of debt funds, you have to pay capital gains tax. If you redeem debt funds before three years of investment, i.e. short term gain, it will get the same treatment as a fixed deposit – that is, you will have to pay income tax according to your slab rate. If held for over three years, the tax on debt funds will be treated as long-term gains and will be taxable at 20 per cent with indexation, and 10 per cent without indexation. Indexation adjusts the purchase value of your investment for inflation, reducing the capital gain, and hence your tax burden.

Inflation Adaptability of Debt Mutual Funds and FDs

Everyone knows that inflation eats into the future value of your savings. Debt mutual funds, inspite of the risk, have the potential to cope and adapt better with inflation. For instance, if you have invested in an FD at 5.1% interest, and the inflation rate is 6%, the adjusted return would be -0.9%. Debt funds may deliver relatively higher returns.

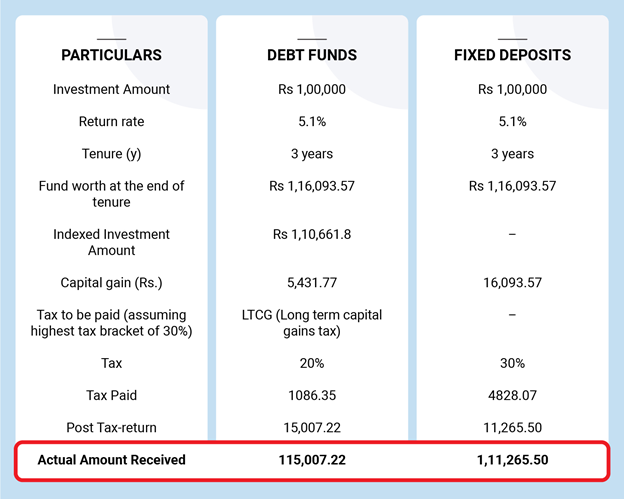

Let’s understand indexation benefit with an Illustration. Suppose an investor invested Rs.1,00,000 in Jan 2018 and redeemed his investment 3 years later in Jan 2021. For the sake of comparison, the rate of return on debt mutual fund has been assumed at the same rate of an FD at 5.1%

The above table is for illustration purpose to explain the benefit of indexation.

As we see in the table above, the indexation benefit accommodates for the inflation costs to calculate the taxable amount on your returns.

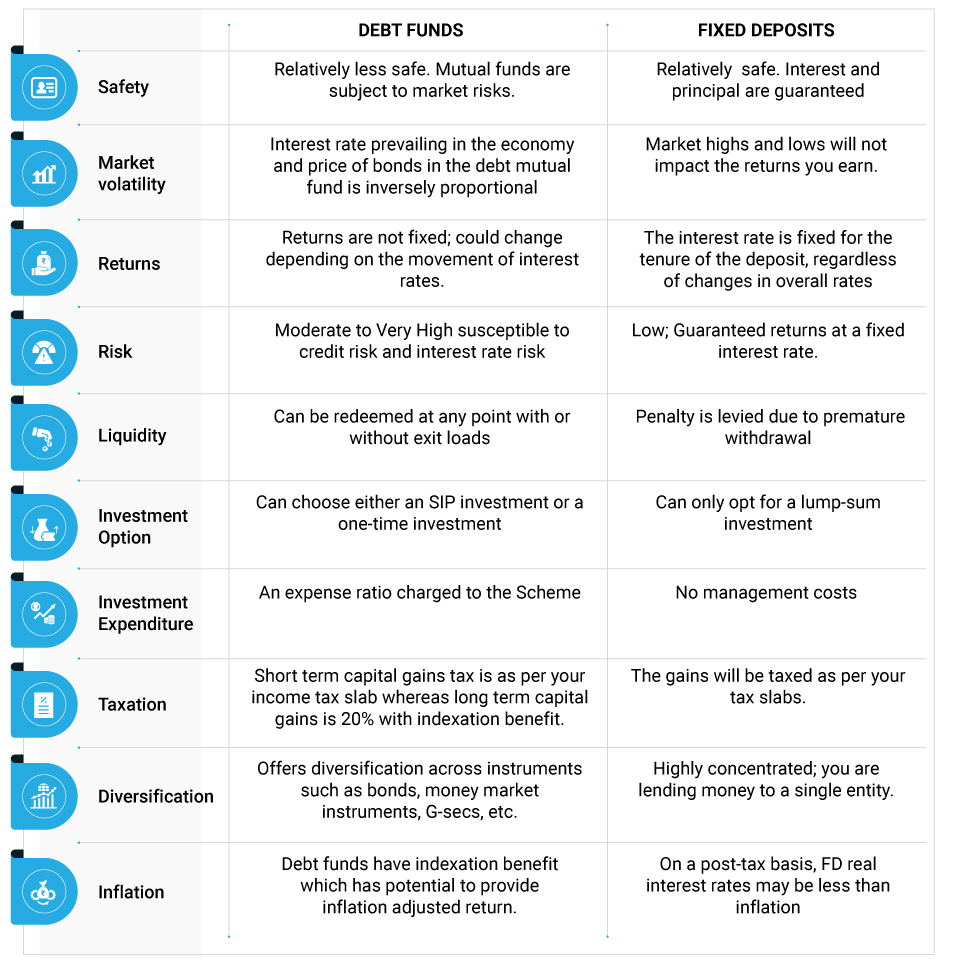

Let’s see an overview of the differences between debt funds and fixed deposits so that you can figure out for yourself which one’s best for you:

In conclusion, investors should not consider debt funds only in search of returns but as an option to consider to park their savings instead of relying solely on bank FDs. Debt Fund carries lesser amount of risk when compared to equity mutual funds. Debt funds acts as a portfolio diversifier for your investment from the downside risk due to market fluctuations. Ultimately, you should weigh your decision on your risk appetite, income tax slab, time horizon and investment goals before you decide which is the right mode to park your savings.

*Note: The comparison with Fixed Deposits has been given for the purpose of the general information only and not a recommendation to invest. Investments in Quantum Mutual Fund should not be construed as a promise, guarantee on or a forecast of any minimum returns. Unlike fixed deposit with Banks there is no capital protection guarantee or assurance of any return in Quantum Mutual Fund investment. Investment in Quantum Mutual Fund as compared to Fixed Deposits carry moderately high risk, different tax treatment and subject to market risk and any investment decision needs to be taken only after consulting the Tax Consultant or Financial Advisor

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.