This article is written by Mr. Chirag Mehta Senior Fund Manager - Alternative Investments

India, despite being one of the largest consumers of gold, is a price taker. What we mean by a price taker is that the prevailing International gold price is used to set gold price in India. The International gold price is used as a base price and converted to Indian rupees using the Dollar/ Rupee rate and we add to it various Indian duties and levies to arrive at the Indian gold price. We call this as the benchmark gold price or also known as the theoretical gold rate.

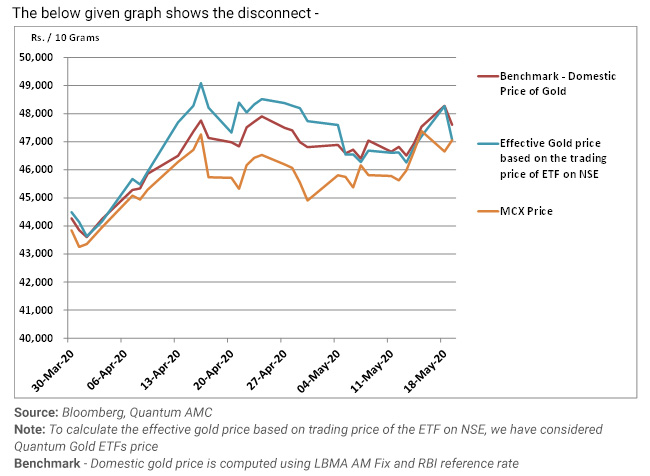

With that background, we are trying to explain gold market behavior over the last couple of months due to the lock down. Most investors track the prices that they see on TV channels, newspapers, web portals. Most of these showcase MCX gold prices. MCX is a derivative exchange and reflects futures prices. As a result, many Gold ETF investors are concerned about the apparent price disconnect between physical and derivative gold markets. Earlier we had physical gold-backed Gold ETF prices seemingly increasing faster than MCX prices and now the Gold ETF prices seem to be tapering off and MCX prices are seen catching up.

As we have gone through phases of lock down, there was an apparent disconnect between physical and the derivative gold markets.

In early April, when the existing inventory of gold started reducing and no new gold imports could arrive due to flights not operating, increasing demand led to a buildup of premium for the physical supplies in the Indian markets. This premium is seen in the differential between the red and blue line wherein the red line reflects the benchmark / theoretical Indian gold price. We have used the Quantum Gold ETF traded prices on NSE (blue line) as a proxy and equated to a converted 10 gram gold price reflective of the actual physical gold market prices.

As import of some gold was possible post mid-April, the premiums have decreased as seen in the chart below. As a matter of fact, mines and refineries were also impacted due to lockdowns globally; such premium build up was not unique to India but also seen in global markets like London and US.

However, if you see the orange line, the MCX gold prices that most of the investors track, were trading at a discount to the benchmark gold prices. The spread between the spot price of gold and the futures price is typically fairly efficient. That is to say, the two prices are normally within a few Rupees. However, that same spread (often referred to by traders as the EFP, or Exchange-for-Physical) has been wider than usual over the last 2 months with physical gold trading at premiums and futures contracts trading at discounts to the benchmark price.

The MCX gold contract prices which have been trading at a discount to the benchmark prices now seem to be rebounding to the benchmark price levels to reflect their underlying - physical gold prices - as the expiry date nears.

In the graph, we see that the physical gold price has been trading at a premium to the benchmark price and the MCX futures contract price has been trading at a discount. Both are now merely returning to benchmark levels and thus appear to be moving in opposite directions, warranting investor concerns. In summary, there is no anomaly with Gold ETF pricing and returns, it was just the market dynamics at play that led to short term jump in premiums on account of import stoppage and has been corrected now.

Also, investors should note that the one day return changes that they see in various prices could significantly differ on account of sheer differences in timing when the closing prices of each are determined. Gold ETF closes at 03:30 pm and the closing price is the weighted average price of the last half hour of trade. Whereas, MCX closing price is arrived at using the weighted average of last hour trade which ends at 11:30 pm (reduced to 5pm now due to lockdown). Given the volatility in gold markets, these closing prices could significantly differ and therefore the one day change that you see for both these products could be very different at times.

Hope that eases your worry on the price changes you see. In fact, if you think of it, despite India being a price taker we still don’t have a standardized gold price. From a price standpoint, Gold ETFs are highly price efficient, regulated vehicles to invest in 24 karat real physical gold, so build your portfolio allocation through Gold ETF now.