With IT Results season starting today, here’s a comprehensive report on IT Industry by HDFC Securities.

Some noteworthy highlights!![]()

-

Mid-tier IT and tier-1 IT are both experiencing growth, which is correlated to macros. Inflationary pressure on enterprises can accelerate technology spending. The enterprise trends are strong, and the growth vectors are: (1) strong tech spend continuity in BFSI; (2) growth delta - E&U, travel & hospitality verticals; (3) strong growth in cloud partnerships; (4) mean reversion ‘favorable’ outcome; (5) BUY/ADD on this dip. Page 3

-

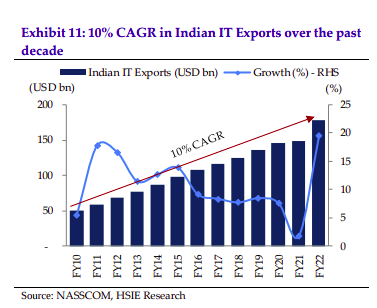

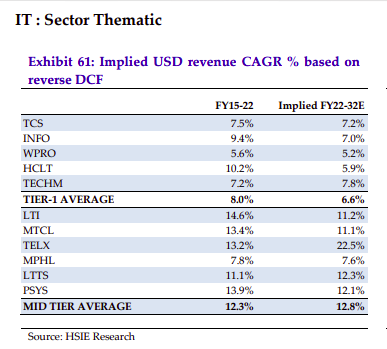

Growth in the IT sector is premised on the continuity of growth premium, with Indian IT growing at a premium of 550bps compared to global IT services and 150bps compared to US GDP growth. Deal wins are a stronger determinant of overall performance than industry/GDP drivers. - Page 8

- Indian IT has grown more by market share gains than industry growth, and its competitive advantage has been reflected in the market share displacement. The accelerated digitization by enterprises has amplified industry growth. Page 8

- The enterprise buyer segment, growth trends, and tech spend priority across industries are discussed. The key pointers are that: (1) US S&P 500’s revenue growth trajectory is still ahead of historical growth; (2) Q3 and Q4 growth moderating over the CY21 high growth base; (3) E&U vertical and travel & hospitality vertical accelerating; (4) retail & CPG vertical expected to decline. Page 13

-

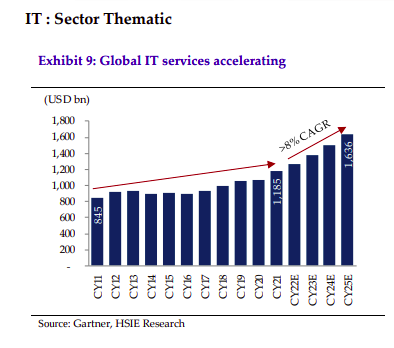

Tech value migration towards large cloud providers is underway, with AWS, Microsoft cloud, Salesforce, GCP, ServiceNow, and Adobe contributing nearly 20% to incremental growth of global tech. As a result, large service providers have started building dedicated business units and investing in partnerships with cloud providers. Page 19

-

Infosys has seen the least drawdown in EPS estimate within the tier-1 IT sector, with EPS cuts in only two years of the past 15 years. Page 23

-

Built 12% earnings CAGR for tier-1 and 17% earnings CAGR for mid-tier IT companies over FY22-24E, assuming a flat margin trajectory. The earnings estimates are slightly below consensus. Page 23

-

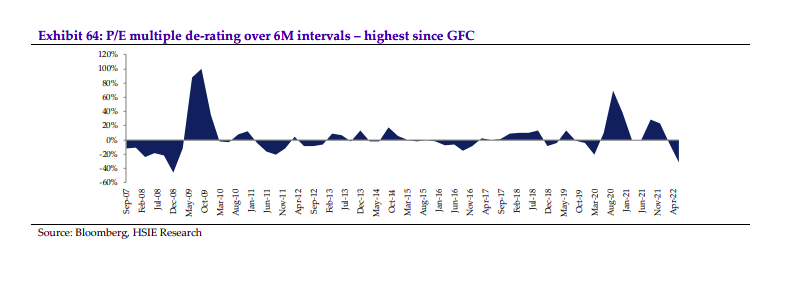

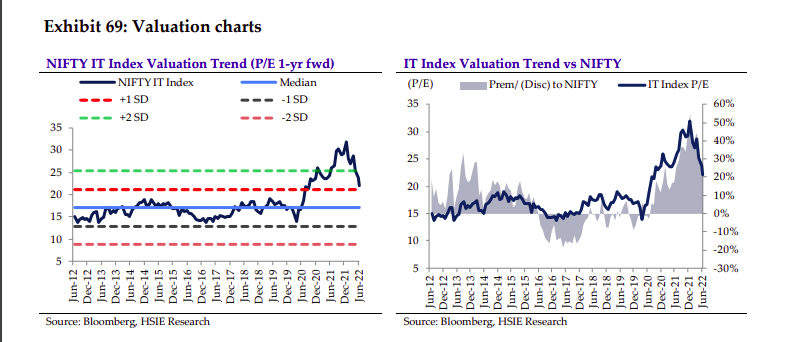

IT index P/E multiples have corrected 35% from their peak of 35x in Dec-21 to 22x now. Valuations are near five-year average multiples and at a 15% premium to 10-year average multiple.

-

USD Revenue

-

Q1 Preview

-

Corelation with US GDP

-

Valuations

-

TCS’s growth drivers include a full-stack services portfolio, dominance in BFSI vertical, strong global tiering with leading cloud platforms, industry-leading execution and operational metrics, and a calibrated focus on building upstream/consulting with org. structure changes to improve client mining. Page 33

-

Infosys will lead the growth within tier-1 IT with incremental revenue addition >80% of TCS’ incremental adds, supported by a strong digital portfolio, top tiering in cloud partnerships, and operational efficiency. Growth catalysts include mega net new deal signings and recovery in the life-science vertical. Page 36

-

HCL Tech’s growth will be driven by mode-2 services, large deals, cross-sell into the P&P customer base, strong hyper-scale partnerships, ER&D opportunity, scale advantage, and Europe expansion. Catalysts are vendor consolidation and mode-1 services deals, and the key risk is a disproportionate impact on ERS portfolio due to macro weakening. Page 39

-

Wipro’s growth is supported by investments in global account executives, leadership diversity, the scale of consulting business, strengthened BFSI portfolio, and accelerated investments in alliances. The company’s TP is INR 490, 19x FY24E EPS. Page 42

-

Tech Mahindra’s growth would be led by the scale-up of sub-segments within the enterprise division, consistency in deal wins, and improved capability and synergies from acquisitions. Key risks include operational underperformance, high dependence on sub-contracting, and acquisition intensity and its integration. Page 45

-

L&T Infotech has a strong track record of account mining, a diversified vertical base, solution expertise, and scope to increase the base of the pyramid to improve efficiency. Growth catalysts include large deal wins, joint GTM with Mindtree, and an uptick in the insurance vertical. Page 48

-

Tata Elxsi is a niche ER&D and design services provider with industry-leading growth and operating profile. Its outperformance has been led by an increase in project duration and scale-up in multi-million deals and building sub-verticals/adjacents such as off-highway, rail within the transportation, and OTT & new media within broadcast & communication. Page 51

-

Mindtree’s growth is led by strong credentials in hi-tech and travel & hospitality verticals, scale-up in the partner ecosystem, focus on building full-stack services, cross-sell/upsell focus, and reducing growth dependence on the top accounts. Page 54

-

Mphasis’ growth is based on the direct vertical business momentum, PE portfolio channel, BFSI vertical prowess, Europe geography, organic momentum, and negligible portfolio risk from a decline in the DXC channel. Key risks include high concentration of BFSI vertical, supply-side risk, and interest rate increase impact. Page 57

-

L&T Technology Services (LTTS IN) has established itself as a leading pureplay ER&D service provider with a diversified industry vertical base. Near-term growth momentum in transportation vertical and plant engineering will be supported by large deals and digital engineering. Page 60

-

Cyient has a strong portfolio in communication, geospatial, and railways, but low exposure to the Auto (EV) ecosystem. The company has always traded at a steep discount to ER&D peers, but we increase our FY23/24E revenue estimate by 9.6/8.2% and EPS estimate by 2-3%. Page 66

-

Sonata’s Microsoft portfolio is driving growth, and the company expects the Microsoft channel to grow 15-20% YoY over a longer period. The company’s new CEO will lead a strategy refresh, and the impacted travel vertical is set to recover. Page 69

-

Mastek has a strong partnership with the UK government and has been a prime growth driver. We downgrade Mastek to REDUCE from BUY and reduce revenue/EPS estimate by 7.7/6.6% for FY24E, considering the slowdown in organic growth, cross-currency impact, and margin decline. Page 72

-

Zensar has historically struggled with portfolio issues, revenue leakages, low single-digit organic growth, and inferior margin profile vs. peers. The company has since completed a strategy reset, invested in the right direction to strengthen BFSI and Data Engineering capabilities, and recovered to high teens EBITDA margin. Page 75

Disclaimer : This is solely for research and educational purpose, and not a recommendation to buy or sell.