Will it effect Commodities derivatives too or only limited to equity derivatives ?

No info

Proposal by SEBI may get rejected too

Wait n watch

How can Sebi do this. Indian markets have a very long way to go in terms of liquidity compared to us or other foreign markets. Doing such a thing will not only create more problems for liquidity but also discourage business growth and education in india. @nithin Is there any way that sebi can hear from small retailers like us, if there is… then is there any chance they might reconsider their decision?

Good question.

Lets hope for the best.

Read this

@Som_E Thanks, i have submitted it. But will there be someone who is actually attending on the other side or?..

Let’s hope it works.

And let’s see if Nithin has any suggestions.

That also We can do.

hope it does

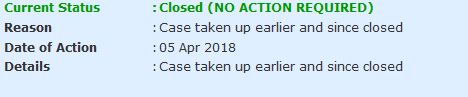

Yes, I had registered a grievance with PMO… This is the result →

Mr. Ambuj Sharma (designated officer) has received my grievance but he closed it ![]()

why should the PMO care about the small retail trading community?.

you are not donating to their party and you want something for free in this country?.

@trader_dude hey man it looks like you really want sebi to impliement their restrictions on retailers. Why do you think so?

i dont want them to implement. But considering how naive and underfunded the retail traders are in this country, i feel its a good move.

But think here for a second, if the income of an individual is higher , he is obviously financially well off , so he can afford to risk his money in derivatives.

But can a person with low income trade in derivatives? what is his account size ?

I think they should base entry in to derivatives based on account size and not income though, that would make more sense.

I really doubt they can implement this. So why everyone is so scared. LOL.

@trader_dude ya true even your side of the story makes sense but making very stringent rules might also kill the market. We do to find the sweet spot really.

Ppl with inheritances have low personal income, but access to funds.

Ppl may retire, get some gratuity and choose to trade.

Same applies to agriculturists (and yes there are agriculturists who trade)

There are some modern agriculturists. Not everyone is illiterate and dumb.

Etc

More importantly, the point is about the freedom to choose.

Ppl also make Loss In real Estate also. (Unitech flats in NCR is a example)

So should ppl stop Owning real Estate?

No chance of that!

Such restrictions sound Meaningless, isn’t it?

Development of a individual /country comes from taking healthy risk.

Avoid excess risk is important and that can only be achieved by spreading education/awareness.

Not restriction.

Look at Indian economy before & after liberelisation.

Infants take the risk of stumbling!

(including everyone in this forum & the bureaucrats @ SEBI)

And so, they/we learn to walk.

Enough said!

need to talk please contact me

My personal view on this.

*Data and material is collected from various sources.

Before commenting on actions of SEBI I believe first we should know the reasons that prompted SEBI to consider these kind of formidable changes to F&O market.

According to finance ministry data, equity derivative markets are growing disproportionately compared to equity cash market, in 2017 F&O turnover was 18 times that of cash market turnover compared to 9 times in 2011 and 3 times in 2009.Alarmingly this growth is witnessed with decrease in number of derivative investors to 5.7 lakhs in 2017 compared to 10.6 lakh investors in 2010.

India ranks second in the world only next to Korea in terms of ratio of derivative turnover to cash turnover. Also according to global standards percentage of non-institutional trades in derivatives accounts for more than 58% which is considered as quite high. Individual investors contribute to almost 1/4th to the total volume of equity derivative trades in India and some percentage of this never traded in cash market. Retail investors in India bet on a notional value of $800 billion of stock futures in 2016, more than the value of stock futures traded in all of Europe, Hong Kong and Singapore combined.

Definitely this data suggests growth in derivative markets in India is mainly driven by speculation and is not sustainable.Also after analyzing this data finance ministry has a reason to concern and wants

SEBI to contain this alarming growth of derivatives compared to equities and want to implement measures that boosts growth of cash markets.

In order to attain sustainable growth,to rationalise, reduce speculation by retailers and to increase their participation as a whole in F&O SEBI is mulling various options.

-

Considering to increase minimum contract size to 10 lakhs from current 5 lakhs, but this is mostly ruled out as there was no effect intially when contract size was increased to 5 lakhs from 2 lakhs and currently there are handful of stocks whose contract size is already much above than 10 lakhs. Also this implementation can lead to rise of dabba trading again in India where one can bet without paying any taxes in multiple small lots.

-

Recently SEBI notified the revised framework for stock derivatives trading under which the stocks that fails to meet the enhanced eligibility criteria will be moved from cash settlement to physical settlement. The move is part of Sebi’s broader plan to completely move towards the physical settlement of stock derivative contracts, which according to it is necessary to curb high amount of speculation in the markets. No doubt, this move will filter out companies with lower trading interest from the F&O segment but few believe in first place stringent criteria should be there for any stock to be allowed to trade in F&O.It is also necessary for the regulators to strengthen the support systems before announcing such measures. Physical settlement is mandatory in several global markets. However, all these markets have strong stock lending and borrowing (SLB) mechanism through which investors borrow stocks at a marginal cost. However, SLB in India is still evolving, leaving little choice for derivatives investors who take short positions.

-

Another proposal from SEBI is to alienate retail investors from F&O is restriction on trade in cash and derivatives based on their disclosed income according to their income tax return over a period of time. For exposure beyond the computed exposure, the intermediary would be required to undertake rigorous due diligence and take appropriate documentation from the investor,which is highly impractical for brokers to implement this. Also client can give same ITR to multiple brokers and trade with additional exposure than permissible limit, one wonder how this can be kept under check? What if one inherited capital and want to trade with that? so, there are many questions unanswered with this proposal.

-

Also SEBI is considering to introduce concept of product suitability for investors in India as prevalent in other advanced markets. The main motive of this would be “Any product sold to investor should be suitable to him”. Not sure how this will evolve considering various parties involvement,customized needs, individual risk preferences, eligibility and different financial capabilities.

-

Few experts also suggest so as to curb speculation by retailers regulators should address lower taxes on options.As Securities Transaction Tax (STT) on options trades is levied on the premium amount only while it is levied on the full value in cash market trades.

-

Few suggest that SEBI should consider relevant education as prior eligibility for investors to trade in F&O, in this way they are fully aware of risks involved upfront.

-

The other focus of SEBI was on algorithmic trading framework and the regulator decided to streamline the segment, it allowed for members to operate from the co-location facility (as this would reduce costs),provided for dissemination of tick-by-tick data to all trading members; tightened the criteria under the order-to-trade-ratio which will now apply a penalty for orders at plus/minus 0.75% of the last traded prices, against plus/minus 1% earlier and extended its applicability to the cash segment; called for a unique identifier for each algorithm; enhanced disclosures on latency by exchanges.

-

The regulator also made norms more stringent for errant listed companies and allowed stock exchanges to impose fines for non-compliance with the new rules. It also empowered the stock exchanges to freeze shareholdings of promoters in non-compliant entities (as well as their holding in other securities) and to suspend their listing.

Considering the motives of SEBI one should appreciate it but too many regulations within short period of time may play spoilsport, kill liquidity and shatter derivative markets resulting in rise of parallel markets such as dabba trading.

@siva i never appreciate SEBI, instead of progressing SEBI is going backward , but as you noticed , that things surely happen , remember the days of restrictions on Gold , finally Govt realized the issue and modified it. Now the Finance ministry is begging people to buy Govt supported Gold Bonds. For every thing related to stock market SEBI is giving an example of American market , but the same SEBI board not able/failed to learn simple thing from them , at least SEBI should learn from Chinese examples.

Ill-conceived decision like point number 3 will encourage dabba trading more than anything else.