Was talking to a few trader friends past few weeks. Some of these have been trading quite actively in F&O, may not be pro but have proper setups, charts, discipline etc.

But when I asked them asked them how do you quantify/manage your risk- like what’s your net delta right now across all your positions? I mostly got blank stares and pretty disinterested faces.

Which felt very odd to me because I know institutional trading is entirely based on risks and not on size/notional or lots. Curious if retail traders even think from risk this way at all? Or just decide the positions size based on some other factors? If there are other factors, what are these factors?

I dont look at it in terms of Delta as such… but I have a system that balances risk purely on position sizing across strikes, its intuitive to do that considering I am mostly ATM/CTM.

Institutional traders have 1000s of positions across different markets/expiries/strikes, and they have to measure greeks to have an overview of their positions.

i am selling only option in stock 15% away from current price - target only 2%

IN iTC, Reliance, NTPC, Powergrid, Monthly 55 k receiving , Bond interest is coming 25k month - again reinvested in Whiteoak midcap, quant multi and invesco small cap fund

Everything include compounding 30% CAGR - that’s enough for me

Now a days selling option is costly in index - and more volatility is killing in indiex ,

See. Told you. No connection to the previous post at all. You keep posting whatever you want with no connection.

Also one request. I dont think anybody want to know how much interest you get per month and all. So it’s better to avoid such things.

That’s what I feel. If others want it then it’s fine.

Thanks, makes sense and yes you do get a sense of intuitive risk if you’re doing it long enough. That said, I would still look at the scenario analysis to quantify the risk. For e.g., even if I am running a simple position as a naked call, I would still want to know the spot/vol or spot/ttm grid to quantify the result. And I’ve experienced myself getting surprised and humbled by the results when there is extreme vol levels(both low and high).

Everything is quantified via backtests over long periods. So seeing intuition/common sense validated consistently over long periods helps build conviction.

Plus I mainly do ATM/CTM STBT with adjustments. For my strategies I dont get into analysis paralysis.

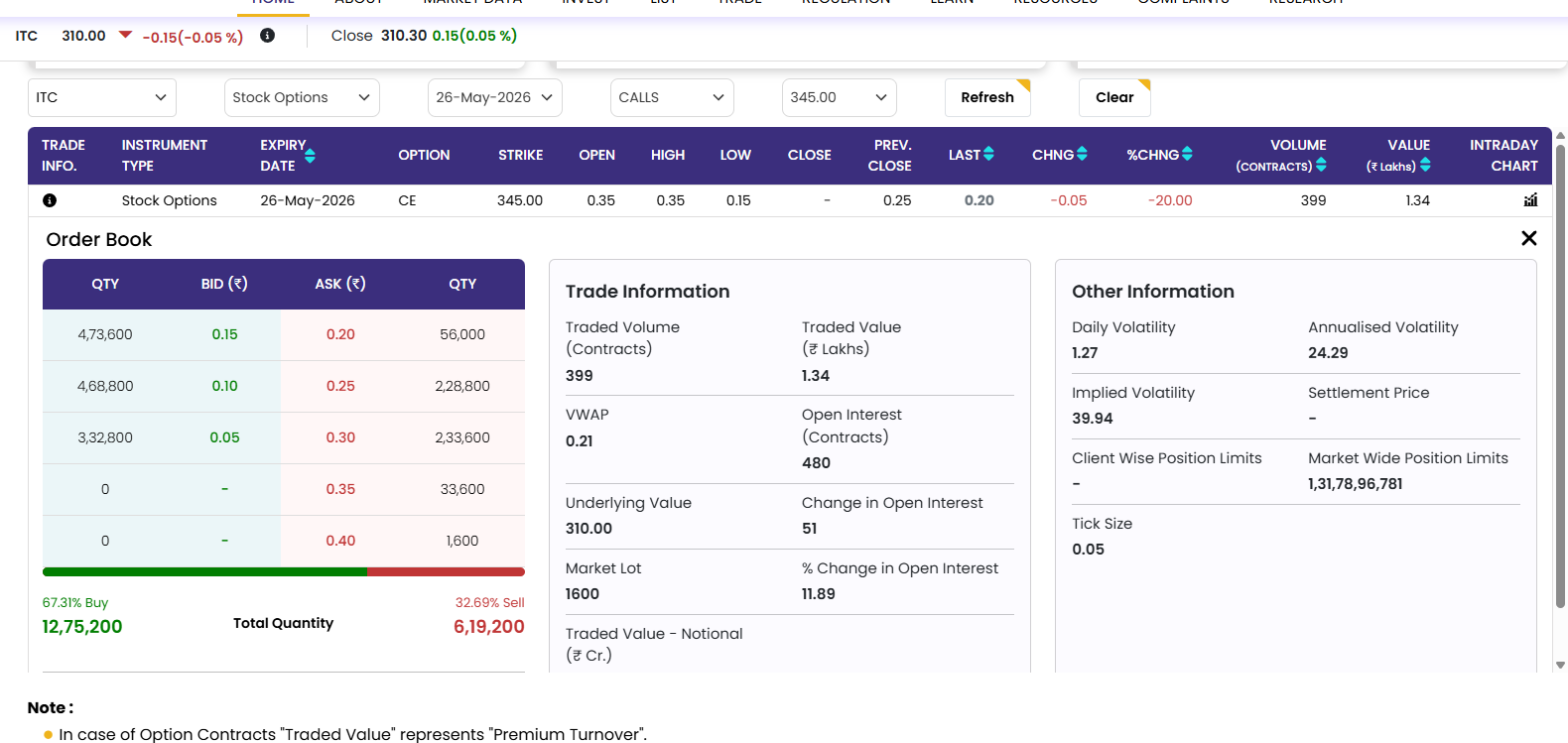

Ok, there are two concerns, First- there is not enough liquidity other than ATM options for single names, and it gets even thinner for deep OTM options. Secondly, the bid ask spread(again related to liquidity but even for smaller size) itself costs you >10% for a round trade. Just look at the bid ask for ITC 10% OTM trade- 33% bid ask!

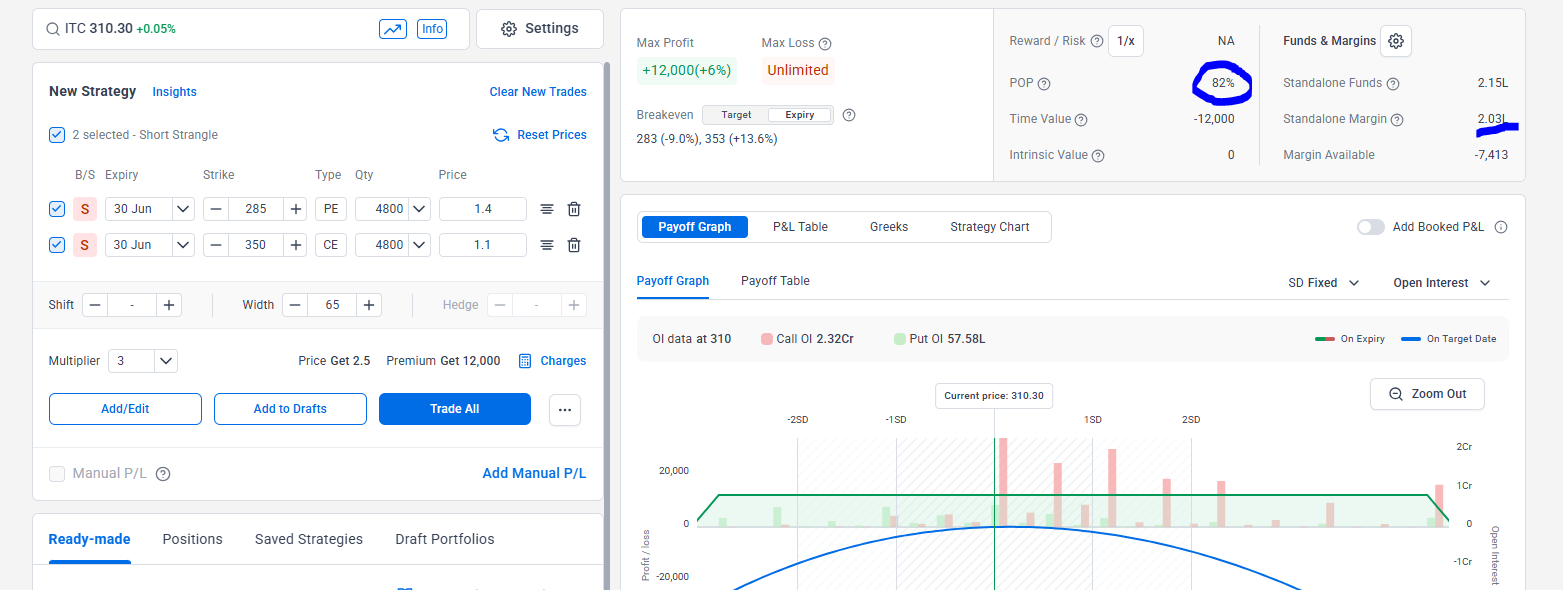

Short strangle looks like a steady income machine until it isn’t. Right there on your screen beneath the Max Loss is what I would worry about. But maybe that’s just me, good luck to you.