Does anyone have experience with A stable or BBB stable grade bonds?

Is it safe to buy it or we should only go with AA and AAA bonds?

Does anyone have experience with A stable or BBB stable grade bonds?

Is it safe to buy it or we should only go with AA and AAA bonds?

Unless you are an expert at assessing default probabilities of these bonds and credit in general, I would recommend staying away from individual bonds, not just low rated bonds. You are better off with G-Secs or debt funds.

Point of ratings is that you don’t have to assess risk individually and that the agency will update it as time passes on and when financials change.

Returns of GSsecs is not comparable to bonds. They pay 7%. Tax on top of it.

I would say he can definitely stick to AAA or AA bonds atleast right?

AFAIK, these ratings are trailing indicators.

It will be interesting to review historically how often AAA bonds have defaulted or deferred their interest payments / principal re-payments (and subsequenlty were downgraded).

Also, the move Big Short (2015) showcases a common failure point of such ratings.

In early 2007, as these loans begin to default, CDO prices somehow rise and ratings agencies refuse to downgrade the bond ratings. Baum discovers conflicts of interest and dishonesty amongst the credit rating agencies from an acquaintance at Standard & Poor’s.

Yes obv who can predict in future. All we can do is hope. Chances of your hopes turning out correctly increase when ratings increase.

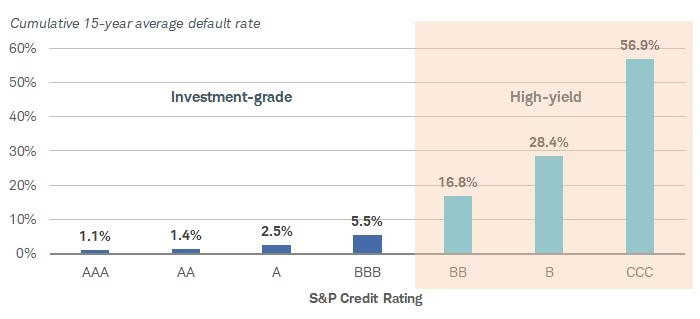

Bond ratings summarize the risk of default for an individual bond. The safest bonds—AAA, AA, A, and BBB—have a one-year probability of default that is less than 0.1 percent.

as per https://www.newyorkfed.org/medialibrary/media/research/current_issues/ci2-6.pdf

Taken from https://www.schwab.com/learn/story/what-happens-when-corporate-defaults-rise

And yeah I have watched The Big Short . ![]()

Ratings aren’t infallible. They can change dramatically in a single day like ILFS, DHFL etc. You can argue these are edge cases, but the question is do you want to assume that risk with an asset class that is supposed to protect capital. Why take equity like risk for debt like return. This has been my framework for debt.

Depends on what you are comparing against and time period. Today, for example, the entire yield curve is flat and the spread between corporate bonds and G_Secs is flat. It makes very little sense to invest in corporate AAA bonds.

There’s some nuance here. For a person who needs income, regular bonds make sense. If not, then debt mutual funds are still relatively tax efficient. In a regular bond, you pay tax on coupons. Inside a fund, you only pay tax when you redeem. Also, funds give you more flexibility in portfolio construction. As for opportunistic trades, that’s a separate argument.

Hmmm… Doesn’t make sense.

A GSEC IS a bond, no?

A bond with zero risk of default (sovereign guarantee).

Let us compare the expected utlity of 3 hypothetical bonds -

a. GSEC yielding 7.5% (say)

b. AAA bond yielding 9% (say)

c. BBB bond yielding 14% (say)

Assuming the typical “invest in bonds for stability” and not income approach,

the additional 0.2-0.3% of expected-utlity in corporate-bonds compared to GSECs,

hardly seems worth it, considering the impact on one’s life of losing the entire principal.

Would you agree?

Or do you think the above is an example of failing to overcome loss-aversion ?

I was talking about corporate bonds, the kind @Abhijit was thinking about

Yeah true there is not much difference in returns of AAA and Gsecs now.

Debt funds seem best, taxation wise. If we invest in corporate bond funds and a company defaults, impact could be low because of diversification among bonds by the fund manager.

I feel the stability Gsecs offer is a bit overkill for retail investors considering we have much lower capital. 7% on our capital is not same as 7% on the hundreds of crores these big funds invest in Gsecs ![]() . Does not make sense (to me) to invest in Gsecs due to my low capital.

. Does not make sense (to me) to invest in Gsecs due to my low capital.

Small finance bank FDs are offering 8-8.5%+ now and they are insured too. They have DICGC insurance upto 5 lakhs. Can easily spread deposits and sleep peacefully with better returns.

Yup. Max-out your investment in FDs upto the insured limit / threshold for extremely quick and liquid emergency needs. Can then think of getting into GSECs.

Purely from a risk perspective, here’s a handy list i like to use -

When thinking of investing in N,

first think whether you have already maxed-out your investments in 1 to N-1?

(and still have some left to “invest” in N ?)