AFAIK US economy is developed and there is less prospects for growth for companies in US as compared to companies in emerging markets like India.

Also US equity market is less volatile so does it makes sense for Indians to invest in US equities.

I know even though US is developed there is a possibility to find 3x , 4x returns over few years.

But probability of finding such returns should be more in Indian right?

Also US equity market has more than 6k listed companies with around 4-5k companies with market cap more than 300MM i.e. large mid and small cap stocks.

And India has around 1k companies with market cap of 500 cr and more. Which should make it easier to analyse and keep track of companies financial performance.

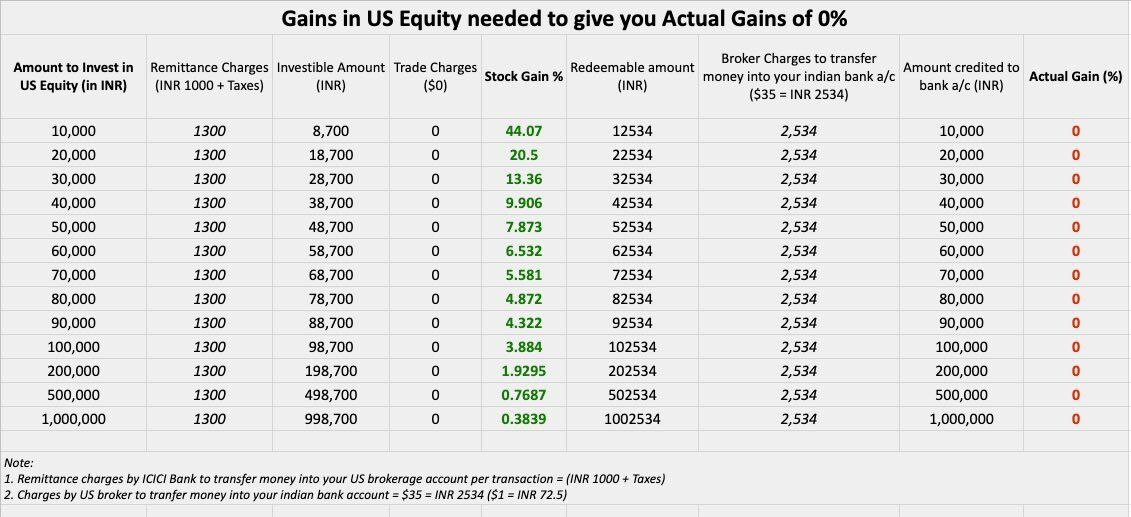

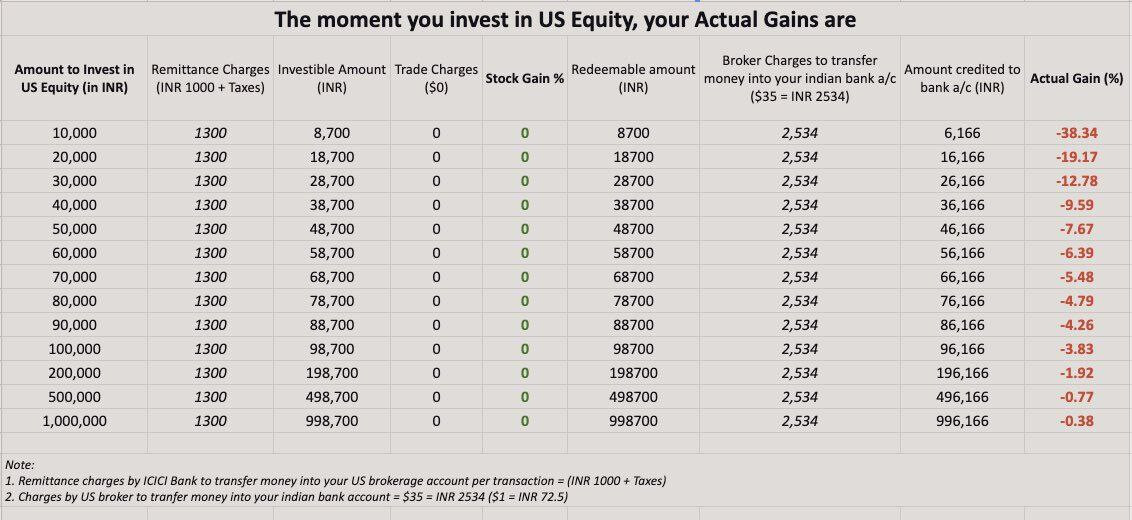

The forex mark up for most banks for retail customers is around 3.5 %. so, there is a hurdle rate of 7 % for just round tripping the money.

so, straight answer to this is, it doesnot make sense for small time retail investors.

The returns and risks (std dev) for long term investments is quiet similar between S&P 500 (in INR) and Nifty 50. Returns of S&P 500 are slightly better but nothing worth noting. The good thing to note is there is no correlation at all. This means that when Indian markets are up, US markets are not so great but when Indian markets are falling, US markets will be doing better. So it makes a great diversification tool…

Apart from the standard exchange transaction cost, there is TCS (Tax collected at source) of 5% that will be deducted when you convert funds from your resident account. Please read the attached article on this. However if you are an NRI and maintaining NRE account, then this TDS will not arise if you remit the funds from your NRE account.

True…

But it makes sense to me as earning in UK and Singapore and investing there…it charges 7% to send and get back money to India market’s and considering the rupee value is going down…then when I take money out of India it will be costly with transfer chargers and also rupee going down

But India’s who spend rs60 per dollar after years will get rs74 per dollar and only have to worry on 7% fees.

i completely understand your argument and infact what you do would be the right thing given the continuous rupee depreciation in the past.

but, times seem to have been changed. back then we hardly had 10 months of forex reserves and it was always a call between defending rupee from speculative attacks and saving for imports.

But, covid scenario seem to be entirely different and india now has 650 + Billion $ as forex reserves ( including the dollar forwards the rbi entered).

so, DON’T BET AGAINST INDIA.

It’s not exactly what I mean to bet …what really I meant is that is worth to invest in India market’s or foregin market’s with small amount of money thinking I can take it back anytime. And also what I told the currency advantage india gor other’s don’t get…

Disc: Not an expert at all and I could be absoloutely wrong.

If you are an NRI and living abroad, yes, it makes sense to invest in US markets. If you live in Singapore, there are few PMS who invest in India as well (which you could consider).

With regard to INR-USD, do not expect this rate to improve. INR will only depreciate in the long term, but the rate at which it will depreciate no one can tell, what is constant is depreciation is for granted. Check with any Indian Bank who offer forward premium USD fixed deposit for NRI’s The forward rate of INR-USD in 5 years time is around 88.

There could be ups and dips in short term but in the longer term ask any Banker, it is only going to be depreciation.

If you are an NRI and wish to settle abroad, then it is pointless to invest in Indian Market and your better option is to invest in US market in USD. However if you are an NRI and wish to return to India in future, then it is better to start investing in Indian Market, so that by the time you come back, you would have a decent corpus.

How to circumvent the currency depreciation when investing in India, you could invest in tech stocks like TCS and Infosys where their major income is in USD. You can also think of investing in ETF of Motilal Oswal Nasdaq 100 or very recently, Mirae Asset - FAANG - ETF. There are few mutual funds who invest overseas as well. This will give you the benefits of investing in US based stocks and at the same time, the NAV will have the benefit of any currency depreciation as it is in INR (Taxation is a separate thing which you need to look at as well).

Please do read my disclaimer - these are my personal thoughts only and I am not an expert. @Ratna_sai_kosuru

My two cents too. I have tried to structure my thoughts on the following 4 points.

The only reason we invest in Indian equity is because we were born here. Let that sink in. We never made a conscious choice. And it has never been easy or cheap to invest outside India. Indian equity was the only convenient option for us. But now it is neither hard nor costly. You have Motilal Oswal S&P fund which allow you to own S&P 500 without any money lost in forex markup or ‘transaction fees’

India is just 3% of world’s GDP. Investing in India is very much like being a frog inside a well. India’s largest company by market cap, Reliance Industries, would be #74 in a list of US companies.

Correlation between Nifty 50 and S&P 500 long term returns is actually negative. Hence investing in S&P 500 gives you good diversification. You also get extra benefit from USD INR currency movement.

Look at the S&P 500 list of companies and then look at Nifty 50 list of companies. Which companies will you choose? Which companies do you use on a regular basis? Which companies do you want to bet your money on?

i agree on the part of depreciation. what i wanted to convey but missed doing so, is that India is better placed to defend speculative attacks on the INR. Expecting sharp depreciation in INR like in 2013 would not be wise.

The rate of depreciation has fallen and might continue to do so.

Given that the inflation trends in both countries doesnot seem to follow the historical trends, and in extreme case, both india and usa could have similar inflation for prolonged time.

with the inflation differential being the key factor for usd-inr rates, i personally dont see so much of depreciation.

inspite of all the above, mutual funds are a better vehicles for foreign diversification. i made the comments considering direct investing in usa into stocks which is in trend now. i presonally hold motilal oswal nasdaq etf.

hope this clarifies the stance taken!

there are people. i know a friend of my sibling who invests 100 dollars every month. he gets advice from a person who charges him 7500 per year. they buy fractional shares. the thing is they start at the bottom of the market and feel it is profitable now. once the music stops they will realise the truth.