Nippon focused on ETFs long before, but SBI has the highest AUM because of EPFO, its Nifty 50 ETF has 1,54,851 crores of AUM.

A lot of people trade in ETFs, they are recommended as trading instruments, including pharma and IT, and as there are lacs of active demat holders now, there is momentum in ETFs, and on the other hand index funds while getting introduced by AMCs are not pushed much because AMCs have active funds.

I guess we can consider them as 2 different segments, despite belonging to the same indices.

agreed but sayin NIPPON took the market

but again SBI EPFO is on different league only

If you are referring to the main ETFs such as Nifty and Nifty next 50 . Liquidity is never an issue till date. I am invested in these two ETFs. Every AMC, has to display the iNAV and when you buy, you can put limit order equal to that. In most occasion, the transaction will go through. Even otherwise, the intention is to hold for long term and hence the small marginal difference when compared to the overall picture would be miniscule. As an example, If you had bought Nifty 50 during march 2020 when it had gone down to 95 to 98. Now it is 182 (odd). How much of a difference does it make whether it was available at 95 or 96 or 97

The commission that SBI ETF nifty charge is 0.07% whilst Nifty Next 50 is 0.15%. I am sure index funds would be higher than this.

AFAIK Nippon had ETFs long before other AMCs were interested in introducing them, they focused on ETFs, I think they had many ETFs even when it was Reliance.

Liquidity comes with selling.

If you are investing for long term, I would suggest to do a calculation of the possible amount/units you will buy till your investment is over, apply the price-NAV difference of the ETF, and check if the lowest traded units for a period of time, and see if this liquidity is more than what you would have with you.

I buy ETFs, more so with the intention of selling them for profit and buying them again when they fall, and I stay invested as long as they become profitable, and I have not bought much compared to my other investments.

Does this mean, that I check the price of the ETF which i bought with that of the SBI Index fund of the same AMC and check the difference? Not clear

With Nifty 50, I do not sell, I just keep accumulating over a period of time, something like a SIP but at my choice. With Nifty next 50, which is more volatile, I do buy and sell. I had sold a portion when it crossed 450 and now buying it back.

NAV of the ETF is different from real time price, sometimes an ETF trades at a premium and sometimes at a discount, this is the price-NAV difference. Premium because of the demand and discount because of no demand. Not every ETF has high difference, Motilal Nasdaq 100 had high difference, it had premium.

Here is SBI Nifty 50 ETF https://www.valueresearchonline.com/funds/30710/sbi-nifty-50-etf

And AMCs will not buy if our units are not as per their size, so we have to sell in the market, and if there is less demand, then we may lose some profit. NAV is what the AMC reports, price is what we pay in real time, they need not be the same.

This is very accurate analysis. That’s why one should not consider it as standalone/isolated investment.

Its simply too risky.

however IMHO Nifty alpha index with its wild swings is very good candidate for improving gains without loosing stability in diversified portfolio with yearly re-balance. Effectively buying alpha when its low and selling high.

of course co-relation with nifty is 0.85 so it not much of gain. But if portfolio consist of low-volatility index, alpha may exhibit lower correlation there by improving stability of overall networth.

yes , However typically over longer duration, it may not be true. its high risk game.

You will be paying short term/long term tax. as you need to churn stocks at reconstitution frequency Please think how much your actual gain, with respect to Kotak, if every quarter tax needs to be paid for churn. You can do some on paper calculation/simulation with past data…

Theoretically… you can calculate index composition , its possible to re-balance stocks a week before kotak does there reducing impact cost. But alpha index do not have significant small cap exposure, so impact cost would be minimal. You may not gain much.

Anyhow if you can do some on paper calculation on past data with respect to tax due to churn, would like to know your findings. Please do share your analysis.

1 Like

I agree with you, but i’ve been backtesting it and started a portfolio too last month

sure!! I just last the portfolio last month

If you wanna know the top gainers v/s losers ill message you

And i wanna keep the chrun less too, I’ve got some quant models (hoping they work well to pick the best stocks)

I’ll be posting my entry and exits and all here

thanks for your insights

Thanks… I would be interested in knowing your overall portfolio performance (After deducting all costs and taxes) Vs nifty alpha 50 index performance year on year basis.

Would be nice, if we know about how your strategy is performing across different market cycles.

oh! you are deviating from alpha 50… which is starting point of this thread.

I do not understand stock investing much… but I can try to learn. Can you throw some light on quant models you have deployed above alpha 50… ofcource only if you want share your secret recipe.

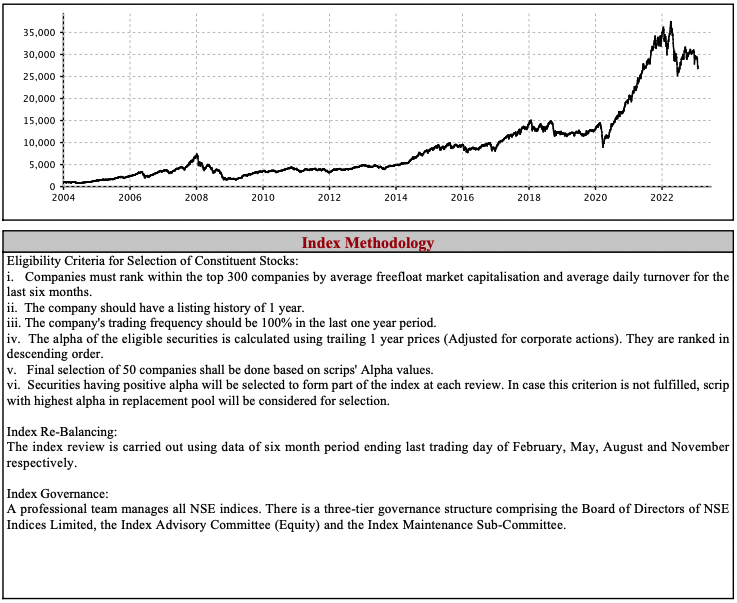

NIFTY ALPHA 50 - This is quite unbelievable. I haven’t seen any other index outperform NIFTY 50 this spectacularly (almost 3x) and so consistently.

Interestingly, kite charts is showing data of NIFTY ALPHA 50 since 2004. So the index is nearly 20 years old and yet there are not many ETFs on this?

Seems to be the case. And they started the ETF at a very wrong time and hence down 24% at the moment. Also, zerodha collateral broker limit is reached on KOTAKALPHA. ![]()

Not to discourage you, but you will be marred with the following -

- Three times the expense because of your monthly churn while the portfolio churn in 4 times a year. Remember that due to STT India is one of the costliest country in terms of % of taxes.

- Short Term Capital Gains instead of Long Term Capital Gains arbitrage via ETF/Fund.

- Error in tracking your personalised ETF and executing the same. And that also 3x times the error of any ETF tracking fund.

- Deciding on the weight of the stock. Equal weights can turn the returns upside down. And that key information is usually held by the exchange.

- Volatility can make you throw in the towel. Like starting at wrong time. KOTAKALPHA is giving almost -24% returns since inception on the same index.

Having said that, there is something definitely in the index criteria herein that augurs well with the Indian markets and is worth exploring.

Reference - https://www1.nseindia.com/content/indices/Factsheet_Nifty_Alpha50.pdf

And on a 5 year rolling basis … the index seems to be performing exceptionally well.

Reference - What is the Nifty Alpha 50 Index? How Does It Work? Should You Invest? - Yadnya Investment Academy

Disclaimer: Few data points are from blog posts … that I am not really sure and haven’t personally cross verified.

2 Likes

Amc generally rush to get a product out and if the return over 5 year period is spectacular, how come none of the AMC have come out with a mutual fund. All we have is a one ETF with a AUM of 68 cr and a 24% negative return.

Kotak AMC website does not show the iNAV same thing is missing in money control as well.

Maybe I am looking somewhere else.

Not sure how many retail individuals would replicate this index manually. Some thing is amiss. It reads like too good to be true thing.

1 Like

yes, but there is other side of coin as mentioned by @ranton137

this can be risky bet with no sufficient history. On the top of its unfortunate but factor indices in India are very arbitrary.

Lot many of us might have seen real estate prices getting doubled every three years during real estate boom. It doesn’t mean that real estate will always give good returns.

Similarly it’s possible that similarly we are only looking at best period of alpha index.

This 24% downfall can either indication of alpha index was opportunistically constituted just to look better during backtesting. or by nature alpha index have wild swings…

Only future can tell. Its difficult to comment at this point of time.

if there some other asset/index with low correlation is already part of portfolio, one can consider investing in alpha 50 index.

Personally If any fundhouse comes with MF, (not ETF FOF), I will think of making part of my portfolio, to reduce deviation. its my journey of discovering minimum variance portfolio,

its not, index value can be recreated based on historical values but the actual index was created only around 2012 or 13.

In you view, what wouldbe the reason for no AMC having a MF replicating this. Is it because of the high volatility which may not be palatable for retail investors. Also why has Kotak come out with a ETF and not a Fund. I would prefer a Fund than a ETF (personal view only)

I calculated that. Risk Adjusted Returns (Sharpe) of NIFTY ALPHA 50 are better than NIFTY 50. Note that I have considered monthly returns for STD.DEV. and considered risk free rate of 4%.

Hmm. Yeah … that will explain a lot. Someone from Zerodha should really explain the data coming in Kite and if it is being reconstructed like that in a backward manner. Unfortunately, my excitement around the index is purely based on tableview data from kite. But even then, I would love to deep dive on the criteria that is helping it outperform like that.

Hey i guess you got me wrong, the thing which i tried to say is

my quant model try to pick best stocks at right moments with in the alpha 50 universe only so that churn can be less

the data is not recreated by zerodha but nse maintains the index data in such a way. Zerodha doesnt create any data it just relays to end user from NSE or whoever maintains the index. Refer to niftyindices.com for more info