I will state my query with an example. Lets say, I have 100 shares which I have held long term. If there is a 1:1 bonus issue then I would have 200 shares. The DOA of the first 100 shares is the original purchase date & the COA is the original purchase price. According to the IT rules, the DOA of the next 100 shares (bonus shares) is the date of issue of the bonus shares & the COA is Rs. 0.

I have read that the Income Tax rules follow FIFO (first in, first out) principle. If I sell 100 shares, say within a month of receiving the bonus shares, they will come out of the original long-term 100 shares (since they were “first in”) & will accordingly attract LTCG. Any sale of shares above that, within 12 months of the date of issue of bonus shares, will attract STCG since this next sale will come out of the bonus shares issued.

My question is will the same FIFO principle apply if, instead of selling, I gift 100 shares within 12 months of receiving the bonus shares ? Will the recipient receive the original 100 long term shares?

"The holding period for determining the nature of Capital Gains, whether STCG or LTCG, would be determined from the date of acquisition by the previous owner until the date of sale. The capital asset acquisition cost would be determined as the previous owner’s purchase price to compute the capital gains.

The sender of the gift is not liable to pay taxes as the Gift Tax Act (GTA) was abolished. Under Section 56(2) of the Income Tax Act, the recipient is liable to be taxed for gifts of movable property, such as shares, ETFs, mutual funds, jewellery, drawings, etc., without consideration and exceeding the fair market value of more than ₹50,000. Income from such gifts should be reported under the headIncome from Other Sourcesin the Income Tax Return, and tax at slab rates should be paid."

Yes, if you gift these shares, the date of acquisition will be considered based on when the sender of the gift (i.e. you) had originally purchased the share. Hence, the gains will be long-term in the above stated example.

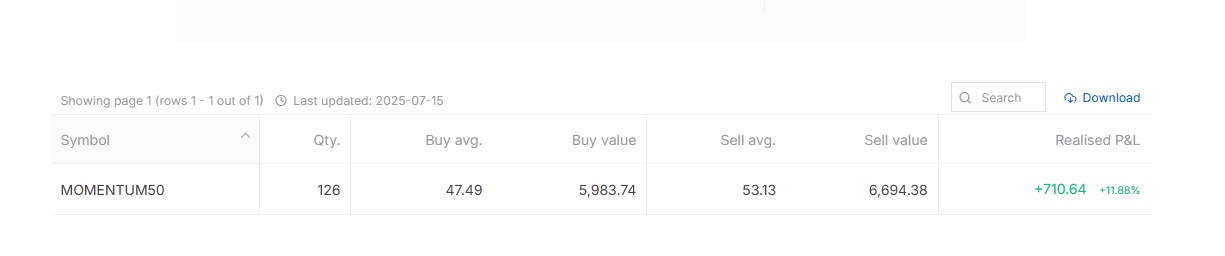

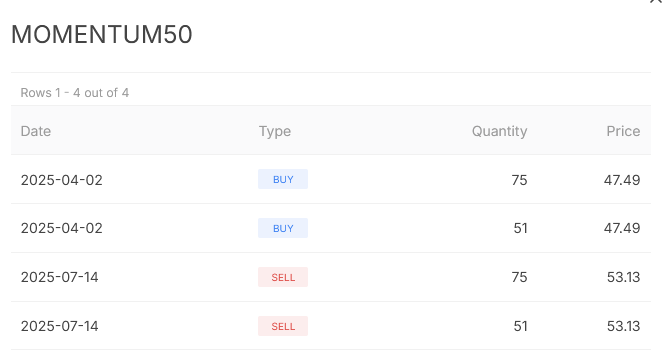

hi @siva@Quicko successfully gifted shares to a family member. the same is reflecting with the updated price. However, in console of the sender, the transaction is showing a Realised profit.