Suppose there’s an fd of Rs. 100000 @ 10% interest for a year. Now after Q2, a TDS of Rs. 1000 was deducted, ignore the interest limit breach part and that no 15g/h is there. Then for the remaining two quarters there will be no interest on the TDS amount that has been deducted? I mean instead of the maturity value of Rs. 110000 as mentioned on the fd certificate, the maturity value will be 110000-1000(TDS)-Interest amount on 1000 for 2 quarters? A SFB bank is saying that there is no compounding benefit on the amount deducted as tds, not able to understand this part. Never heard this before in any bank.

Can someone please explain how it works with a better example? Also from this financial year onwards what is the interest limit for seniors and non senior citizens on which no tds is deducted?

No TDS will be deducted because your FD is only 1 Lakh. TDS is deducted only when your interest exceeds 40k for regular taxpayers and 50k for senior citizens. Otherwise, there is no TDS deduction. If your principal amount is higher, you can submit Form 15G/H to avoid TDS.

Some banks calculate TDS based on the total interest earned from all FDs together,while others may deduct TDS based on each individual FD.

The maturity amount that is printed on your cumulative Fixed Deposit Receipt (FDR) does not take into account the impact of tax that may be deducted (TDS) if the interest earned is more than the government specified threshold. What this means is that the maturity amount printed on your FDR includes the additional interest earned due to compounding of inter even on the TDS amount as it is based on default assumption that no TDS will be deducted. Therefore, entire calculation changes if TDS is deducted.

Normally, TDS on a cumulative FD is automatically deducted by the bank if the interest on the FD crosses a threshold specified by tax laws.

Sir thanks for replying. The figures in the example are hypothetical figures to make the case understandable and simple. The fds belong to a senior citizen with only source of income being fd interest. AFAIK the maturity value should be, Principal amount + Interest – TDS amount but like I said the bank is willing to give in mail that the amount deducted as tds in q3 and q4 respectively won’t be counted under compounding benefits. As per them as interest of fds is cumulative so tds deducted in q3 and q4 wont get any interest and hence the maturity value will be lower then the value which is mentioned in the printed FD certificate given by them at the time of FD booking. As per them maturity value is, Principal amount + Interest – TDS amount- No compounding interest on TDS deducted. Just want to know are they right here? Do all banks follow similar way of calculations if there is TDS? Can we trust their system’s calculations here or should one do the calculations manually to check if the maturity value given by them is right or wrong?

Is there any notification by RBI about this? Notification or something which says that tds deducted amount will not be given interest?

And lastly last year if form 15g/15h were submitted then no tds was to be deducted for non senior citizens till 2.5 lacs interest and till 3 lacs for senior citizens. Have they changed this amount this year?

Sir thanks for replying. The fds belong to a senior citizen with only source of income being fd interest. AFAIK the maturity value should be, Principal amount + Interest – TDS amount but like I said the bank is willing to give in mail that the amount deducted as tds in q3 and q4 respectively won’t be counted under compounding benefits. As per them as interest of fds is cumulative so tds deducted in q3 and q4 wont get any interest and hence the maturity value will be lower then the value which is mentioned in the printed FD certificate given by them at the time of FD booking. As per them maturity value is, Principal amount + Interest – TDS amount- No compounding interest on TDS deducted. Just want to know are they right here? Do all banks follow similar way of calculations if there is TDS? Can we trust their system’s calculations here or should one do the calculations manually to check if the maturity value given by them is right or wrong?

Is there any notification by RBI about this? Notification or something which says that tds deducted amount will not be given interest?

And lastly last year if form 15g/15h were submitted then no tds was to be deducted for non senior citizens till 2.5 lacs interest and till 3 lacs for senior citizens. Have they changed this amount this year?

Mam thanks for replying. So, is the bank right when they say that maturity value is, Principal amount + Interest – TDS amount- No compounding interest on TDS deducted ? Like you have mentioned this way the maturity value will be lower than the maturity value printed on the FDR.

Do all banks, PSU/Private/Cooperative/SFB/NBFC’s, follow similar way of calculations if there is TDS? Can we trust their system’s calculations here or should one do the calculations manually to check if the maturity value given by them is right or wrong?

Is there any notification by RBI about this? Notification or something which says that tds deducted amount will not be given interest?

And lastly last year if form 15g/15h were submitted then no tds was to be deducted for non senior citizens till 2.5 lacs interest and till 3 lacs for senior citizens. Have they changed this amount this year?

You can fill form 15g/h then. I agree that it’s cumbersome but it’s the way unfortunately due to tax rules.

Then the interest will be paid on whole amount since TDS would be 0

And if you fill form 15g/h, I think TDS will not be reduced irrespective of total interest income.

But yeah you should only fill that if you will not be liable for income tax after counting all income in a financial year. Not to avoid TDS

I don’t think such a notification exists.

Bank is paying TDS to govt. So it is not reasonable to expect them to pay you interest on money they don’t have. It would be a loss for them. Hope you understand.

I have few FDs and I don’t get FD interest on TDS paid

@neha1101

Mam this article corroborates what you have mentioned

Few questions-

If form 15g/15h are submitted then no tds is to be deducted for non senior citizens till 2.5 lacs interest and till 3 lacs for senior citizens. Have they changed this amount this year?

My known senior citizen for whom I am asking these queries, had mutliple fd’s. Now what the bank has done is they did not deduct TDS from few fd’s but deducted more tds from the remaining fd’s. The total TDS deducted is 10% of the interest credited + interest accrued amount. It is just that for few fd’s the TDS deducted is NIL, whereas for the others they have deducted like 15-20% to match the total tds deduction. Can this lead to additional loss of interest or something for the accountholder?

Continuing the above point, we want to calculate the Loss due to non-compounding of TDS on all the fd’s. What information should we ask from the bank to calculate that manually and how exactly to calculate that?

RBI hasn’t yet closely regulated these kind of operational details, so this situation might still occur. Additionally, banks can deduct TDS whether your payout is monthly, quarterly or auto-renewal.

For monthly and quarterly payouts, you receive your interest on time but may miss out on compounding benefits. Along with this, if Form 15H submitted and your interest earnings in lakhs then also TDS might be deducted by bank. In such cases, you would need to claim refund through ITR process. However, for payouts at maturity and auto-renewal, you can benefit from compounding even though TDS may still be deducted.

Every bank has its own internal accounts often called dummy accounts, which are used to handle these kind of transactions, like transferring FD interest from one account to another on payout day. This could impact your compounding benefits because each bank has its own method of calculating interest. You must check how much tax has been deducted and from where, for this you can request TDS certificate, an interest certificate, complete FD statement from your bank.

Actually sir the fd in question is has the interest payout frequency: on maturity

About the rest of your reply, please check this post Doubt regarding taxation on fd's - #9 by tax007 it seems what that bank said is true. Requesting you to share your kind opinion about the final queries mentioned in that reply.

Yes. basic exception limit is 3L in new regime for everyone. 3L only for senior citizens in old regime.

Not all TDS gets 5.5%. Interest is compounded quarterly and interest is per annum. Loss calculation is number of days the TDS would have grown (if not cut) * 5.5/365.

They are calculating compounding for that amount since the day it is cut. So you cannot do simple TDS * 5.5%

You have to ask bank why they didn’t cut.

TDS every quarter will just be 10% of quarterly amount credited. Simple.

You will get TDS certificates from bank. you can do

(Days left till maturity)/365) * 5.5% * TDS amount

to get loss (approx).

Exact figure is complex to calculate due to compounding. You will have to do every quarter to get exact figure and then add that for next quarter on top of principle and then again do it (compounding)

In a FD where the interest is paid on maturity, the compounding happens every quarter. In this case where TDS is computed, I believe out of the total interest you receive 10% is deducted and paid out as tax and only the balance will be used to compound. If the person has internet banking, he can select the deposit and see the schedule, it will clearly mentioned, Interest amount - TDS deducted.

So for your question which amount get compounding, the amount after deducting TDS.

Also not sure why you mention this as a Loss. If the amount is within the person income tax ceiling, he can file returns and get the refund.

Sir when they say 2.5 lacs or 3 lacs, as per old regime, does this mean net income (after adjusting all deductions) or does it mean gross income?

They are saying that its due to a technical error but to make up for this they deducted this tds amount from the other fds. Is this ok? Logically speaking if they forgot to deduct tds from a 1 lacs fd but later deducted that amount from a 5 lacs fd, then is there any additional loss due to non-compounding of TDS?

Suppose tds deducted after Q1, so 90/365*Rate of fd interest * TDS amount? Doing this so every quarter will give us the amount lost due to non-compounding of TDS on all the fd’s? I understand that this is very tough and the bank might have been right on their calculations part. But seeing the mess that they have created and seeing their responses we just wanted to double check it. Makes sense?

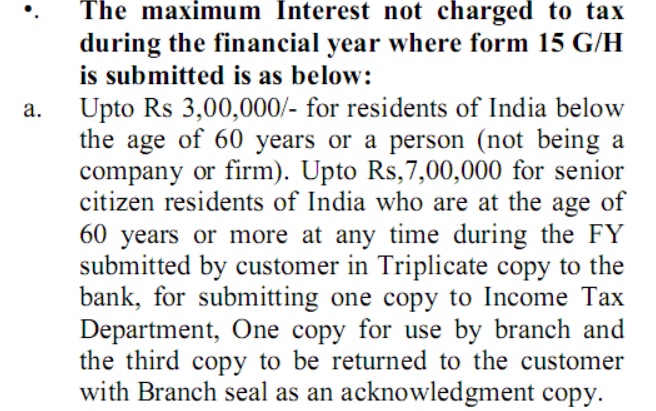

Edit- The terms and conditions mention on the fdr has this point

Have they increased the limit for 15g and 15h from 2.5 lacs and 3 lacs to 3 lacs and 7 lacs respectively? I am not able to find any notification about this on the internet.

Mam are you sure on this part? Because almost all articles say that the threshold for non deduction of TDS after submitting form 15G and 15H is 2.5 lacs and 3 lacs for non senior citizens and senior citizens respectively.

Mam your last post made this part clear. This link corroborates your point + they have given a table in the article TDS on FD: TDS on cumulative FDs: Your money loss is more than the tax deducted - The Economic Times which explains the Loss due to non-compounding of TDS on fd’s, about which I am asking about. Can you please check that once? This is what I am asking as in how can we calculate this manually ourselves?

One more thing, lets say there were fds of 1 lacs and 5 lacs. Now what this bank has done is they did not deduct any tds on the interest earned from the 1 lacs fd but they have deducted its tds from the 5 lacs fd along with the tds applicable on the 5 lacs fd. Logically speaking if they forgot to deduct tds from a 1 lacs fd but later deducted that amount from a 5 lacs fd, then is there any additional loss due to non-compounding of TDS which the accountholder will bear?

Edit- The terms and conditions mention on the fdr has this point

Have they increased the limit for 15g and 15h from 2.5 lacs and 3 lacs to 3 lacs and 7 lacs respectively? I am not able to find any notification about this on the internet.

So should we just trust them? Do banks make mistakes, genuine or deliberate, in cases like this?

This is jana bank. I asked hdfc bank, they were also not sure but did say that till 7 lacs there is no tax deducted. I think they were confusing it with the new tax regime. Did the government release any notification regarding about the threshold limit till which no tds is deducted if from 15g/h is given? It used to be 2.5 lacs for non senior citizens and 3 lacs for senior citizens.

sir all SFB’s are quoting the threshold limits as mentioned in the screenshot in this post but all public/private sector banks are sticking with the interest threshold limits of 2.5 lacs and 3 lacs if form 15g/h are given. Wasn’t able to find any notification on this also online. + @neha1101@Rathi