When you buy an ELSS fund, the units are under lock-in period for 3 years from the date of purchase.

Let say an ELSS fund has a TER of 1%. We know that TER is on a yearly basis which means 1% of the purchased amount is the total expense ratio of the units for a year from the date of purchase. Now, because of the 3 years mandatory lock-in condition of the ELSS units, wouldn’t the TER of the ELSS fund be effectively 3% compounded? (1+1+1)% compounded TER.

If this is the correct way to think, then one should be conscious about the TER of the ELSS funds; the lower the better. Also, while redeeming, this compounded TER should be taken into consideration for calculation of the returns - profit or loss.

Regardless of the type of the fund, expenses work the same way and they compound over a period of times as your investments grow. it’s just that ELSS has a lock-in period. The NAV declared at the end of the day is net of costs and the P&L you see is your actual P&L.

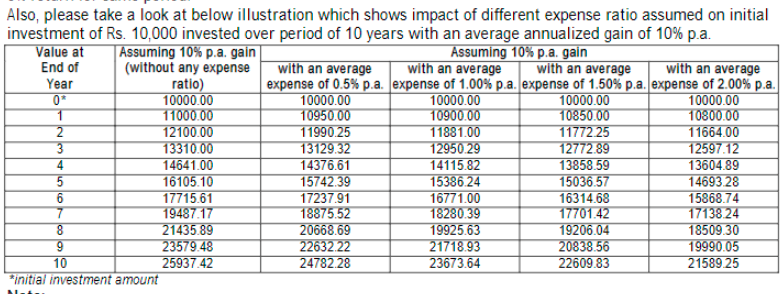

Here’s a simple illustration

Just to add onto what @RahulKhanna has mentioned,it is true that the expense ratio is compunded but not in an incremental manner as you have explained. That way in 10 years if your expected cagr is 10%, TER is 10% then returns are 0

NAV on a daily basis is calculated after factoring in the TER. The ideal way to analyze the effect would be to just subtract the TER from your expected rate of return.

For example. as per the data shown in the table above, if you had invested ₹10000, expected ROI is 10% , holding period is 5 years then you would earn ₹16105. But if 1% TER is considered then your ROI changes to 9% and you would earn ₹719 lesser which amounts to ₹15386.

So yes, higher TER does have an effect on your returns. This is the reason why direct plans exist and the difference in TERs is more visible for equity oriented funds. But its important to note that lower expense ratio doesn’t necessarily translate to better fund performance. It may impact your returns but fund performance will depend on how it has been managed by the fund manager.

@RahulKhanna@faisr I may have articulated the question differently, but the essence of what I mean to ask is the effective cost of buying an ELSS fund is 3X TER for the first 3 years. Since the units are locked-in so you are paying that much for sure. Am I correct on this part? And this is why many distributors push you to have ELSS funds for all investments and not just for tax-saving purpose to earn more commission making use of this lock-in period.

P.S. I know this TER is already captured in the NAV and the returns include this cost.

Nope. If it’s 3X, you might as well buy an ULIP

Expense ratio calculations are the same for all funds. It’s the equivalent of you holding an open-ended fund for 3 years.

Again, since you have no choice to exit from an ELSS fund, before completing 3 years, isn’t the basic cost more than what you perceive, is all I am asking? TER of 3 consecutive years is what you have to pay regardless of the performance of the fund.

I’ve already answered this in 2 different ways. Your expenses are deducted at the end of the day in the NAV and not aggregated and charged the end of the investment when you redeem. Regardless of whether you have an open ended fund or an ELSS fund, expenses are charged the EXACT same way!

My friend, I got this. But since you can’t exit from an ELSS fund before completing 3 years, you have to have to pay the cost for 3 years for sure. Compared to an open-ended fund, although the NAV and costs are calculated in the same way, you have the choice to make an exit instead of being locked-in. This is the difference I am trying to highlight.

Let’s appeal for third umpire @nithin if he could understand my pov.

Opportunity cost - If that is the word, I am with you because there is no escape from paying cost for 3 years until the units are locked-in and you can’t exit, and regardless of how the funds perform in those 3 years. And with that pov, the ELSS funds have an effective opportunity cost tagged along, compared to an open-ended fund. So while choosing an ELSS fund, checking the TER matters even more.

@rupeshmandal These ELSS funds are also open-ended scheme. Unlike a close-ended scheme where you can only exit once the scheme matures or you cannot invest post NFO, you can enter and exit an open-ended scheme at any point of time post the the NFO. So, a ELSS scheme is open-ended per se.

Also like @RahulKhanna mentioned, this is the price you pay for an investment which is having the least lockin period and better returns compared to its peers under section 80 C.

@faisr yes I agree on ELSS being open-ended fund with the mandatory lock-in period for 3 years, so you can’t escape but pay cost for 3 years from the date of purchase. But as @RahulKhanna said, it’s the price you pay to save tax.

Having said that, in the budget, our hon’ble FM has proposed CPSE ETF and Bharat-22 ETF as tax-saving instrument with 3 year lock-in. If this happens, it would be a low cost alternative to the actively managed ELSS funds. Also, it would open doors for tax-saving @smallcase which would be a combination of these two ETFs in a proportion to get better ROI.

It will be interesting to see how this would be implemented. The 3 year cagr for cpse etf its close 6-7%, in comparison most of the ELSS schemes have given more than 10% returns for the same durstion and bharat 22 is still relatively new.

If ELSS-like ETF become a reality then EPF, NPS funds would also start investing in it. Because of mandatory EPF deduction from an employee and increments every year, the ETF would get significant inflows year on year. But, I have another pov, Govt. is increasing public contributions to these state-run companies as divestment policy. Is it because Govt doesn’t have funds and/ or the cost of running them is getting bigger and bigger with NPAs, Scams, so now raising funds from public to fill the gap. But the management, accountability and corporate policies of these state-run companies remain the same. So i am not sure about the outcome. With more public holding, if these companies fail, then these common people only lose money.