Please Provide an EMA RSI Strategy for Option Buying (CALL) in Nifty

General Conditions:

- Strategy – Option Buying

- Indices – Nifty

- Time Frame – 3 Minute Candlestick

- Maximum Entries – 2 Nos per day

- Reward to Risk – Rs.20/- Points : Rs.15/- Points

Trigger Candle conditions:

- Trigger candle should be a strong bullish green candle, not a base candle.

- Trigger candle close should be above 15 EMA & 33 EMA.

- Triggered candle 15 EMA should be above 33 EMA.

- Trigger candle RSI should be above 60.

- Either body or atleast bottom wick of the triggered candle should touch 15 EMA.

Entry & Exit Conditions:

- Entry Time – After 09:45 AM and Before 2:30 PM.

- Strike Price – ATM strike Price.

- Entry should be on the next first candle of the triggered candle, if the price crosses high of the triggered candle in the Nifty chart.

- Live positions if any should exit at 03:00 PM.

- Before hitting Target or SL of the first entry no second entry should be taken.

2 Likes

Just a halfbaked amateur run. If it helps.

from kiteconnect import KiteConnect

import pandas as pd

kite = KiteConnect(api_key="your_api_key")

kite.set_access_token("your_access_token")

def ema_rsi_strategy():

# Get historical data for Nifty

data = pd.DataFrame(kite.historical_data(instrument_token=256265, from_date='2022-01-01', to_date='2022-02-01', interval='3minute'))

# Calculate 15 EMA and 33 EMA

data['ema_15'] = data['close'].ewm(span=15).mean()

data['ema_33'] = data['close'].ewm(span=33).mean()

# Calculate RSI

delta = data['close'].diff()

gain = delta.where(delta > 0, 0)

loss = -delta.where(delta < 0, 0)

avg_gain = gain.rolling(window=14).mean()

avg_loss = loss.rolling(window=14).mean()

rs = avg_gain / avg_loss

data['rsi'] = 100 - (100 / (1 + rs))

# Set initial values for entry and exit conditions

entry_time_start = '09:45:00'

entry_time_end = '14:30:00'

exit_time = '15:00:00'

entries_per_day_max = 2

entries_per_day_count = 0

reward_to_risk_ratio = 20 / 15

for index, row in data.iterrows():

# Check if current time is within entry time range

current_time = row['date'].time()

if current_time >= datetime.strptime(entry_time_start, '%H:%M:%S').time() and current_time <= datetime.strptime(entry_time_end, '%H:%M:%S').time():

# Check if maximum number of entries per day has been reached

if entries_per_day_count < entries_per_day_max:

# Check trigger candle conditions

if row['open'] < row['close'] and row['close'] > row['ema_15'] and row['close'] > row['ema_33'] and row['ema_15'] > row['ema_33'] and row['rsi'] > 60 and (row['low'] <= row['ema_15'] or (row['open']+row['close'])/2 <= row['ema_15']):

# Entry condition met

print(f"Entry condition met at {row['date']} with price {row['high']}")

# Calculate target price and stop loss price based on reward to risk ratio

target_price = round(row['high'] + reward_to_risk_ratio * abs(row['high'] - data.loc[index-1]['low']), 2)

stop_loss_price = round(row['high'] - abs(row['high'] - data.loc[index-1]['low']), 2)

if row[‘high’] > data.loc[index-1][‘high’]:

Place entry order if the price crosses high of the triggered candle in the Nifty chart

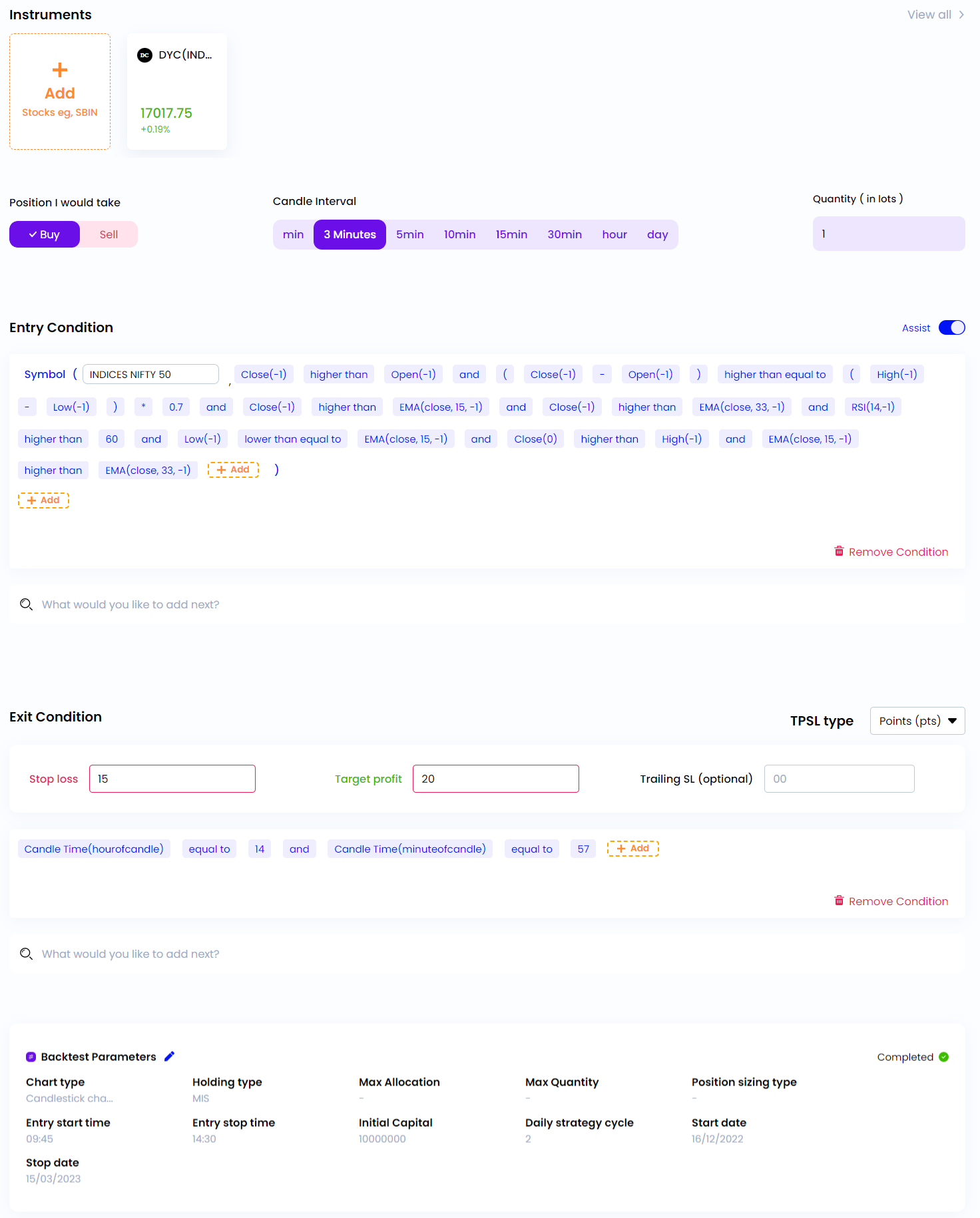

@trade4lyf Check out the image below to learn how to create the strategy conditions: