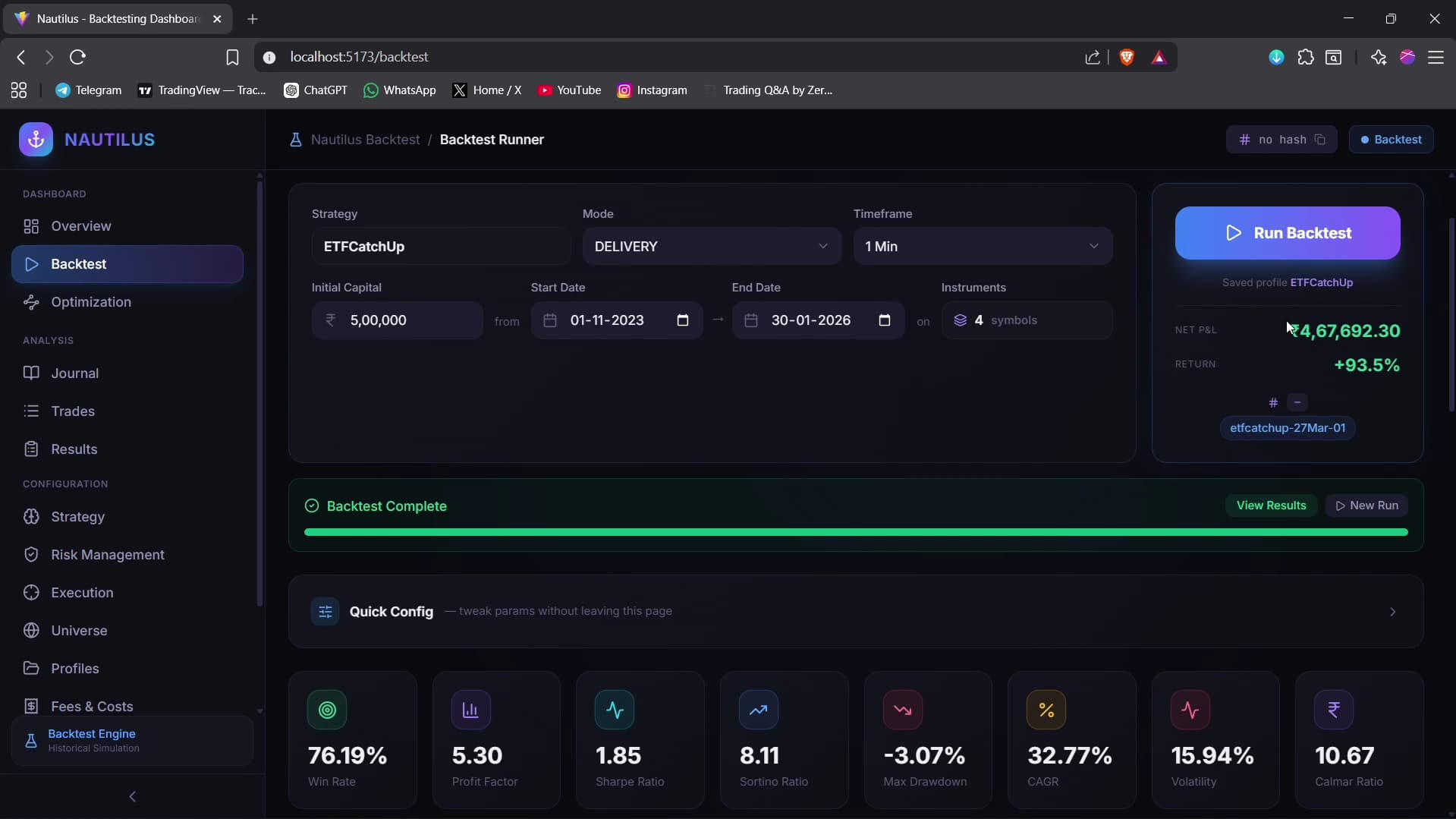

I recently tested a simple ETF strategy idea and got around ~90% return in a 2-year backtest, but I am not fully satisfied with the result.

The idea is simple:

If the parent index moves significantly intraday, the corresponding ETF sometimes reacts late. So the strategy enters the ETF near the end of the day and holds for a few days with risk rules and time-based exits.

Backtest results look good, but there are a few issues:

- I only have ETF data for the last ~2 years, so the strategy is tested only in one market regime.

- In the same period, buy & hold on Gold/Metals ETF would have given very high returns (~200–300%), so beating buy & hold is important.

- Backtest results are not enough — I plan to do parameter optimization, walk forward optimization and then paper trading to see real behaviour.

I believe a strategy should be tested across bull, bear and sideways markets and should be compared against buy & hold before trusting the results.

Would love to hear suggestions on how to improve or properly test this strategy.