Hello and welcome to Beyond the Charts! A newsletter where we dive into fascinating charts from the world of finance and the economy, breaking down what’s happening in a way that’s easy to understand.

If you prefer watching video over reading, you can watch the episode here:

In the last episode, we talked about the US economy. Today, let’s turn our attention to the Eurozone.

The Eurozone is a group of 20 European countries that use the euro as their currency. It was created to make trade, travel, and economic cooperation easier. It’s managed by the European Central Bank (ECB) and includes major economies like Germany, France, and Italy.

The past few years have been tough for the Eurozone, with challenges like energy crises, inflation, and geopolitical tensions.

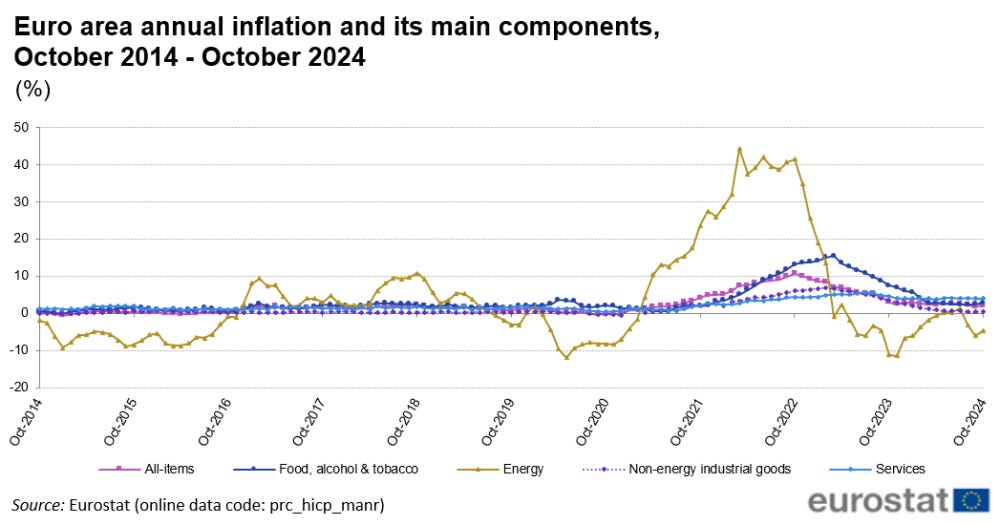

One major blow came in 2022 with Russia’s invasion of Ukraine. Many Eurozone countries relied heavily on Russian energy, so when gas and oil supplies were disrupted, energy prices soared. This led to record inflation, hitting households and businesses hard.

Source: Eurostat

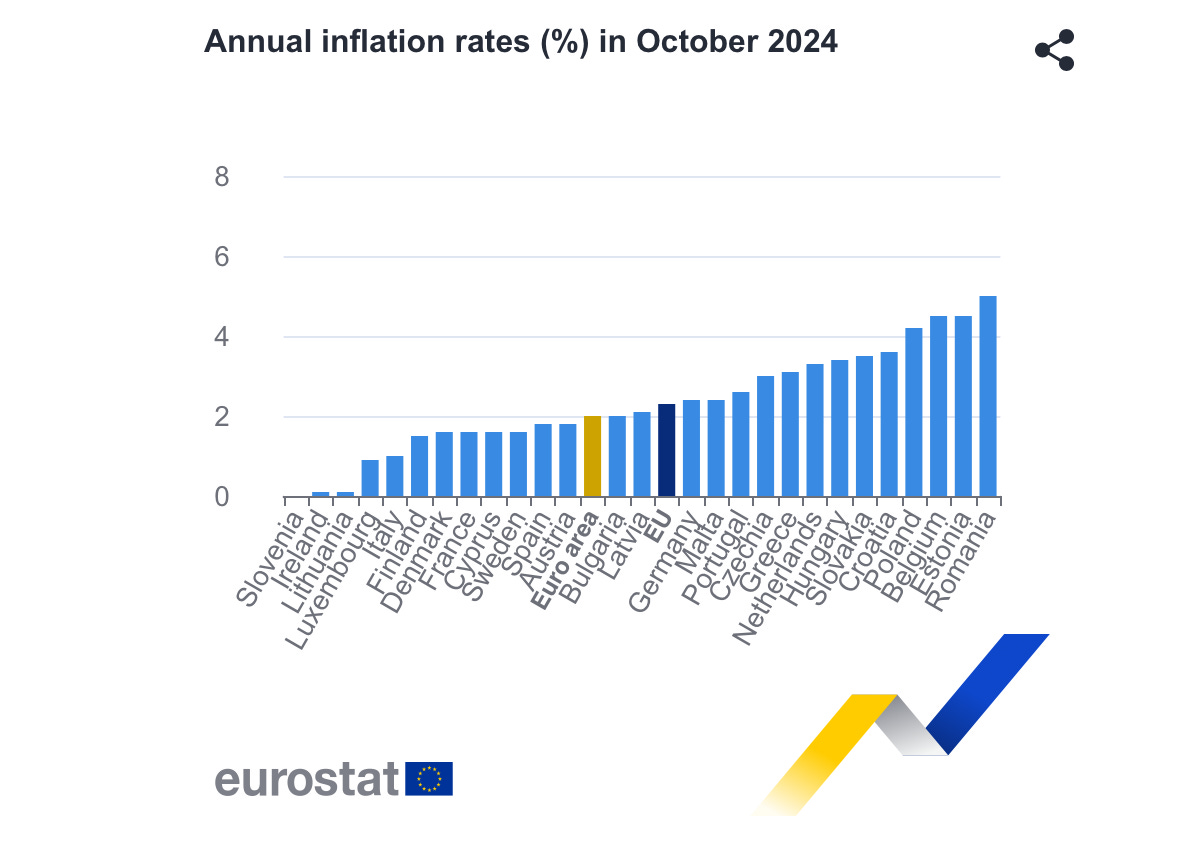

Inflation in the Eurozone has eased to the European Central Bank’s (ECB) target of 2%. However, the trend isn’t uniform across all countries. While nations like Slovenia and Ireland have seen minimal inflation growth, others, such as Romania and Estonia, are still dealing with rates above 4%.

Source: Eurostat

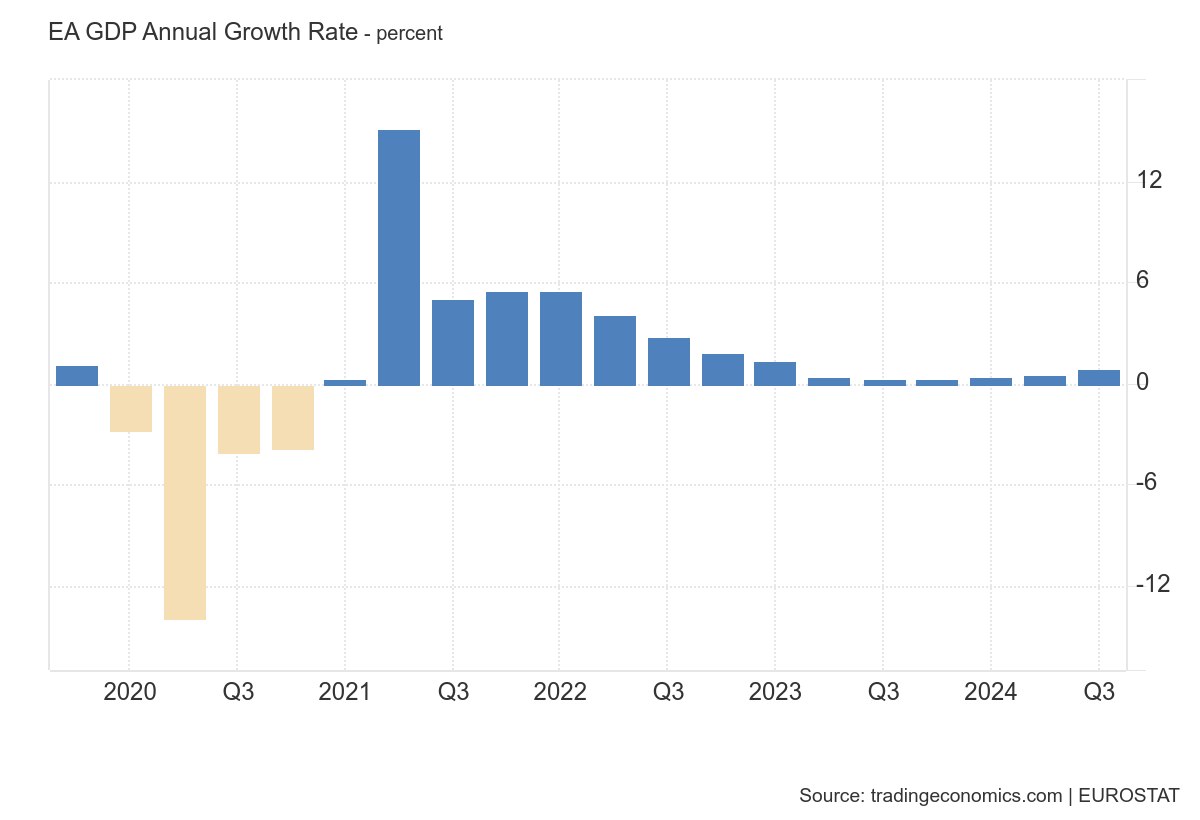

Inflation isn’t the only challenge for the Eurozone—trade imbalances are adding to the strain. The war disrupted key supplies of metals and grains from Ukraine and Russia, driving up costs and disrupting industries.

The conflict also triggered a wave of refugees seeking safety in Europe, increasing pressure on public services and government budgets. Over the past seven quarters, economic growth has barely moved, showing how deeply these issues have hit the region.

Source: Trading Economics

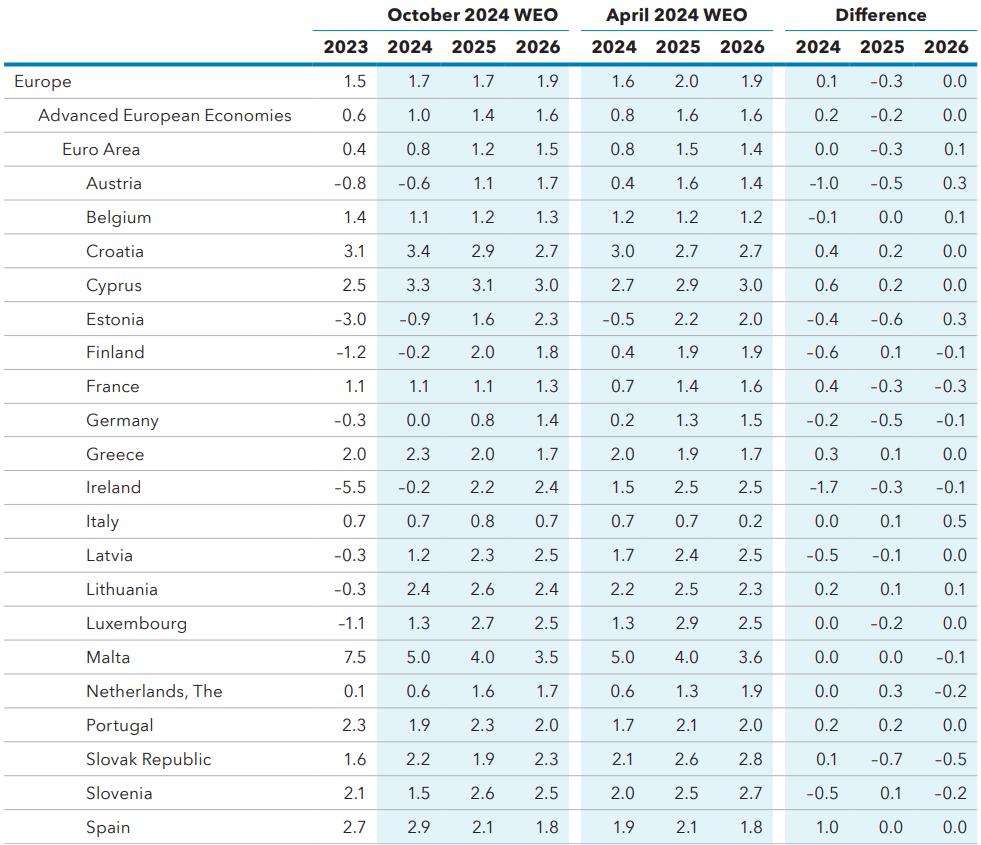

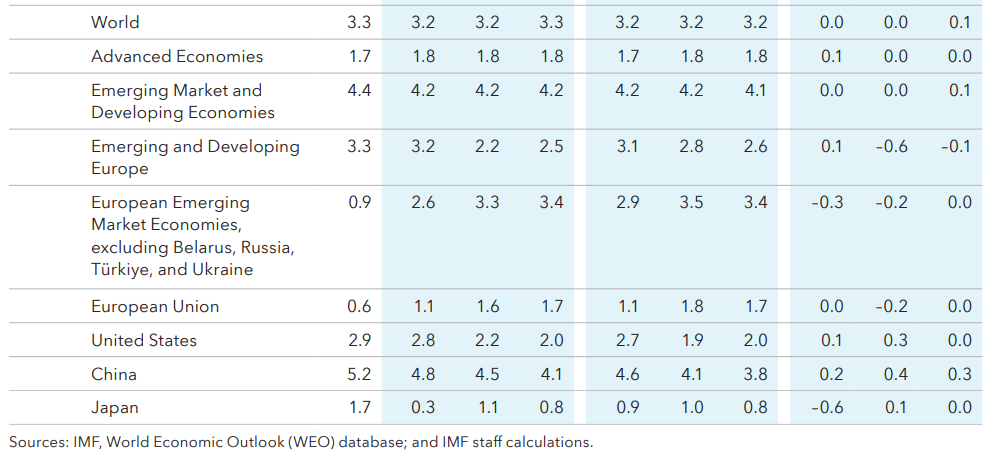

The International Monetary Fund (IMF) expects advanced European economies to grow by just 1.0% in 2024 and 1.4% in 2025. These numbers are not only lower than its April forecasts but also fall behind the growth projections for other advanced economies globally.

Source: IMF

The services sector has been a rare silver lining, growing despite the challenges. Consumer spending on dining, travel, and entertainment has helped support the economy. In contrast, industrial production has been struggling, with factories facing weak demand both in Europe and globally.

Source: IMF

These struggles are clear in the Eurozone’s largest economies—Germany, France, and Italy. Germany, in particular, feels the impact due to its reliance on manufacturing. Weak global demand and high energy costs are taking a toll, with Germany’s GDP expected to shrink by 0.1% in 2024 before seeing a modest recovery of 0.7% in 2025.

Source: European Commission

In Germany, key industries like automotive and machinery are seeing fewer orders, especially from China. Although energy prices have dropped since 2022, they’re still high enough to strain energy-intensive sectors. On top of that, high borrowing costs and uncertainty are holding back private investment.

Germany’s slow recovery isn’t just a local concern—it’s affecting its neighbors in Central and Eastern Europe, which depend on German trade and investment to fuel their economies.

Source: European Commission

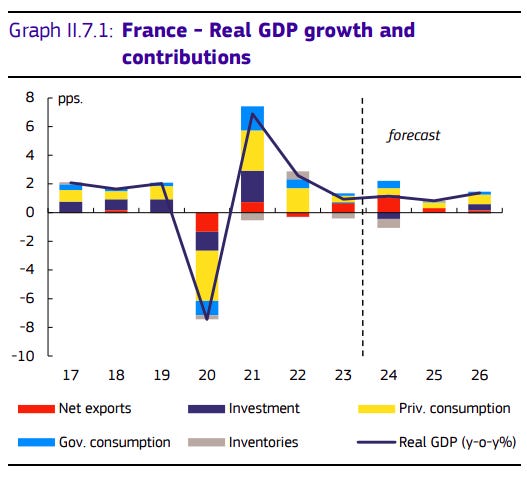

France tells a more balanced story, with its GDP expected to grow by 1.1% in 2024, supported by a strong services sector, especially in tourism, dining, and leisure. However, inflation in services remains a concern, driven by rising labor costs.

Challenges persist. Businesses are still reluctant to invest, and while consumer spending is improving, it remains cautious, reflecting ongoing economic uncertainties.

Source: European Commission

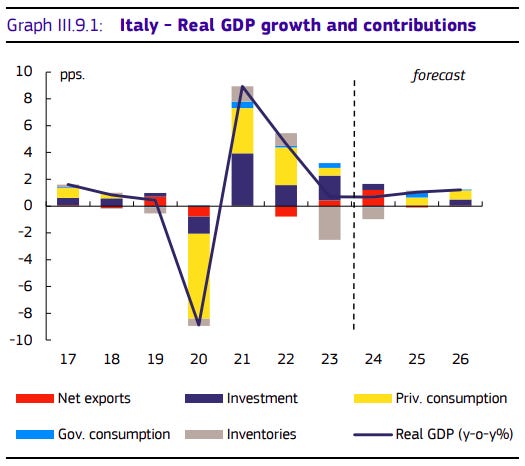

Italy’s economy is recovering slowly, with GDP projected to grow by 0.7% in 2024 and 1.0% in 2025. Tourism, a key driver, has rebounded strongly, and government investments in infrastructure and renewable energy are adding some momentum.

However, challenges remain significant. Italy’s public debt, exceeding 141% of GDP, limits its ability to maneuver fiscally. Additionally, structural inefficiencies and slow innovation continue to hurt competitiveness, making it tough for the economy to regain stable footing.

Source: European Commission

Circling back to the broader European economy, private investments, a key driver of recovery, remain weak. While financial conditions have improved slightly, businesses are still hesitant to invest. This caution stems from ongoing uncertainty about the global economy and persistent geopolitical tensions.

Source: IMF

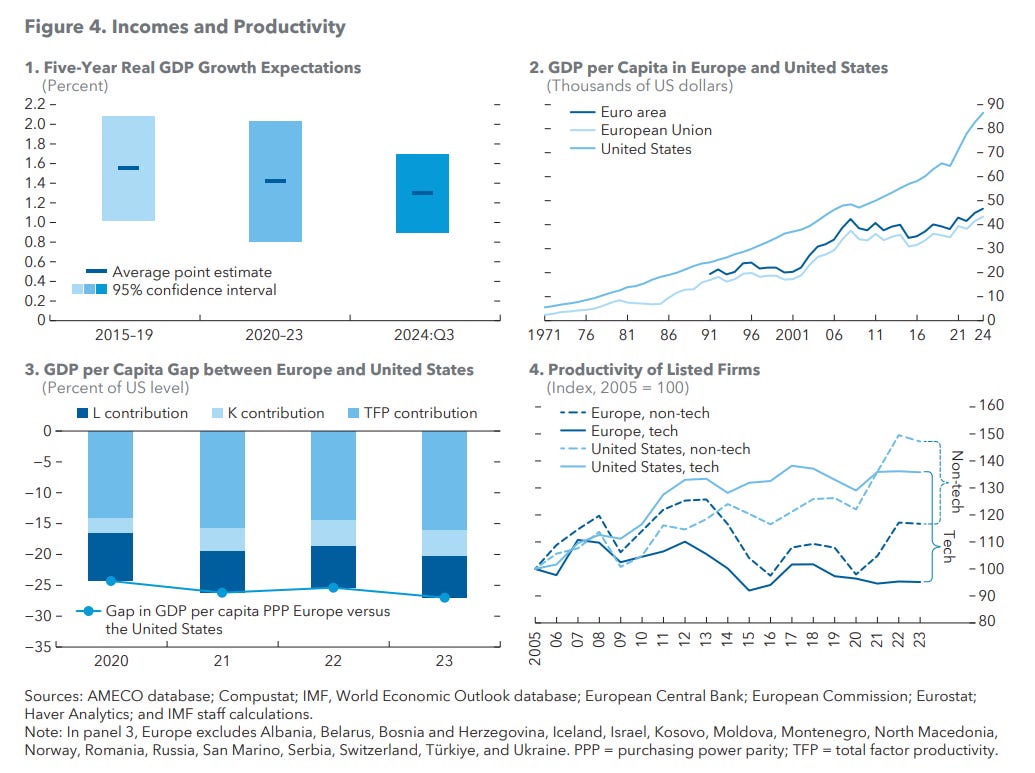

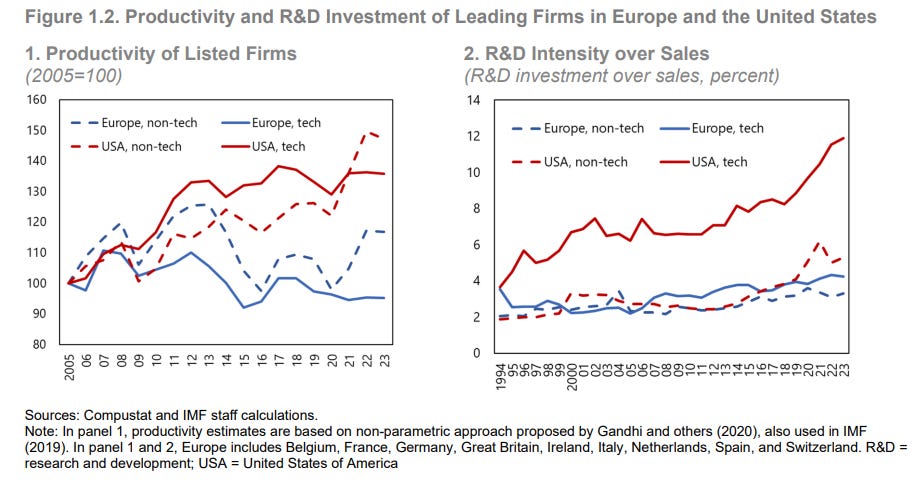

Europe also grapples with long-term challenges, including a significant productivity gap with the United States. Simply put, European businesses are less efficient and innovative compared to their American peers, which limits their competitiveness on the global stage.

Source: IMF

One key reason for this productivity gap is Europe’s fragmented markets. Unlike the United States, where businesses can scale easily across a unified market, European firms face varying rules and systems in each country. This fragmentation makes it much harder for businesses to grow efficiently and benefit from economies of scale.

Source: IMF

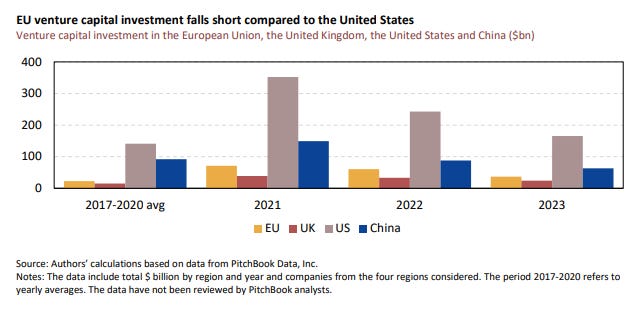

Another challenge is Europe’s underdeveloped capital markets. In the US, businesses, especially startups, have access to diverse funding options like venture capital and public markets. European firms, on the other hand, often struggle with fewer opportunities to raise capital, which slows down innovation and growth.

Source: European Investment Bank

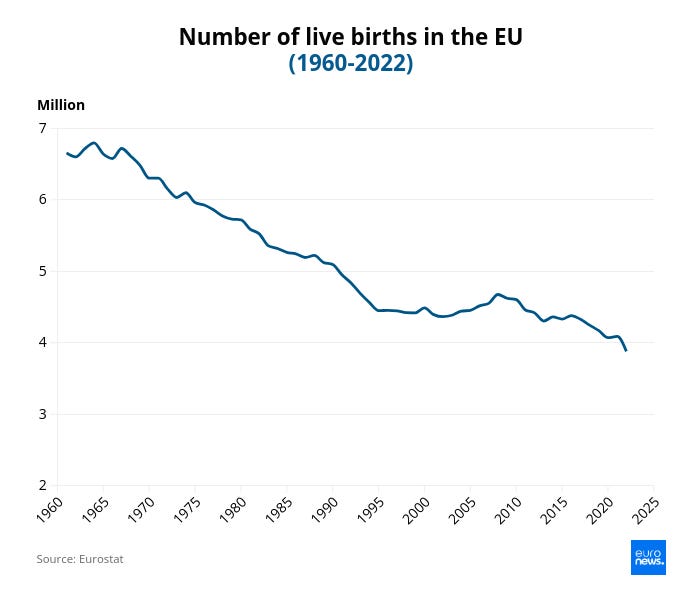

Demographics also play a key role. Europe’s aging population and low birth rates mean fewer young workers are entering the labor force, leading to significant skill shortages in many industries. To make matters worse, labor mobility in Europe is limited compared to the US, making it harder to create innovation hubs where talent can gather and fuel economic growth.

Source: Euronews

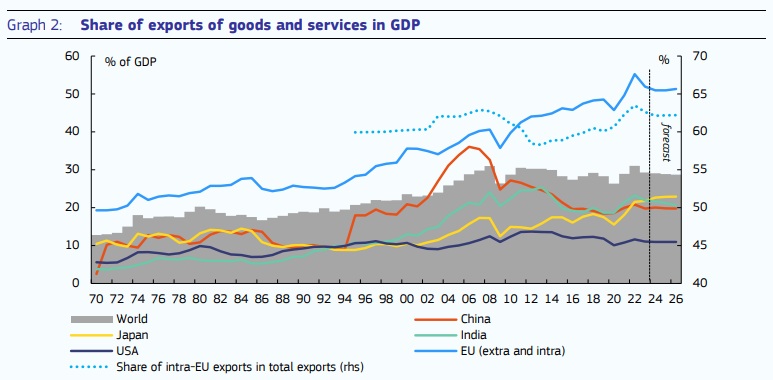

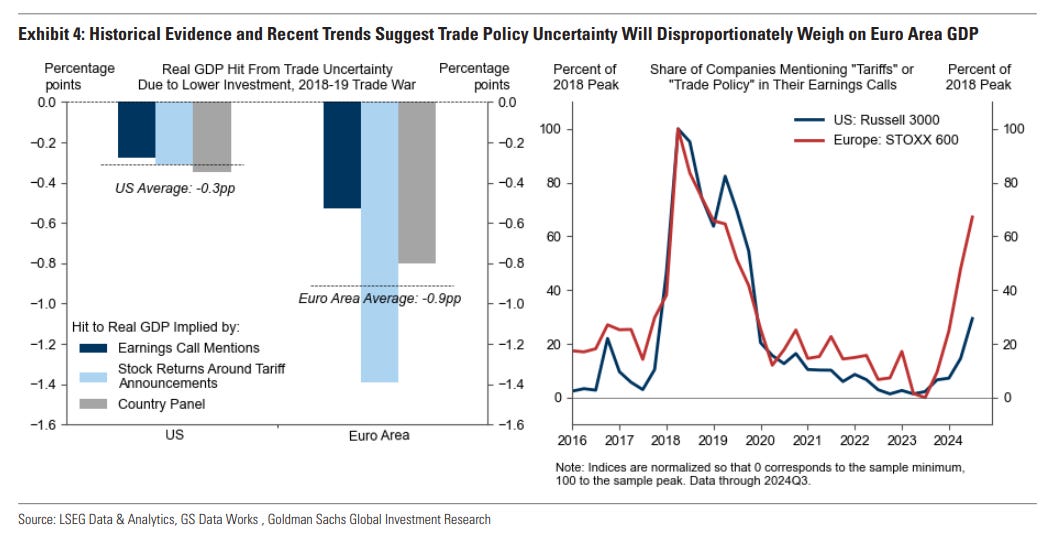

Another major risk for Europe is the potential imposition of tariffs by the United States, as proposed by President-elect Donald Trump. Since Europe relies heavily on trade, such tariffs could seriously impact its economy, disrupting exports and slowing growth.

Source: European Commission

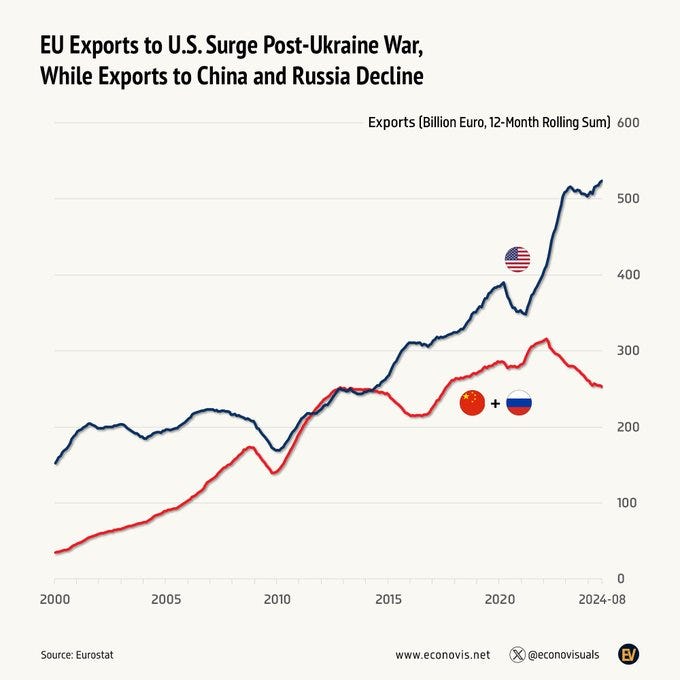

To add additional context, Europe has become more dependent on exports to the US. Between 2021 and August 2024, the European Union’s exports to the US grew by 31.1%, while exports to China and Russia fell by 19.2%. If Trump’s proposed tariffs on European goods go into effect, the Eurozone could face serious economic consequences, potentially cutting GDP growth by 0.9%, according to a Goldman Sachs report.

Source: Goldman Sachs

Source: Econovisuals

To sum up, the Eurozone is grappling with both immediate challenges and long-term structural issues. While inflation is easing, uneven recovery, weak private investment, and trade imbalances are still dragging the economy. The services sector has shown some resilience, but manufacturing and energy-intensive industries remain under pressure.

Long-term problems, like fragmented markets, underdeveloped capital markets, and an aging population, continue to hinder global competitiveness. On top of this, external risks, such as proposed US tariffs, add more uncertainty to an already fragile-looking economic landscape.

That’s it from us today. Do share this with your friends to spread the word.